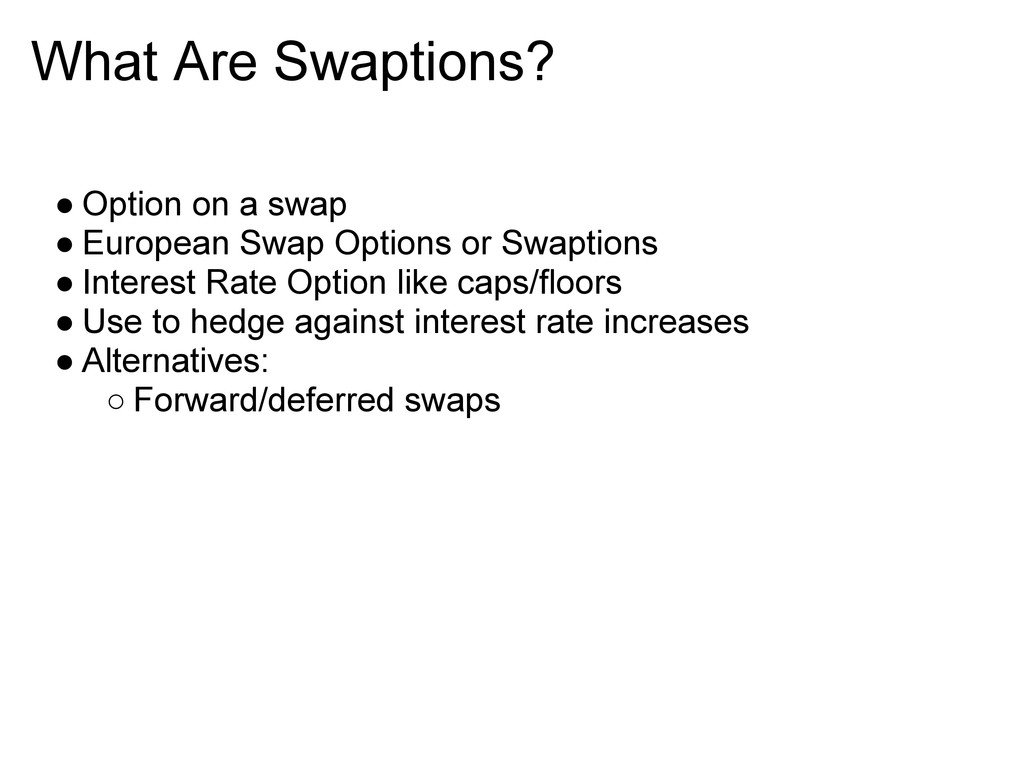

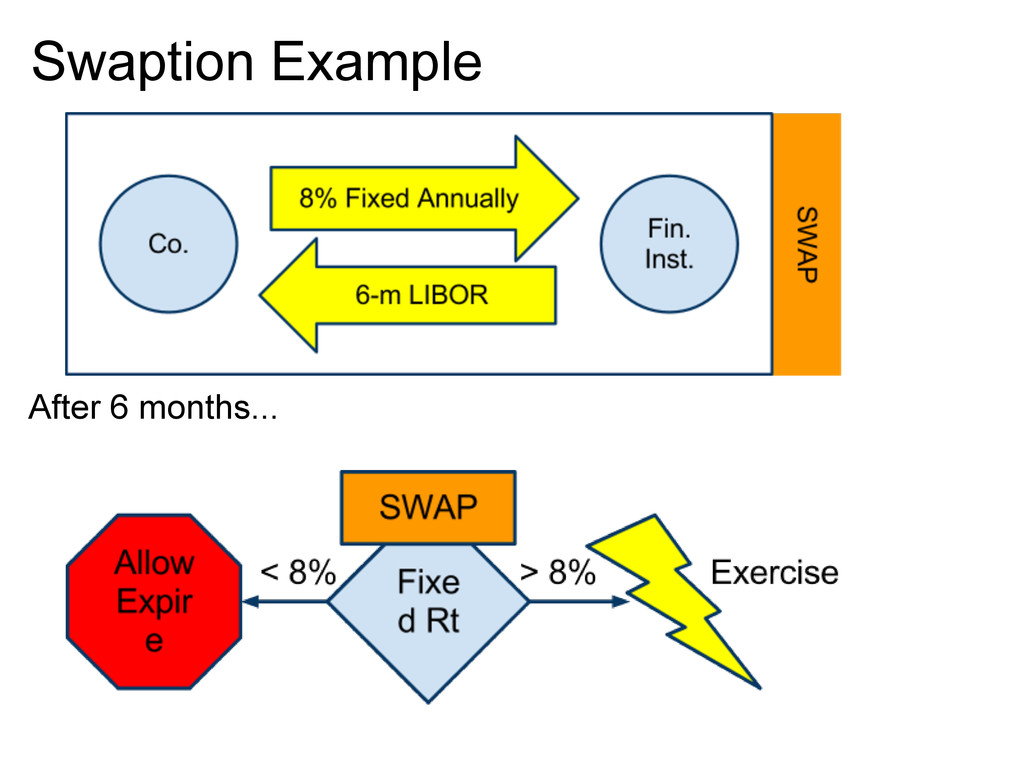

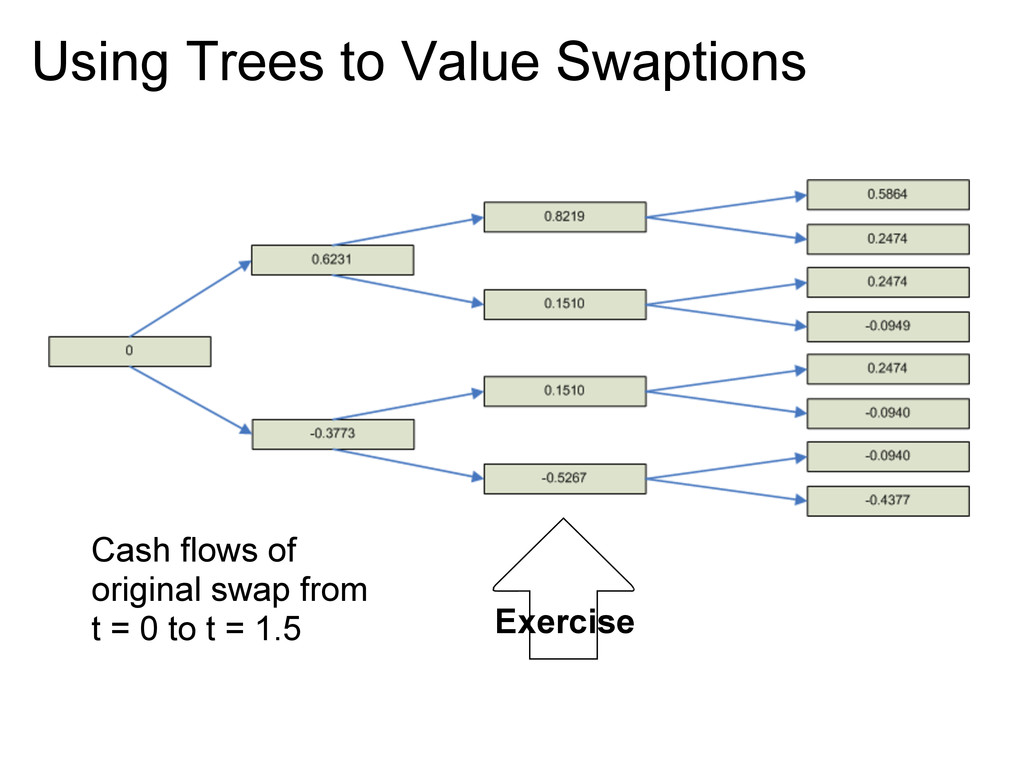

Swap Options or Swaptions • Interest Rate Option like caps/floors • Use to hedge against interest rate increases • Alternatives: ◦ Forward/deferred swaps

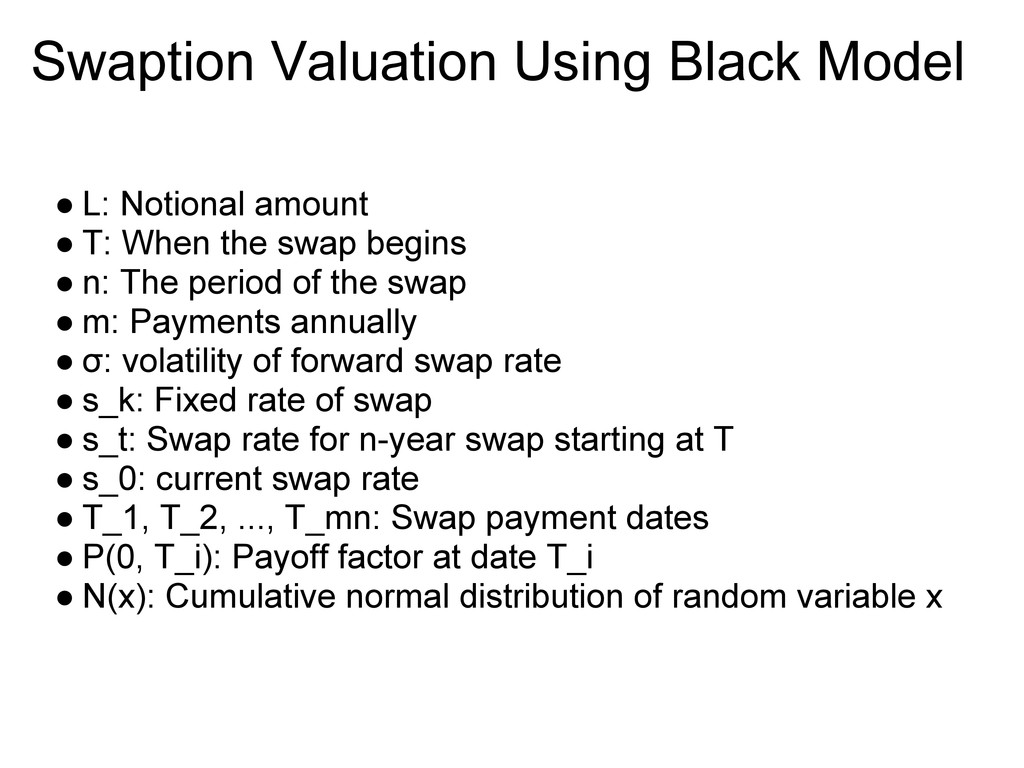

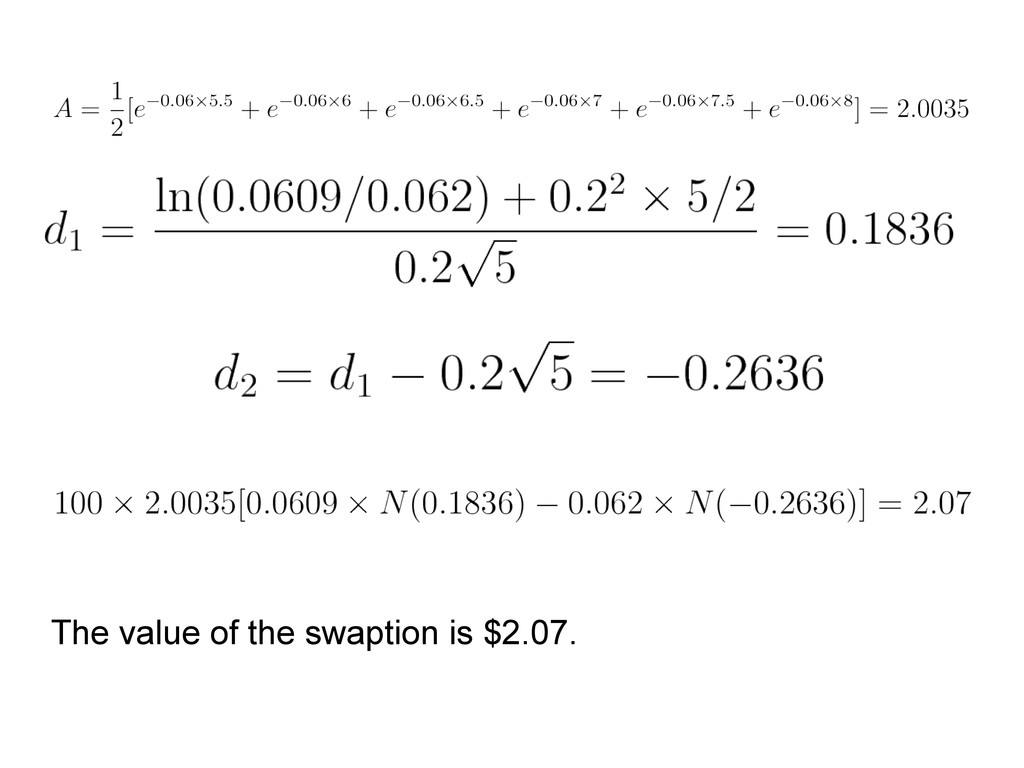

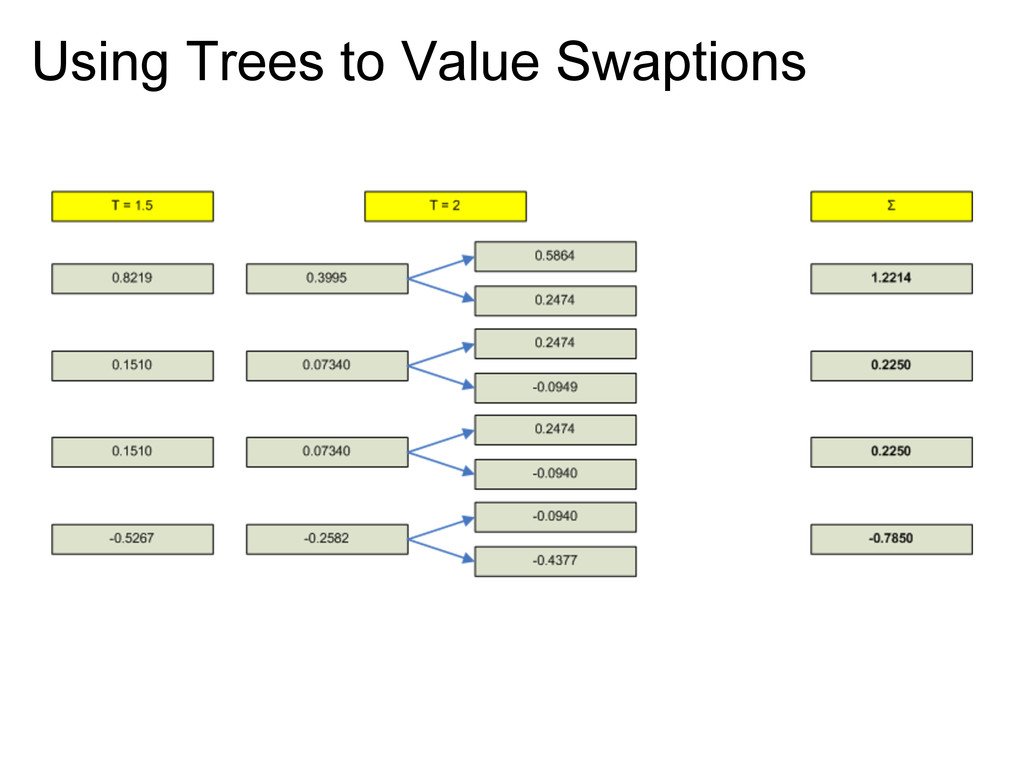

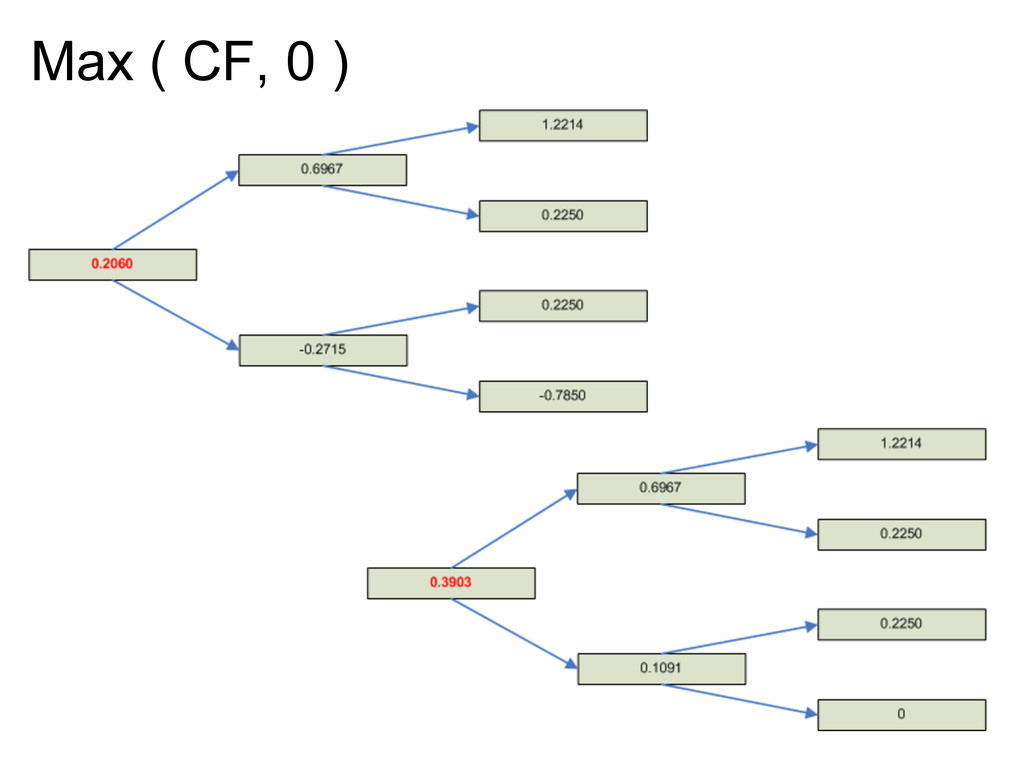

T: When the swap begins • n: The period of the swap • m: Payments annually • σ: volatility of forward swap rate • s_k: Fixed rate of swap • s_t: Swap rate for n-year swap starting at T • s_0: current swap rate • T_1, T_2, ..., T_mn: Swap payment dates • P(0, T_i): Payoff factor at date T_i • N(x): Cumulative normal distribution of random variable x

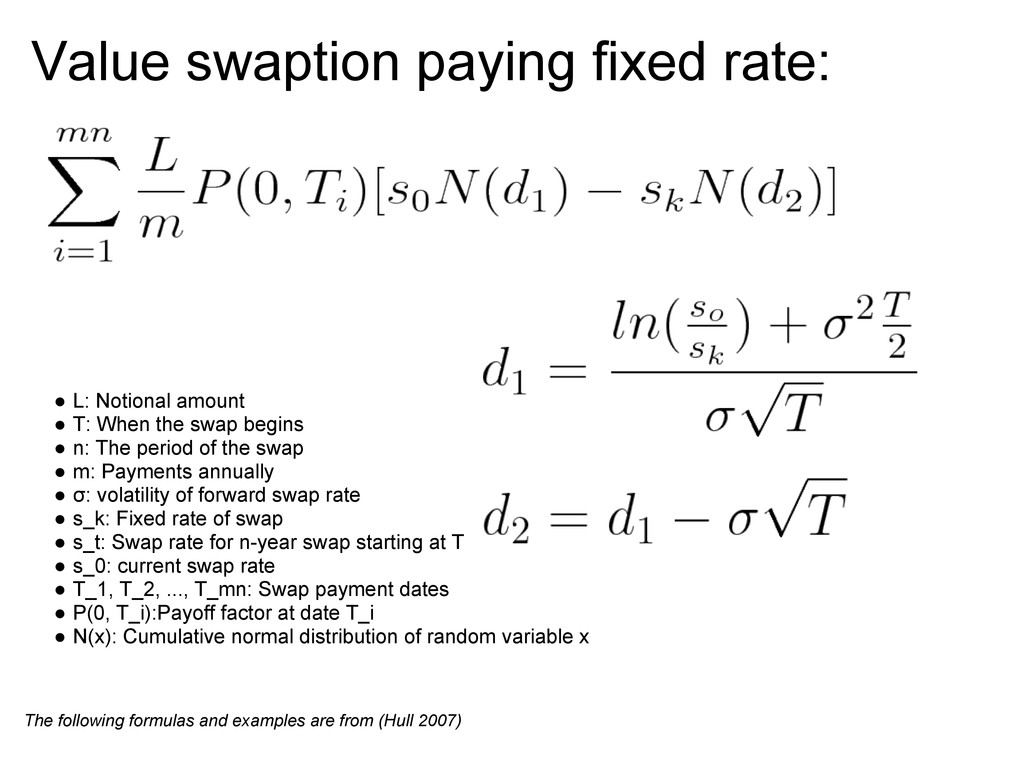

T: When the swap begins • n: The period of the swap • m: Payments annually • σ: volatility of forward swap rate • s_k: Fixed rate of swap • s_t: Swap rate for n-year swap starting at T • s_0: current swap rate • T_1, T_2, ..., T_mn: Swap payment dates • P(0, T_i):Payoff factor at date T_i • N(x): Cumulative normal distribution of random variable x The following formulas and examples are from (Hull 2007)

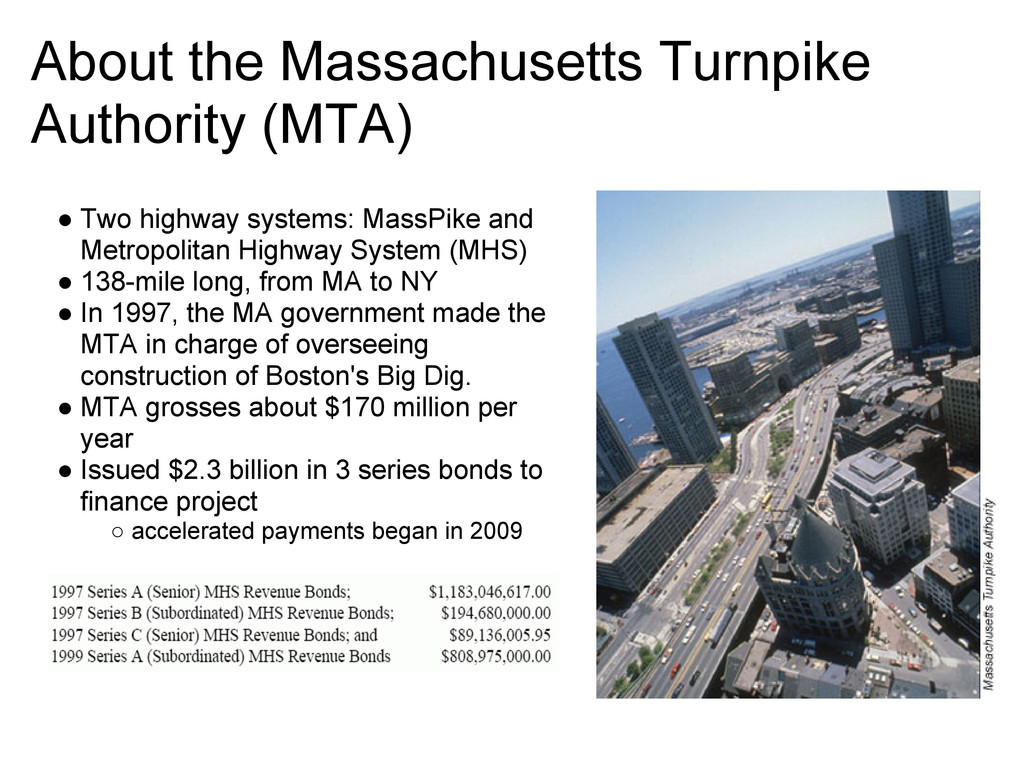

MassPike and Metropolitan Highway System (MHS) • 138-mile long, from MA to NY • In 1997, the MA government made the MTA in charge of overseeing construction of Boston's Big Dig. • MTA grosses about $170 million per year • Issued $2.3 billion in 3 series bonds to finance project ◦ accelerated payments began in 2009

led to the MTA entering into swaption agreements. • Purpose of the swaptions: ◦ additional revenue source that allowed them to: ▪ avoid the need for a toll increase in 2002 to 2008 ▪ achieve a 1.35 coverage ratio ▪ provide a modest capital program ▪ fund the Fast Lane discount program ▪ to offset the fixed-rate bonds they issued ◦ Total of $64 million received in additional revenue (UBS $29M,Lehman $35M) • But assumed risks for the next 35 years!

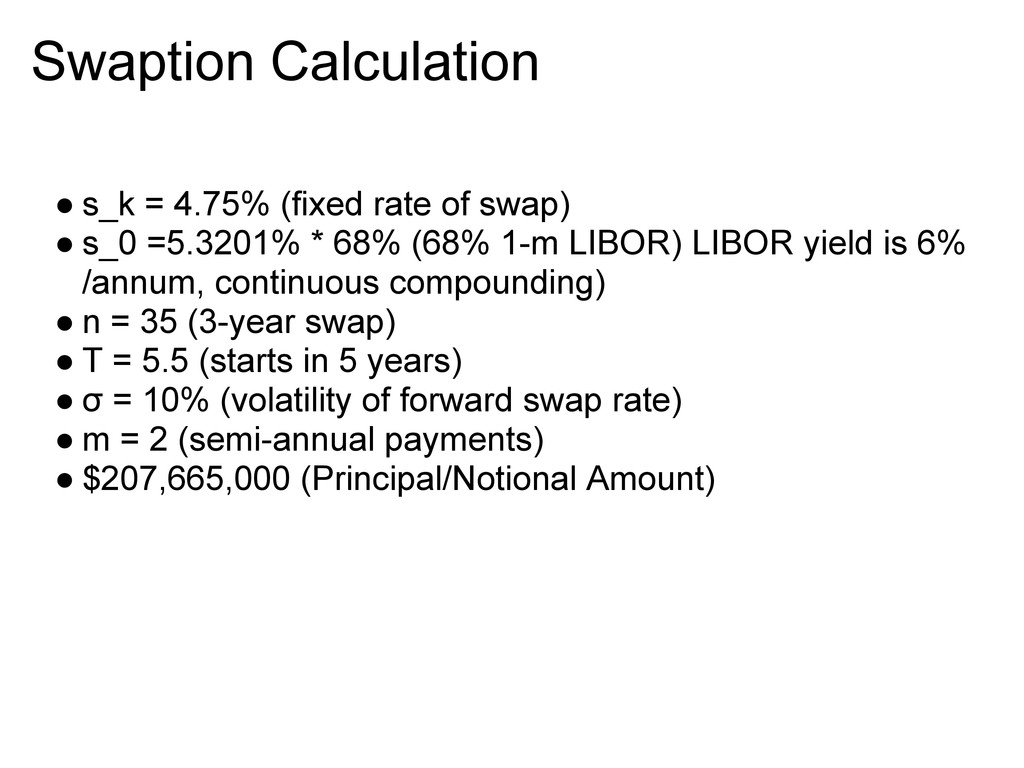

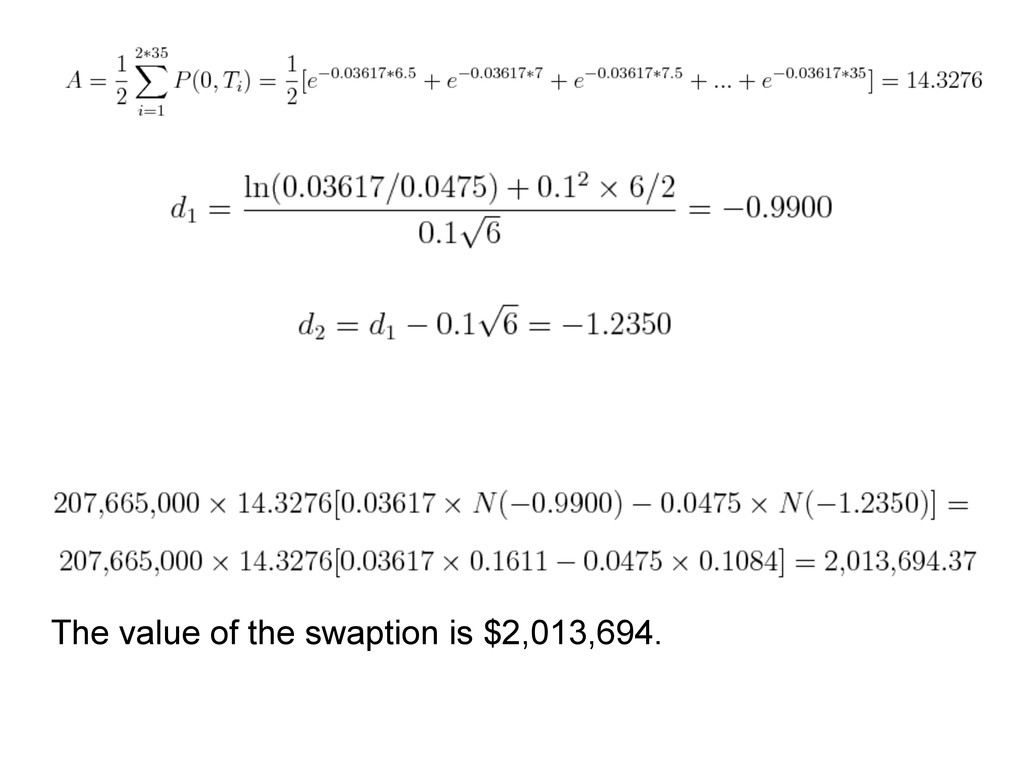

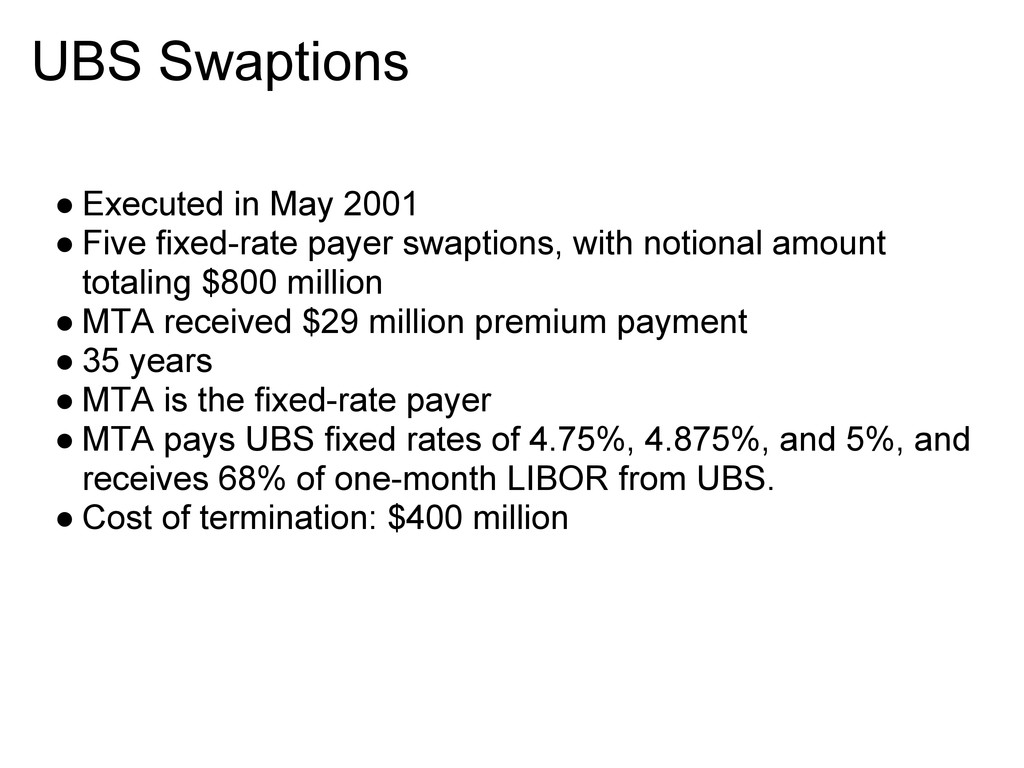

payer swaptions, with notional amount totaling $800 million • MTA received $29 million premium payment • 35 years • MTA is the fixed-rate payer • MTA pays UBS fixed rates of 4.75%, 4.875%, and 5%, and receives 68% of one-month LIBOR from UBS. • Cost of termination: $400 million

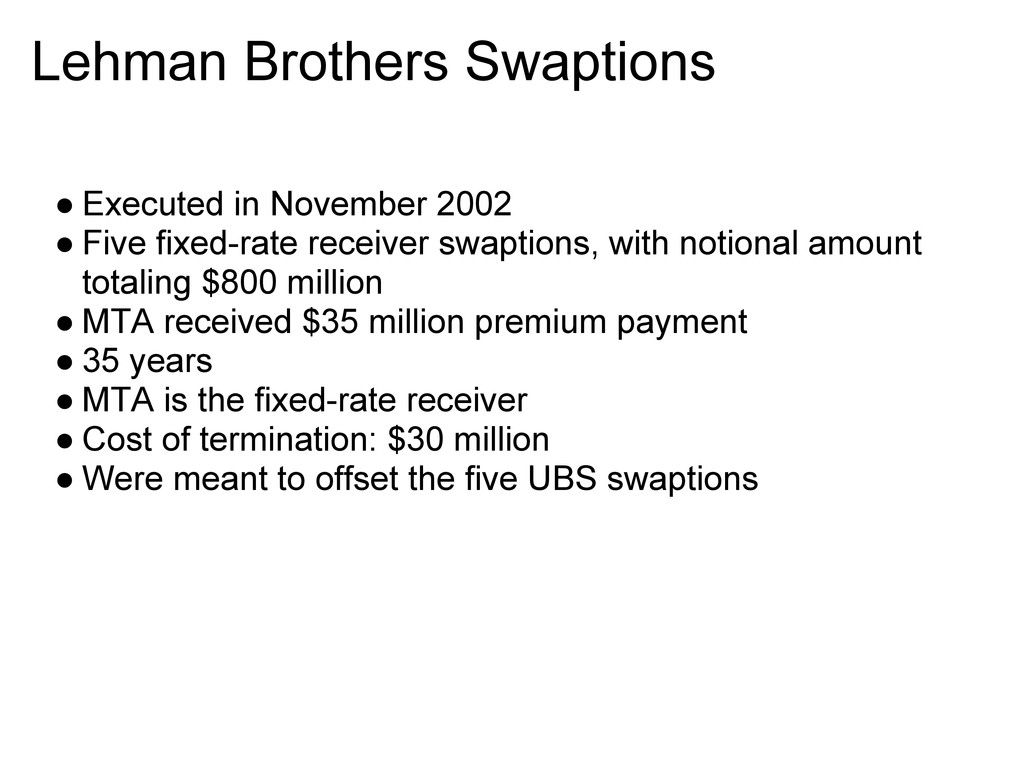

fixed-rate receiver swaptions, with notional amount totaling $800 million • MTA received $35 million premium payment • 35 years • MTA is the fixed-rate receiver • Cost of termination: $30 million • Were meant to offset the five UBS swaptions

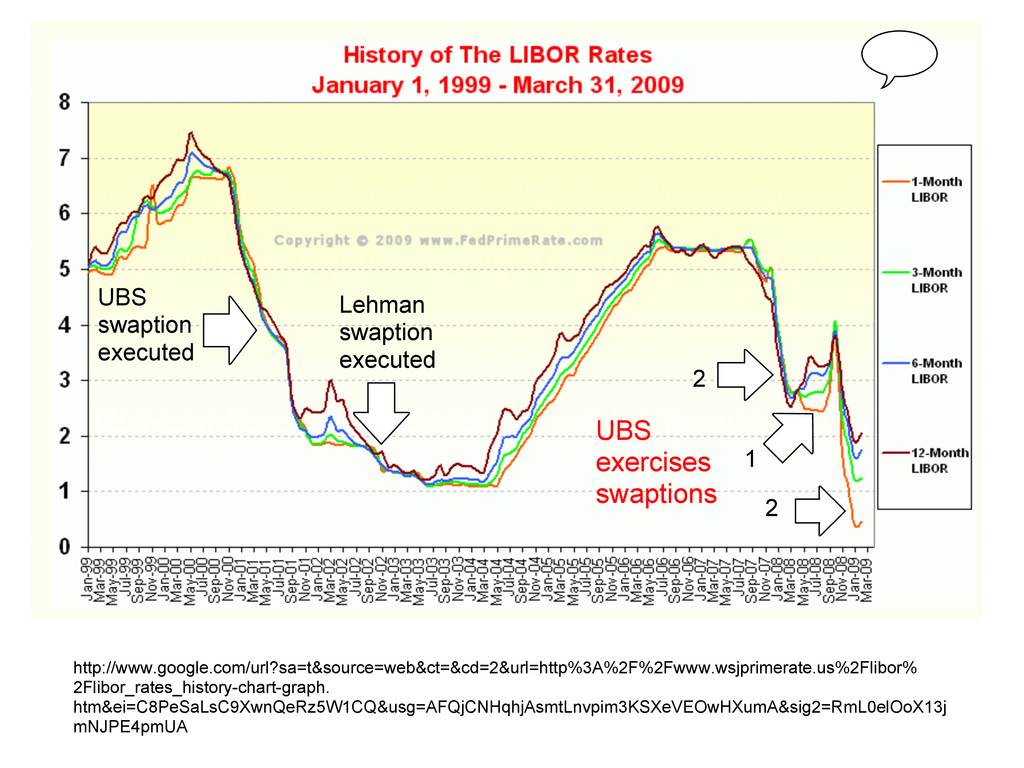

Jul 2008, Jan 2009 • MTA pays UBS fixed rates of 4.75%, 4.875%, and 5%, and receives 68% of one-month LIBOR from UBS. ◦ One-month LIBOR is now ~0.33%, compared to 4.56% three months ago. This means the MTA is receiving only 0.2244%. • The swaptions have increased MTA's fixed rate liabilities and is estimated to require $24 million in annual expenses by 2010. • Massachusetts government temporarily backed the MTA with a "general obligation" which expired in January 2009 ◦ MA government has a stronger credit rating (AA) than the MTA

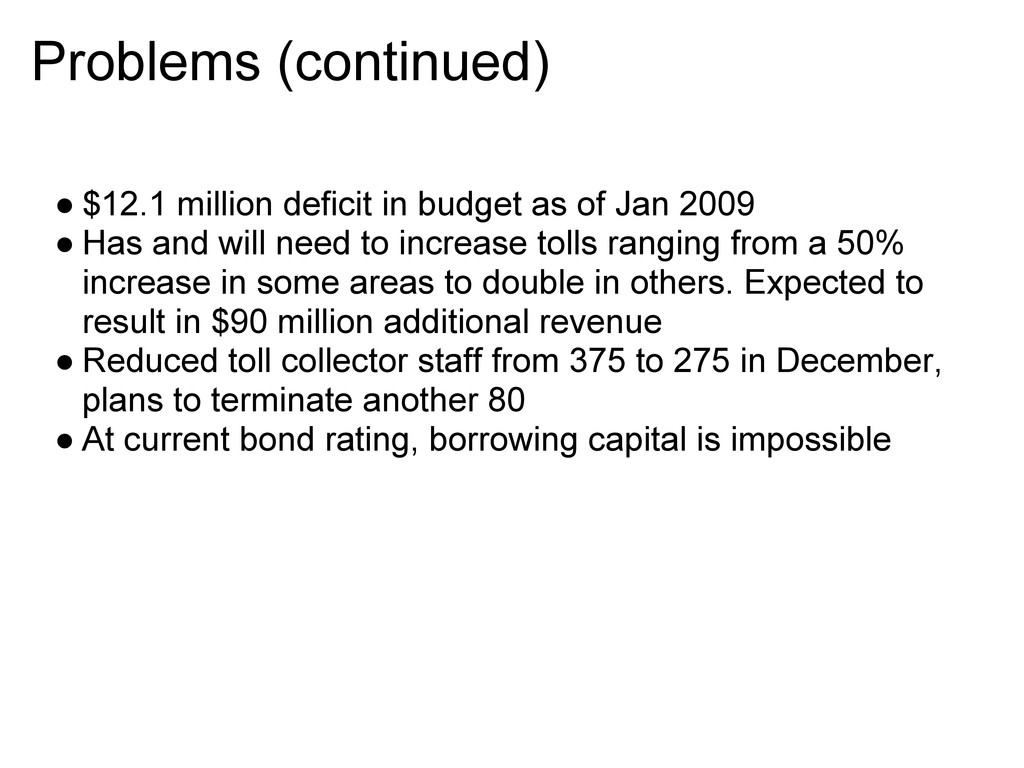

Jan 2009 • Has and will need to increase tolls ranging from a 50% increase in some areas to double in others. Expected to result in $90 million additional revenue • Reduced toll collector staff from 375 to 275 in December, plans to terminate another 80 • At current bond rating, borrowing capital is impossible

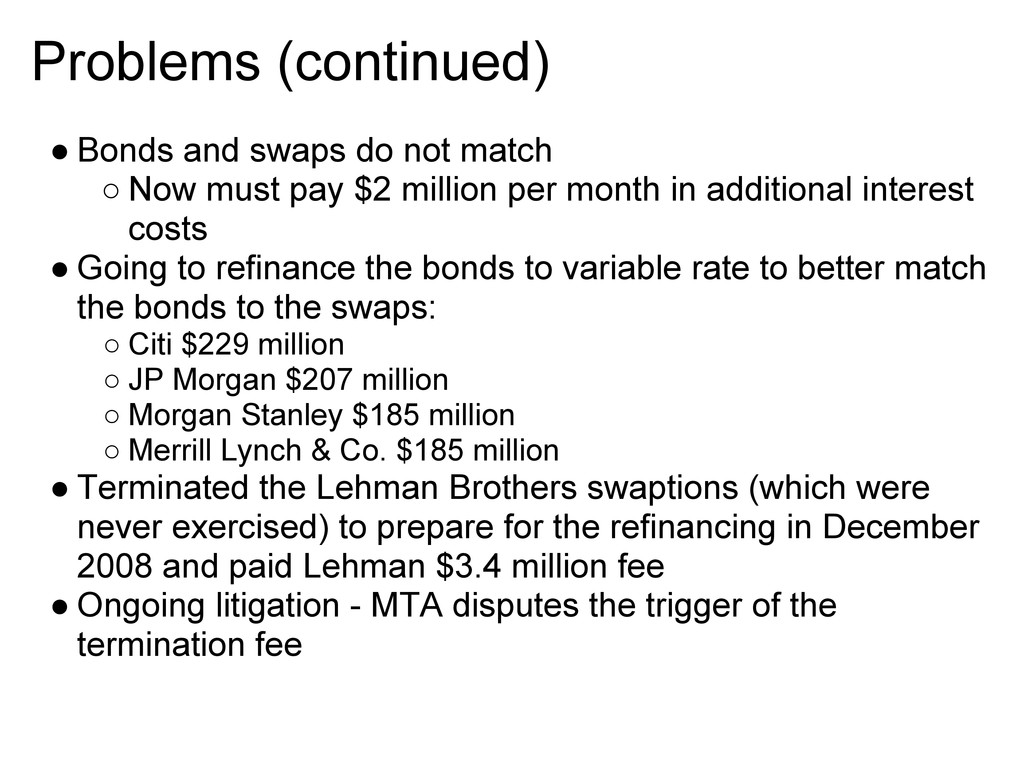

Now must pay $2 million per month in additional interest costs • Going to refinance the bonds to variable rate to better match the bonds to the swaps: ◦ Citi $229 million ◦ JP Morgan $207 million ◦ Morgan Stanley $185 million ◦ Merrill Lynch & Co. $185 million • Terminated the Lehman Brothers swaptions (which were never exercised) to prepare for the refinancing in December 2008 and paid Lehman $3.4 million fee • Ongoing litigation - MTA disputes the trigger of the termination fee

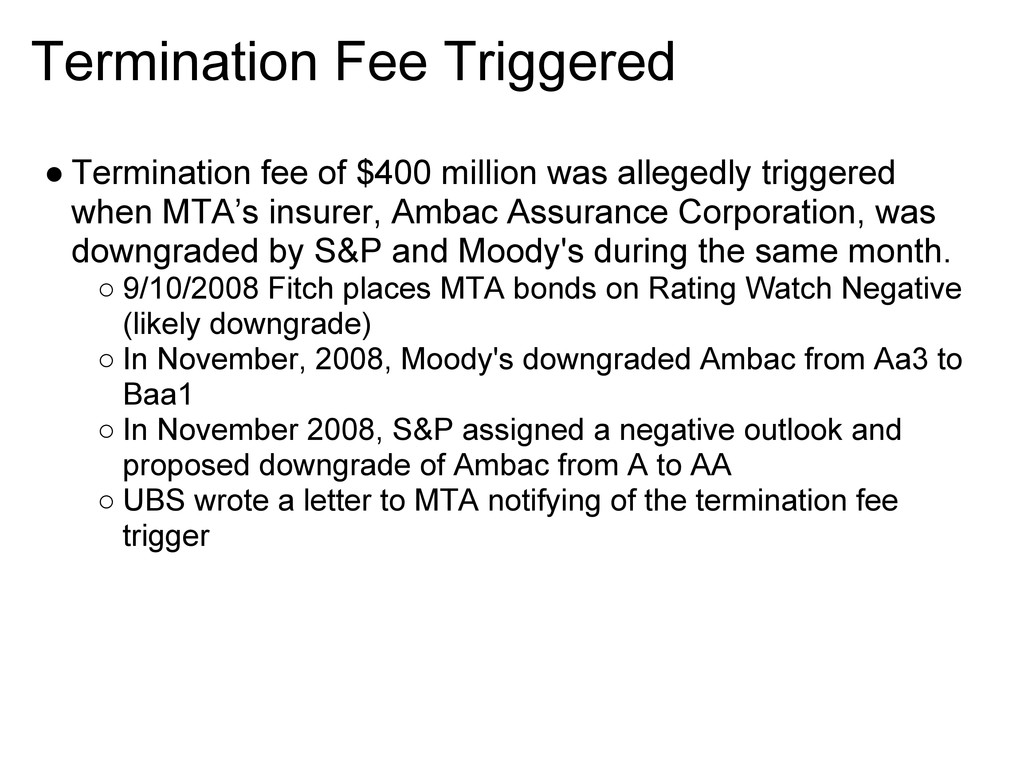

allegedly triggered when MTA’s insurer, Ambac Assurance Corporation, was downgraded by S&P and Moody's during the same month. ◦ 9/10/2008 Fitch places MTA bonds on Rating Watch Negative (likely downgrade) ◦ In November, 2008, Moody's downgraded Ambac from Aa3 to Baa1 ◦ In November 2008, S&P assigned a negative outlook and proposed downgrade of Ambac from A to AA ◦ UBS wrote a letter to MTA notifying of the termination fee trigger

Sons, Inc., 2001 • "Fitch Puts Massachusetts Turnpike Authority's Metro Highway System Revs on Watch Negative." Reuters. 9 Sep 2008. 28 Mar 2009. <http://www.reuters.com/article/pressRelease/idUS188113+09-Sep-2008+BW20080909>. • Hull, John C.. Options, Futures, and Other Derivatives. 6. New Delhi: Prentice-Hall, 2007. • "Massachusetts Turnpike reducing toll collectors from 375 to 275." Tollroad News. 12 Dec 2008. 18 Mar 2009. <http://www.tollroadsnews.com/node/3882>. • "Fitch Comments on Massachusetts Turnpike Auth MHS Swaptions." Business Wire. 19 Dec 2008. 18 Mar 2009. <http://www.allbusiness.com/banking-finance/financial-markets-investing/5973127-1.html>. • "Toll Increase - Frequently Asked Questions." MTA - Turnpike News. 15 Dec 2008. 18 Mar 2009. <http://www.masspike.com/user-cgi/news.cgi?dbkey=313&type=Press%20Release&src=news>. • "Fitch Affirms MA Turnpike Auth MHS Sr. Bnds at 'BBB+'/Sub. Bnds at 'BBB'; Stable Outlook." The Free Library by Farlex. 28 Jul 2005. 18 Mar 2009. <http://www.thefreelibrary. com /Fitch+Affirms+MA+Turnpike+Auth+MHS+Sr.+Bnds+at+%27BBB%2B%27%2FSub.+Bnds+at...- a0134595894>. • Kaske, Michelle. "MassPike Swap Payment a Looming Threat." The Bond Buyer. 14 Jan 2009. 18 Mar 2009. <http: //www.bondbuyer.com/article.html?id=20090113QT0BC3WK>. • "Massachusetts Turnpike Authority, Financial Statements, Required Supplementary Information, and Supplementary Schedules, December 31, 2003 and 2002." KPMG. 17 Sep 2004. • "Transportation Finance in Massachusetts: An Unsustainable System. Findings of the Massachusetts Transportation Finance Commission." 28 Mar 2007. • "Massachusetts Turnpike Authority Request for Proposals. Legal Services for Potential Claim(s) Against Investment Bank/Swap Counterparty, Financial Advisor, Bond Insurer and/or Rating Agencies." 29 Jan 2009. • "Ehrlich: Understanding 'swaptions' coming down the Pike." The Milford Daily News. 26 Mar 2009. 10 Apr 2009. <http: //www.milforddailynews.com/opinion/x759739191/Ehrlich-Understanding-swaptions-coming-down-the-Pike?view=print>. • http://www.wsjprimerate.us/libor/libor_rates_history.htm

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}