• Security Working Group Chair: 楠正憲 (Japan Digital Design)、 松本泰 (セコムIS研)、崎村夏彦 (野村総合研究所) Editor: 佐藤雅史 (セコムIS研)、島岡政基 (セコムIS研) • Accounting Working Group 設立準備中 40

[1] ◦ ISO/TC307 WG2/JWG4にCGTFメンバーが多数参加 • Internet Engineering Task Force ◦ SecWGの成果物をInternet-Draftとして投稿 General Security Considerations for Cryptoassets Custodians [2] Terminology for Cryptoassets [3] ◦ 暗号資産のセキュリティに関するmailing-listの開設を予定 • 認定自主規制団体との関係 ◦ 日本仮想通貨交換業協会技術委員会に対するリエゾンの派遣 41 [1] Security management of digital asset custodians, ISO/NP TR 23576 [2] General Security Considerations for Cryptoassets Custodians, draft-vcgtf-crypto-assets-security-considerations, Masashi Sato and Masaki Shimaoka and Hirotaka Nakajima [3] Terminology for Cryptoassets, draft-nakajima-crypto-asset-terminology, Hirotaka Nakajima and Masanori Kusunoki and Keiichi Hida and Yuji Suga and Tatsuya Hayashi

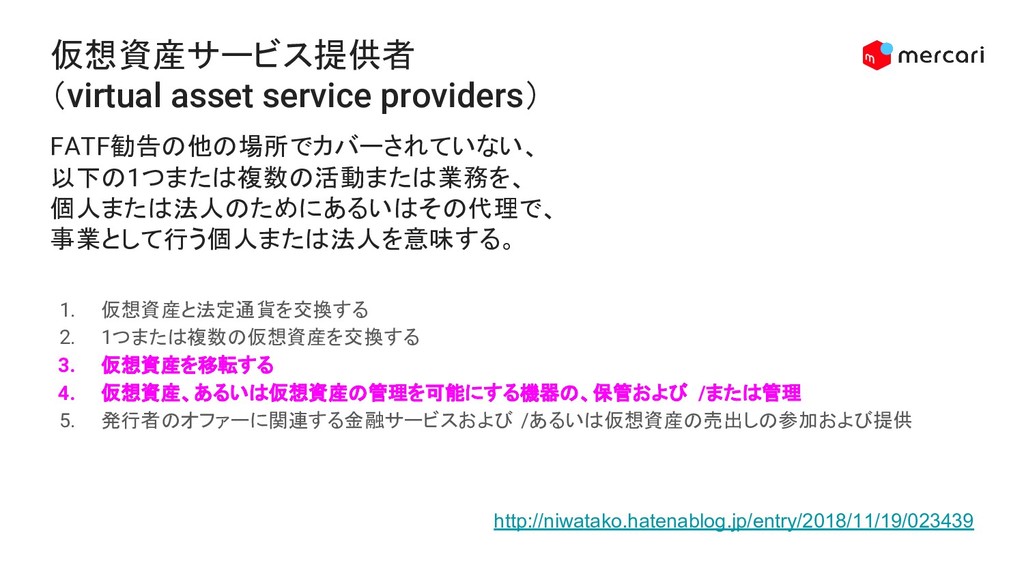

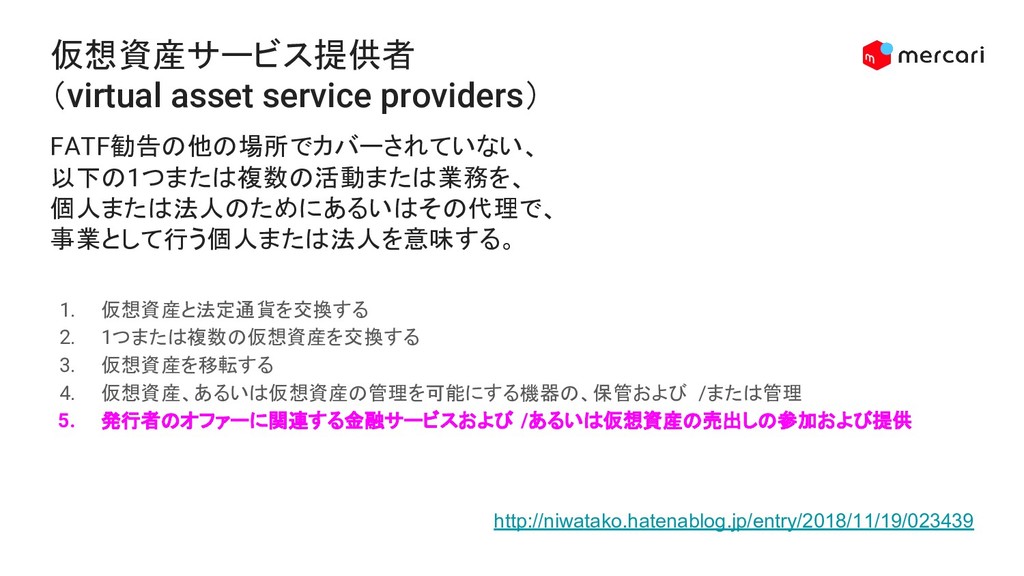

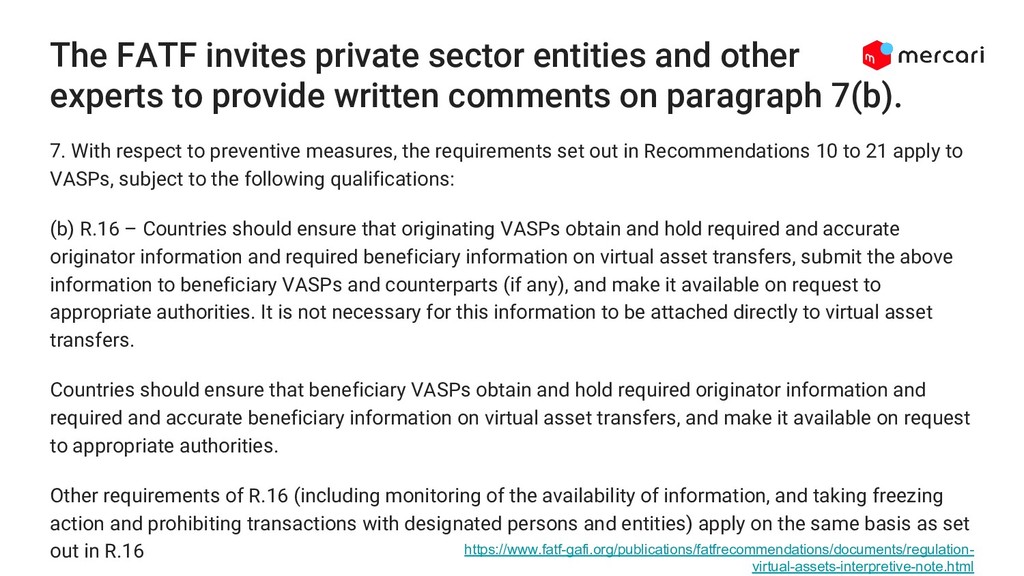

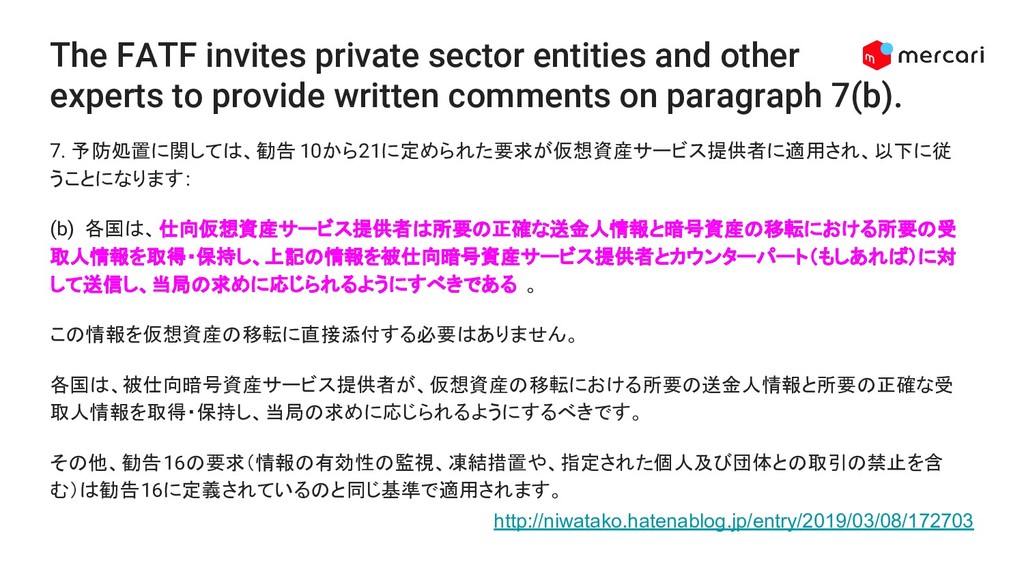

provide written comments on paragraph 7(b). FATFは7(b)について、民間機関やその他専門家に書面によるコメントの提供を求めます。 Comments should be sent to the FATF Secretariat by 8 April, at: [email protected]. コメントは4月8日までにFATF事務局( [email protected] )まで送付してください。 FATF Public Statement – Mitigating Risks from Virtual Assets http://niwatako.hatenablog.jp/entry/2019/03/08/172703

provide written comments on paragraph 7(b). 7. With respect to preventive measures, the requirements set out in Recommendations 10 to 21 apply to VASPs, subject to the following qualifications: (b) R.16 – Countries should ensure that originating VASPs obtain and hold required and accurate originator information and required beneficiary information on virtual asset transfers, submit the above information to beneficiary VASPs and counterparts (if any), and make it available on request to appropriate authorities. It is not necessary for this information to be attached directly to virtual asset transfers. Countries should ensure that beneficiary VASPs obtain and hold required originator information and required and accurate beneficiary information on virtual asset transfers, and make it available on request to appropriate authorities. Other requirements of R.16 (including monitoring of the availability of information, and taking freezing action and prohibiting transactions with designated persons and entities) apply on the same basis as set out in R.16 https://www.fatf-gafi.org/publications/fatfrecommendations/documents/regulation- virtual-assets-interpretive-note.html

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}