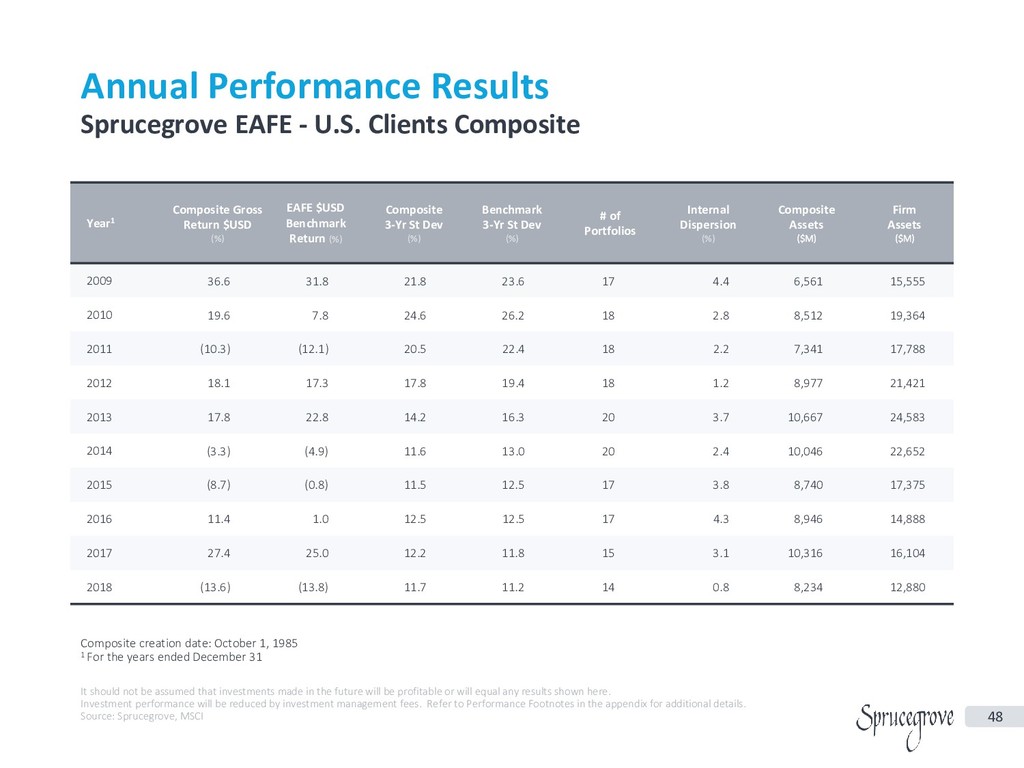

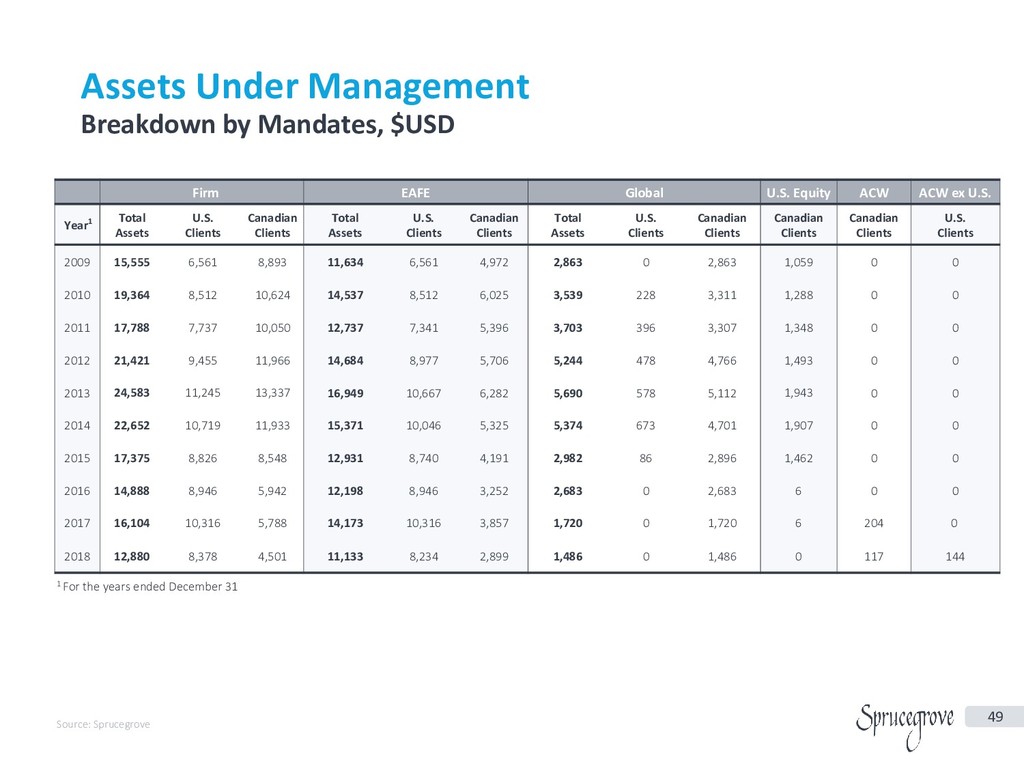

Title: Trend in North American Pension Market and Introduction of Value-Oriented Approach

Seminar Outline:

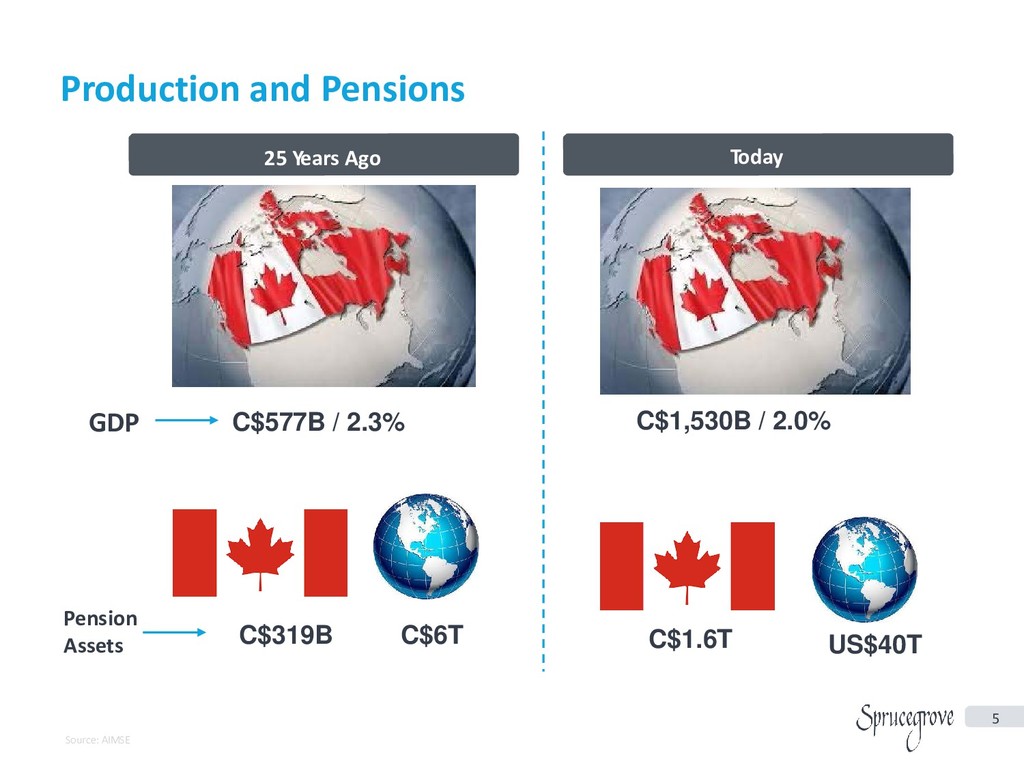

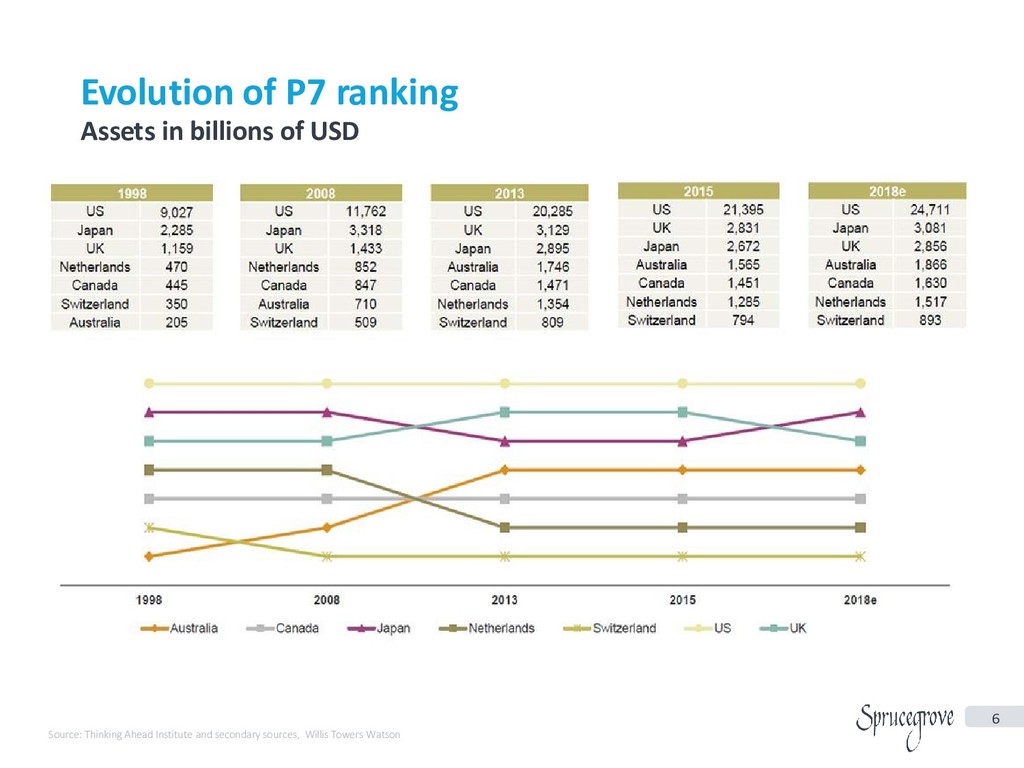

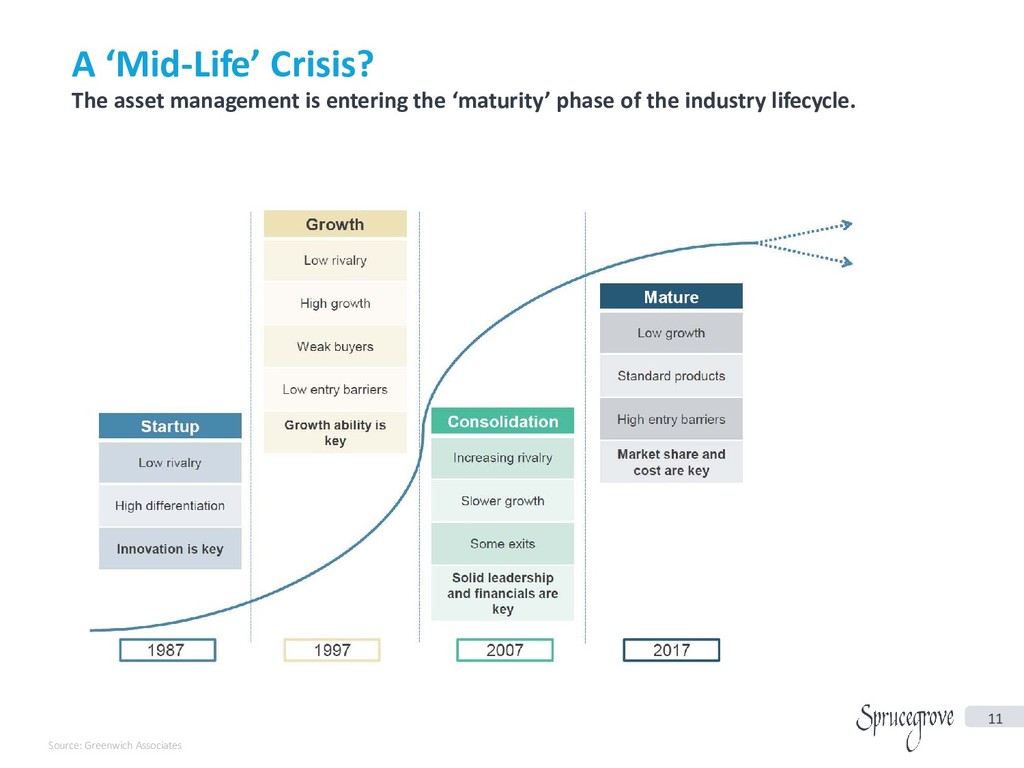

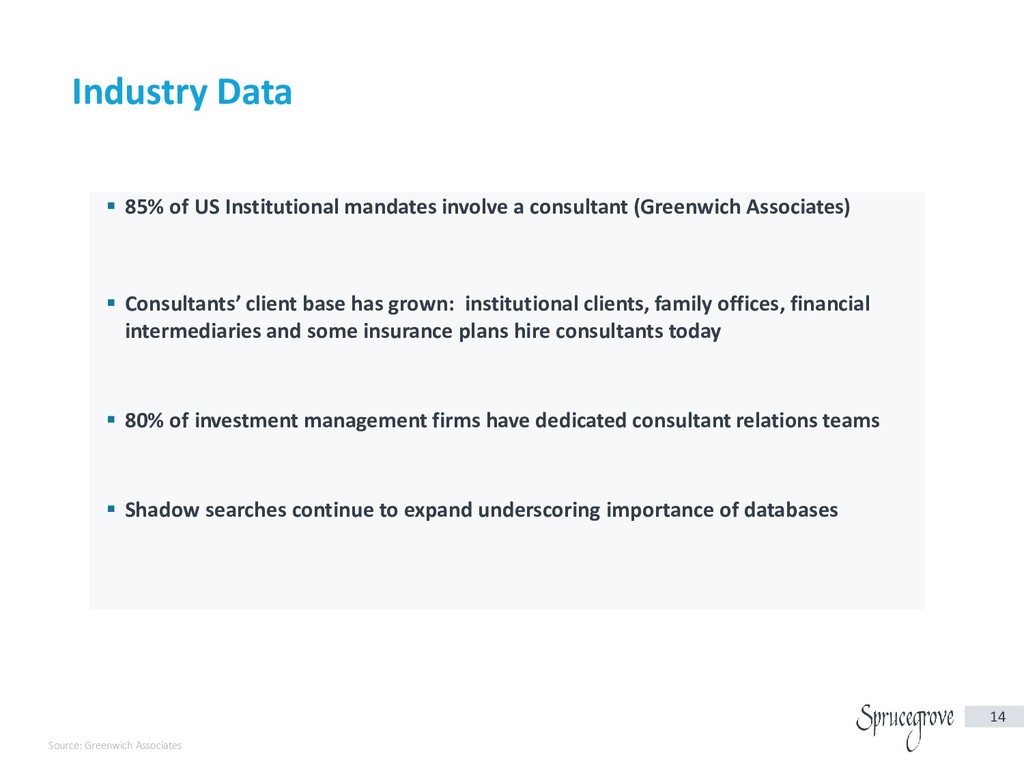

North American pension funds have grown their assets more quickly than their global peers over the past decade. This was driven by the strengthening US dollar and a greater emphasis on investing in equities, which posted strong gains. Overall the world’s biggest pension funds have also begun growing again. This growth is, in part, symptomatic of bond-buying programmes by the world’s biggest central banks, known as quantitative easing, which have driven asset prices up in the decade since the financial crisis.Over the same period, low interest rates have made returns increasingly elusive for investors. Japan’s Government Pension Investment Fund is an example of an investor that has improved returns after a shift in strategy. In 2014, the GPIF signalled a change into riskier assets and away from low-yielding bonds.

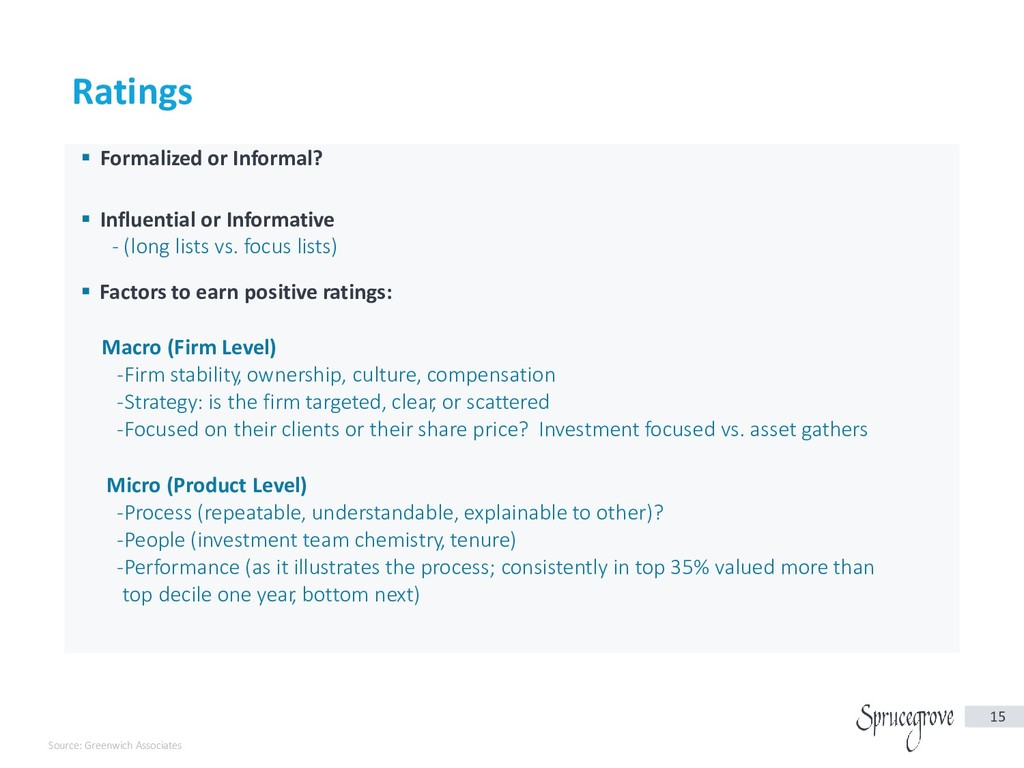

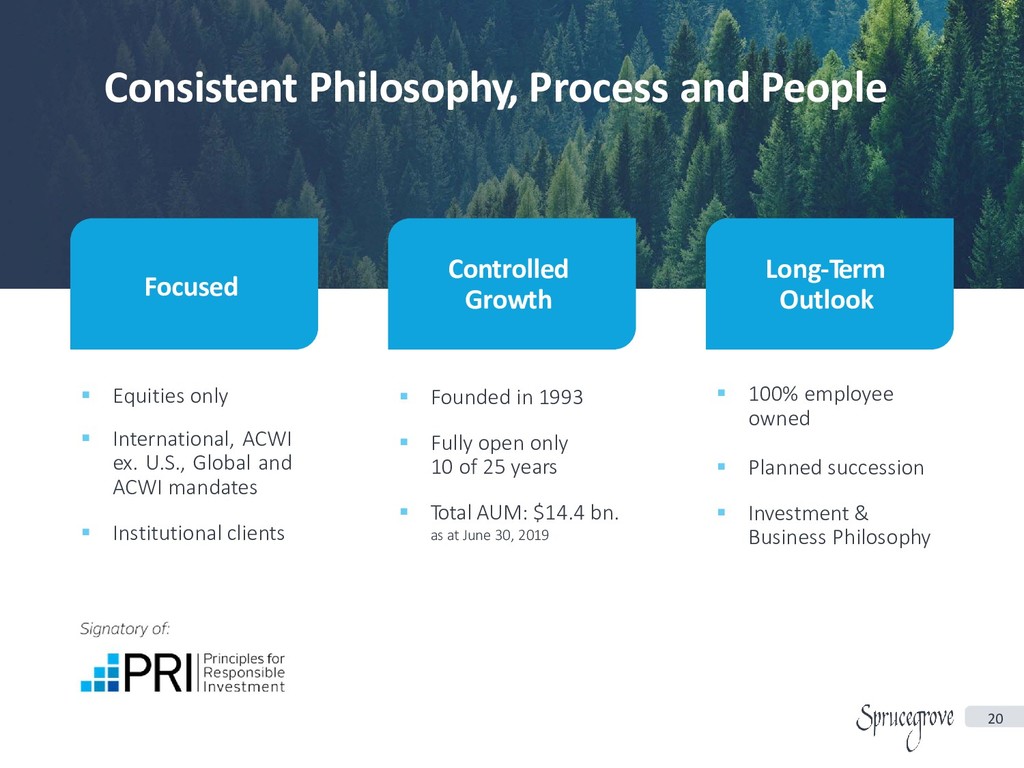

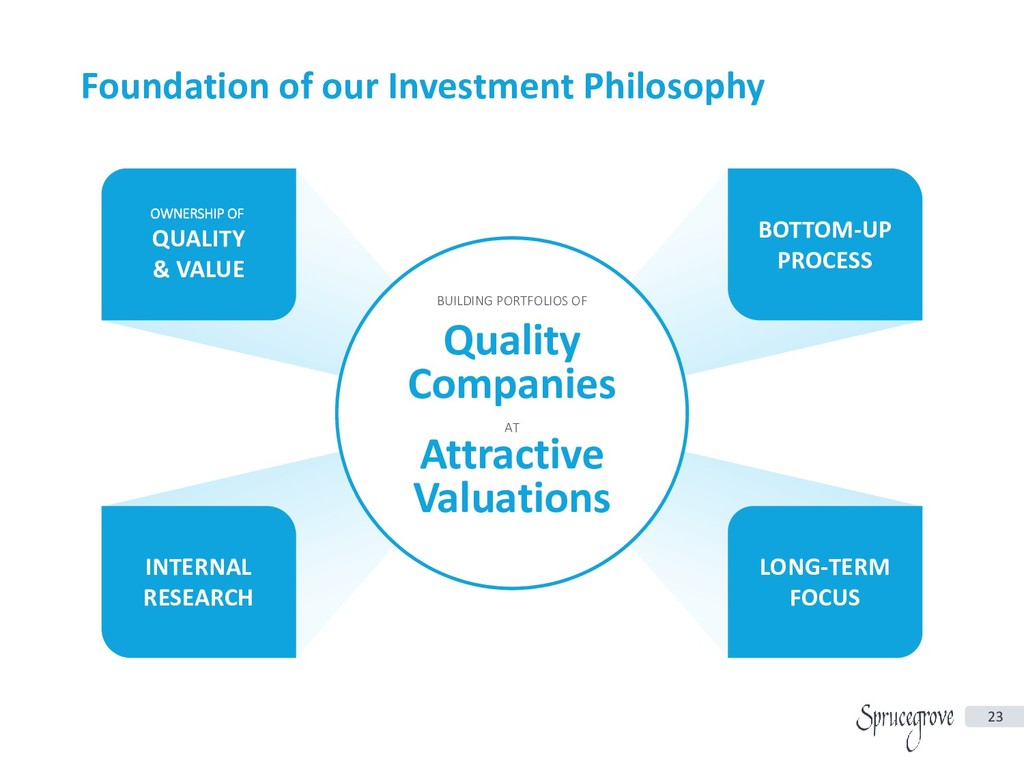

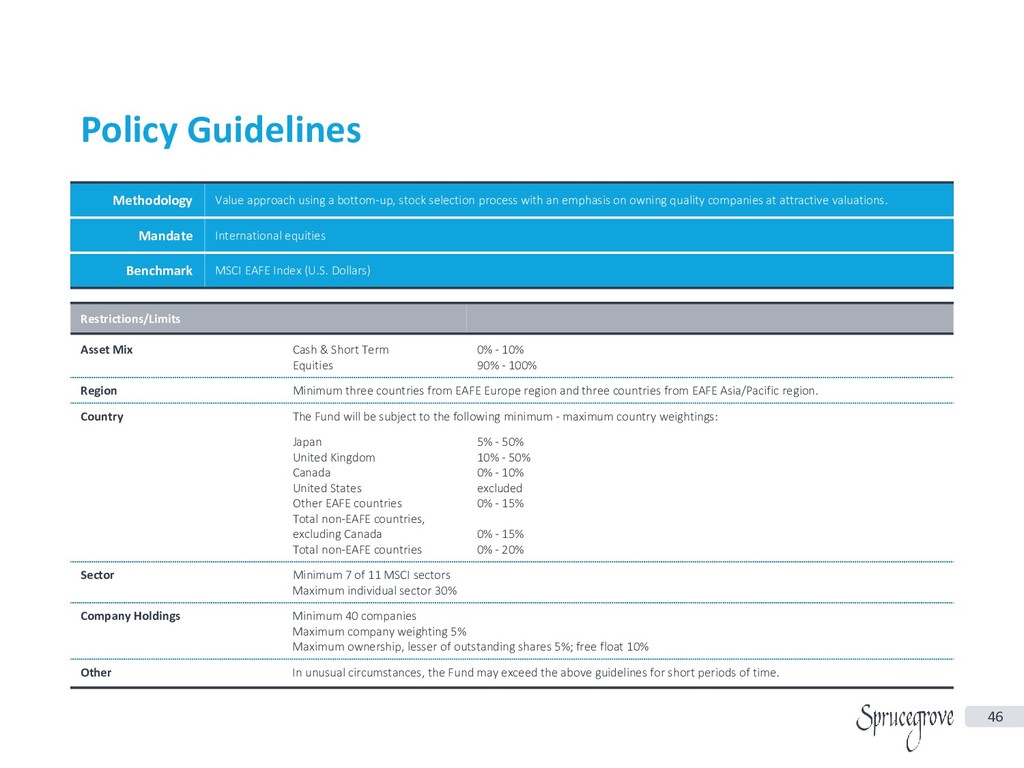

With that background, we look forward to introducing a value oriented investment approach by a Canadian based firm has demonstrated a proven track record of managing US and Canadian pension assets in global equity markets for over 30 years.

We invite you to join us for a presentation by an international equities manager that is focused on delivering outperformance over the benchmark with less risk in the long run.

10:00-10:15 Registration

10:15-10:20 Opning Remarks by Masataka Aoto, CFA (Board Director, Chair of Program Committee, CFA Society Japan)

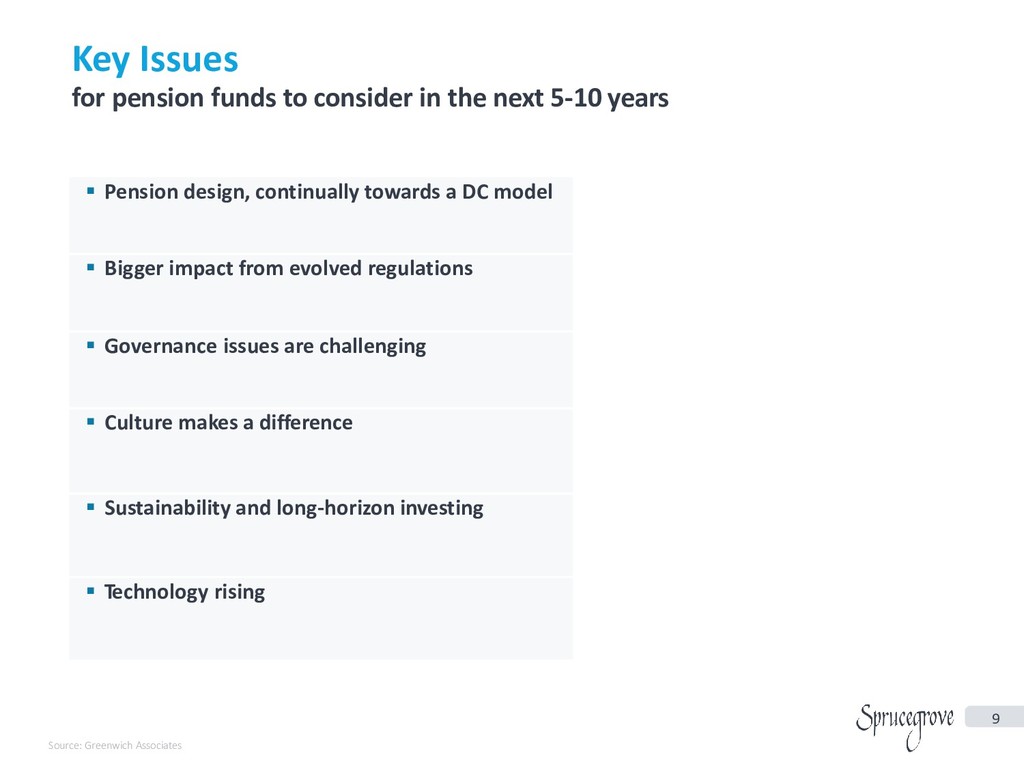

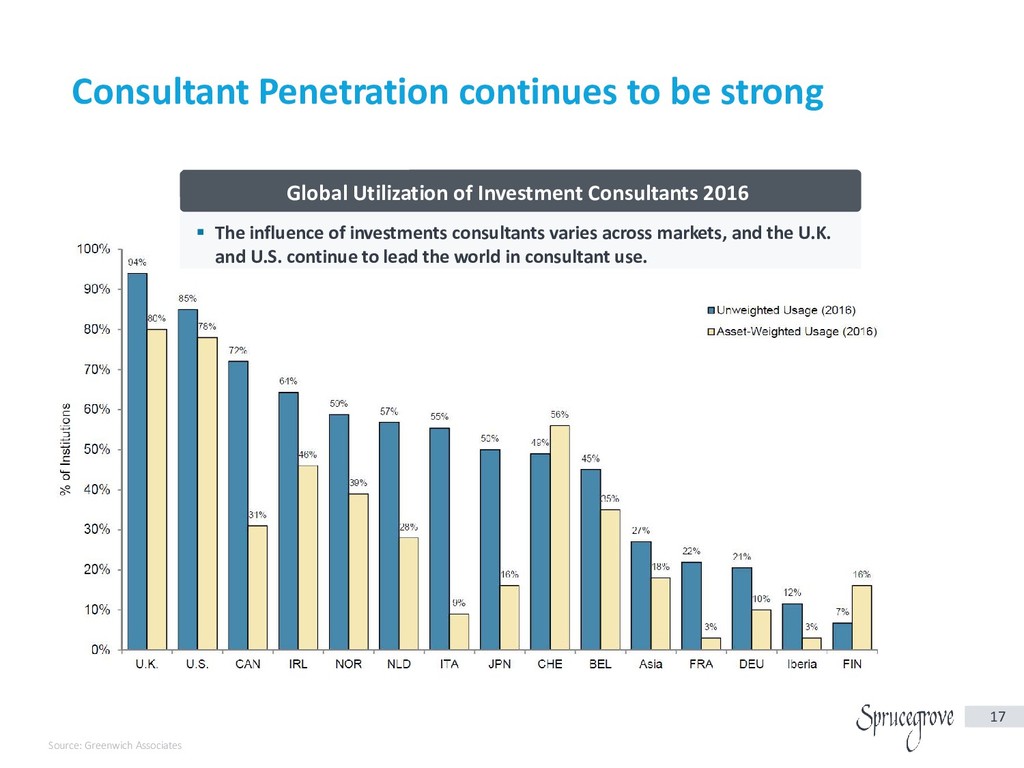

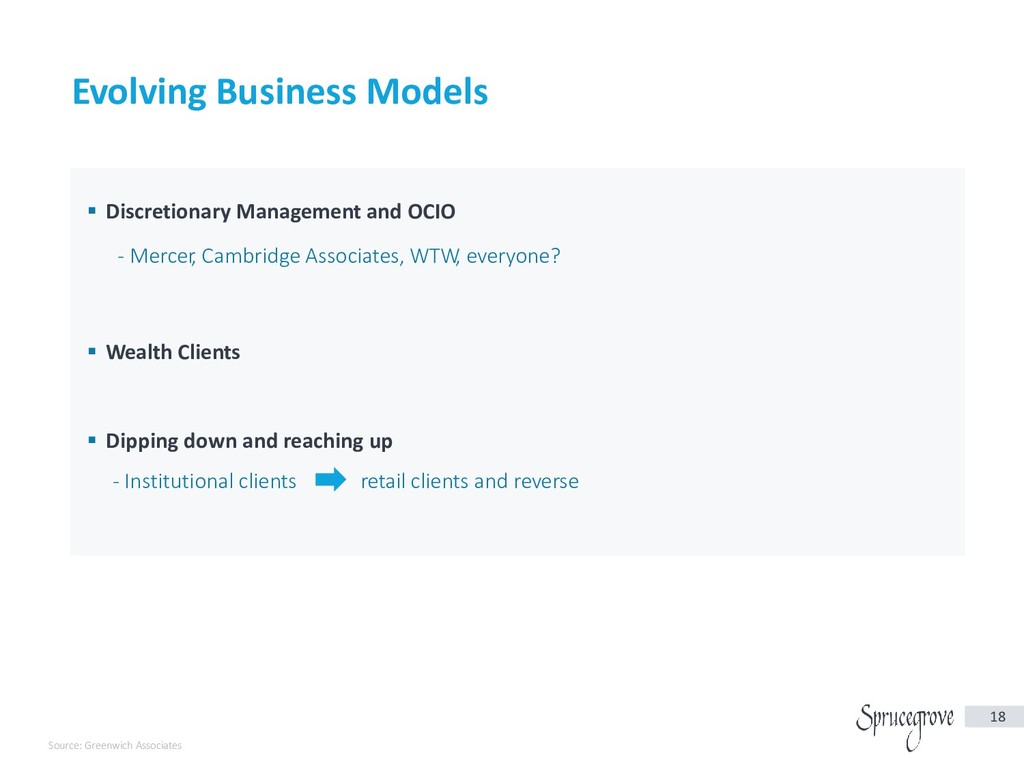

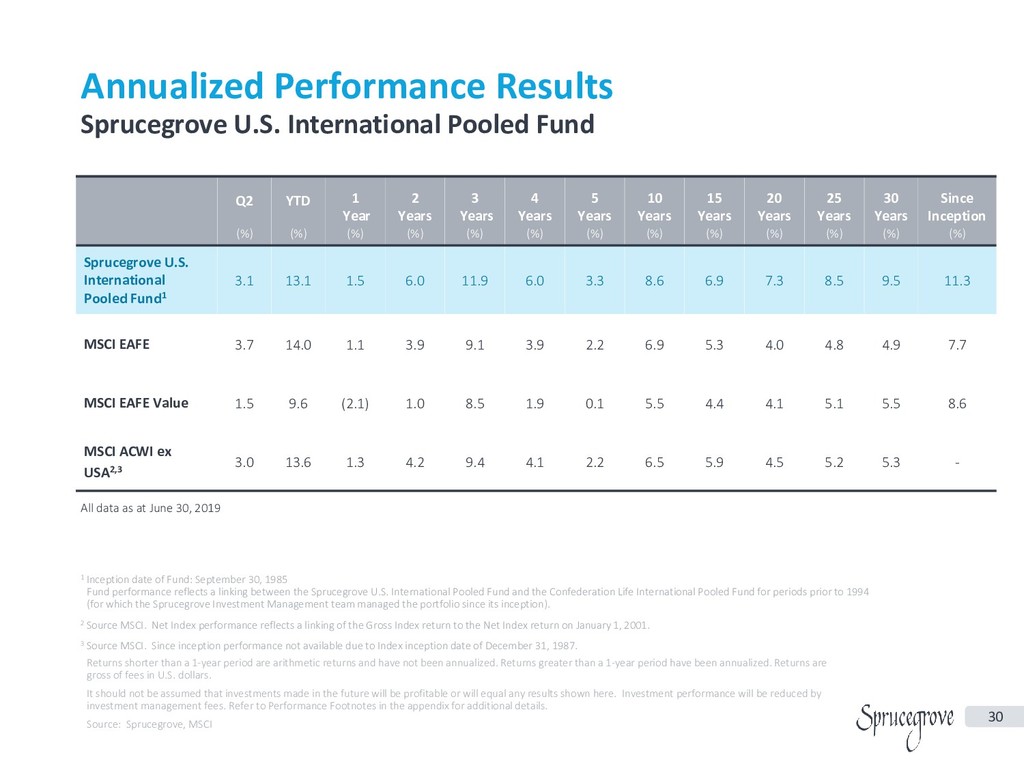

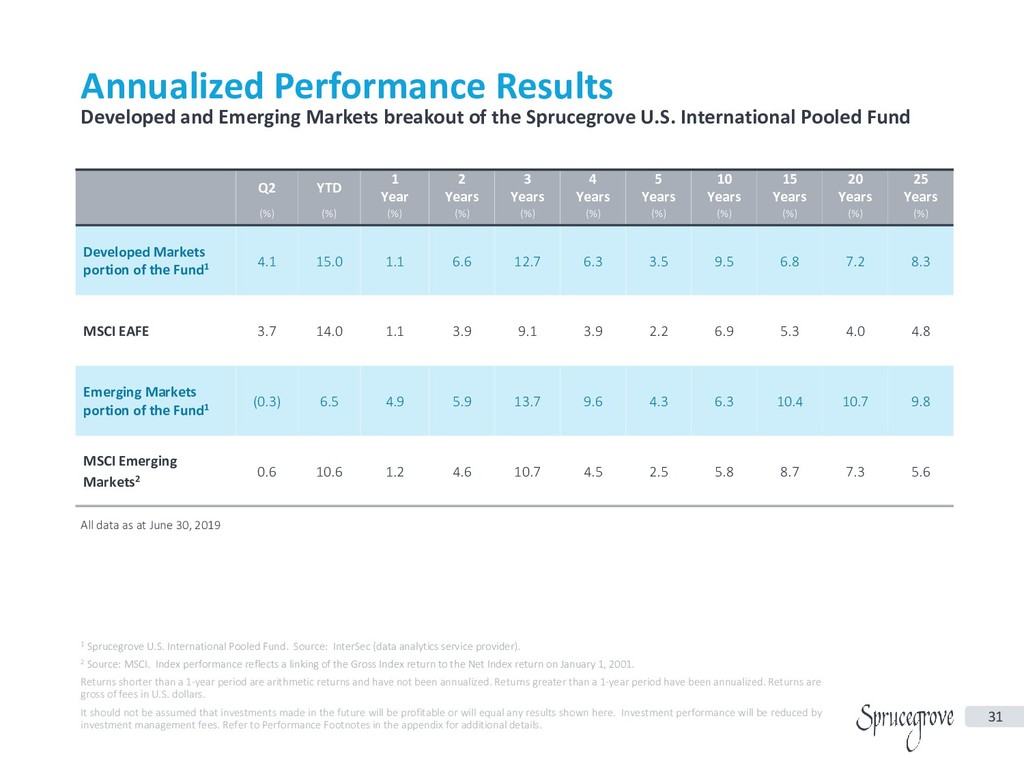

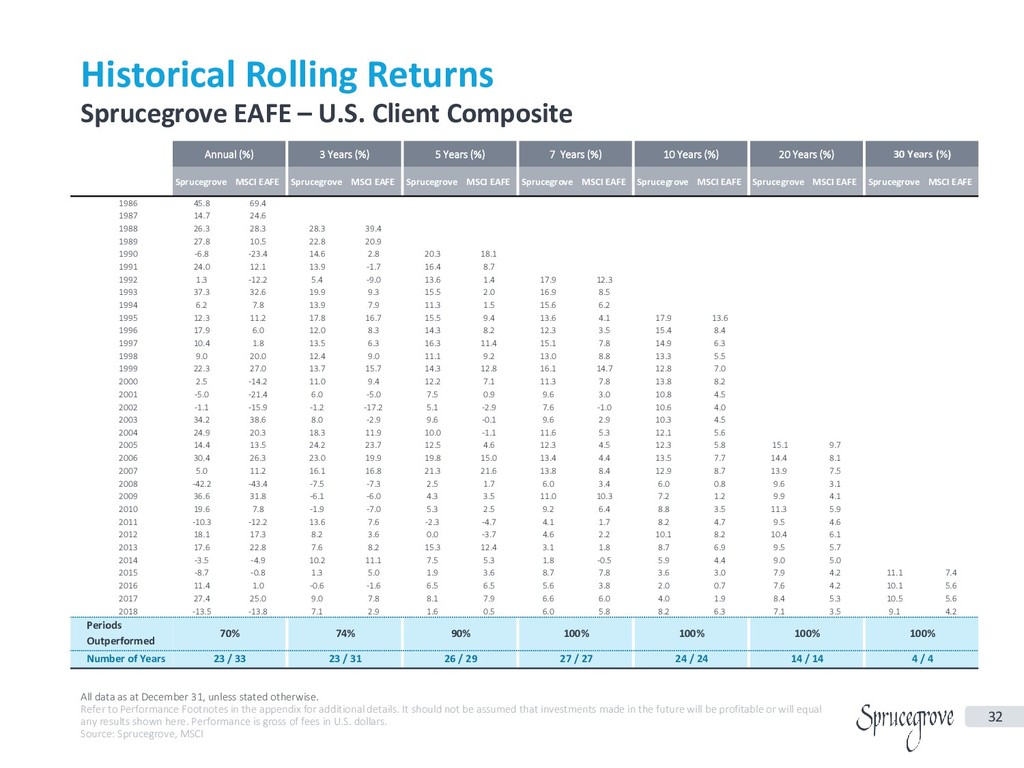

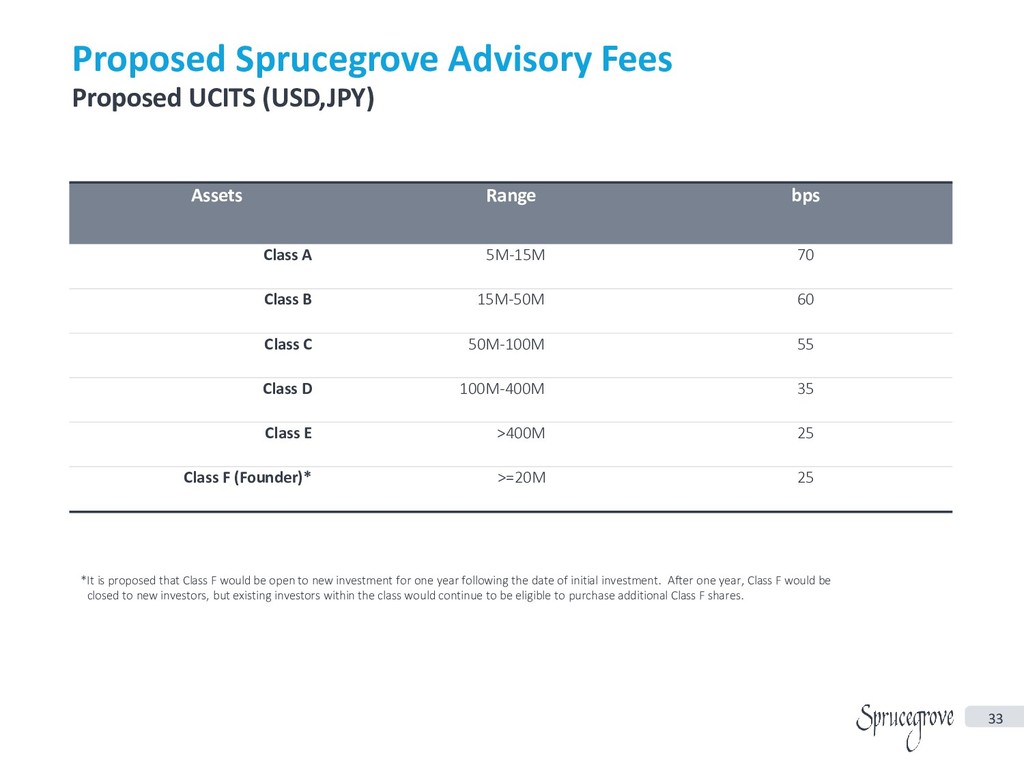

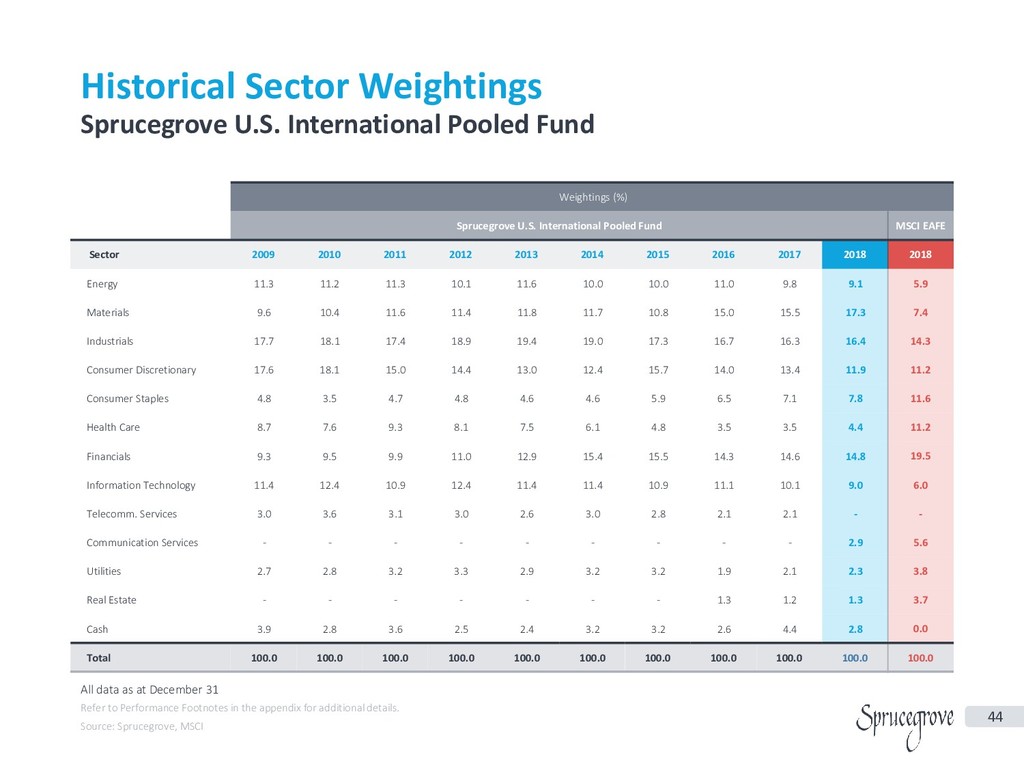

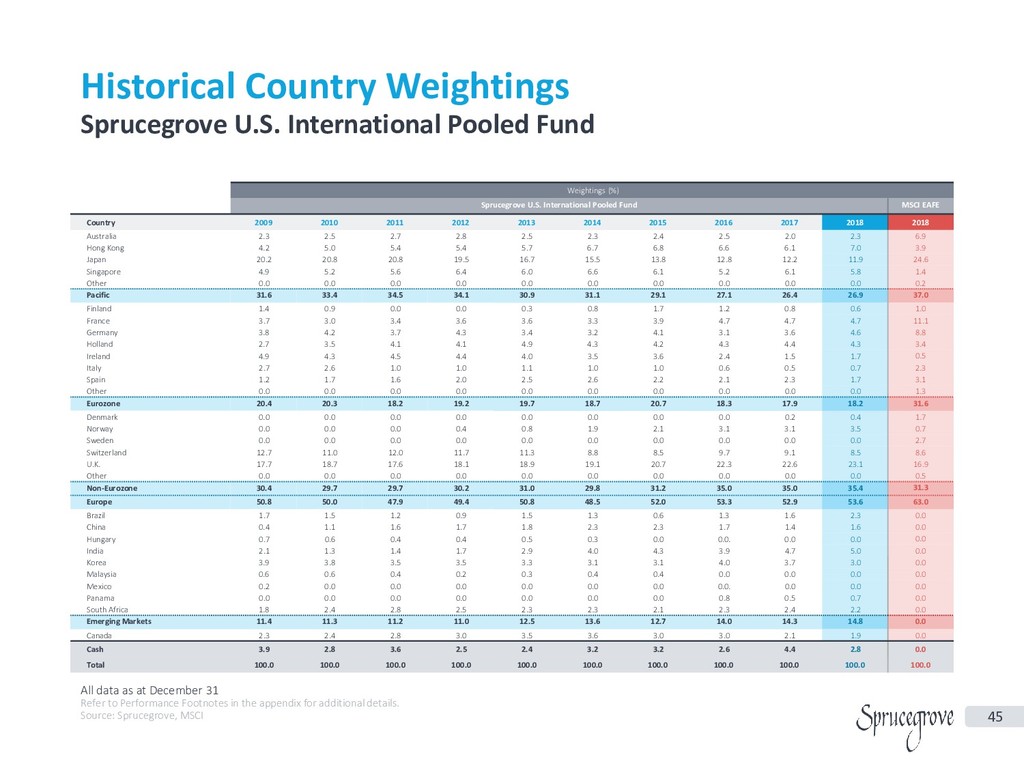

10:20-10:45 "Update investment policy & strategy of pension funds in North America" presented by Tasleem Jamal, CFA (Sprucegrove Investment Management)

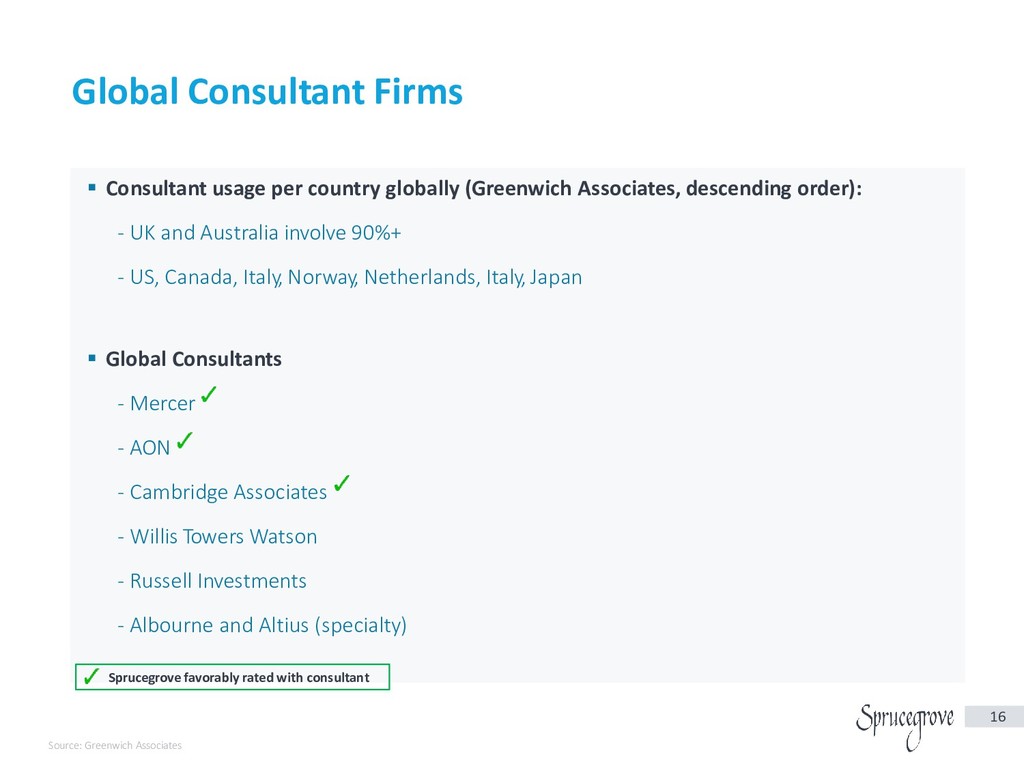

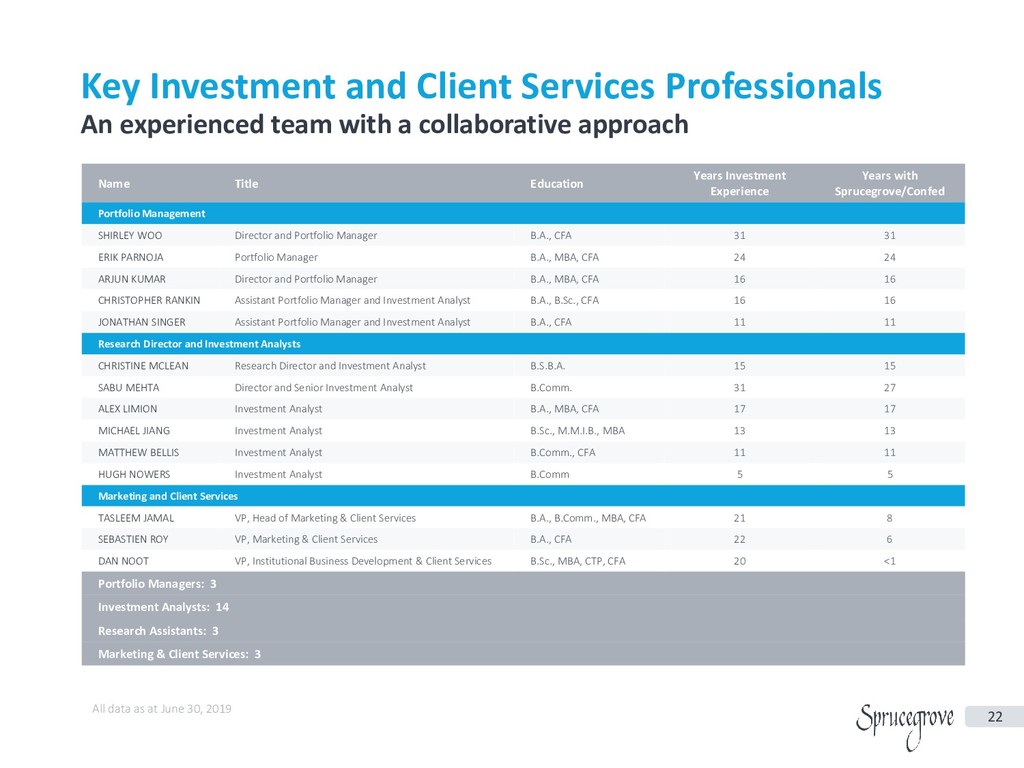

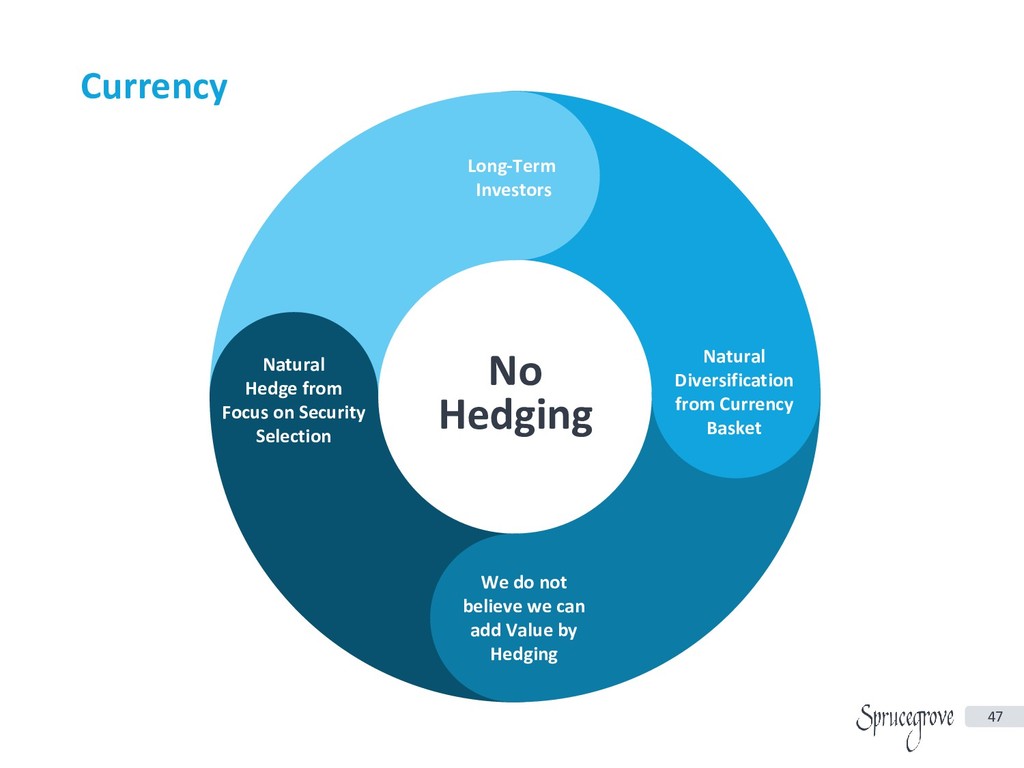

10:45-11:25 "Unique approach in global equity investment by a Canadian Manager" presented by Arjun Kumar, CFA (Sprucegrove Investment Management)

11:30-11:45 QA Session

11:45-11:50 Closing Remarks by Neil Vanwouw, President, The Canadian Chamber of Commerce in Japan

11:50-12:30 Networking Lunch

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![Sebastien Roy Vice President, Marketing & Client Services [email protected] 416.363.5854](https://files.speakerdeck.com/presentations/ce83823e6a31452abdffdf8a863a1962/slide_51.jpg){kind=link}