Milano-Bicocca University ICC Italia Conference, Rome, November 10, 2016 [email protected] @Ferdinando1970 http://www.slideshare.net/Ferdinando1970 https://it.linkedin.com/in/ferdinandoametrano

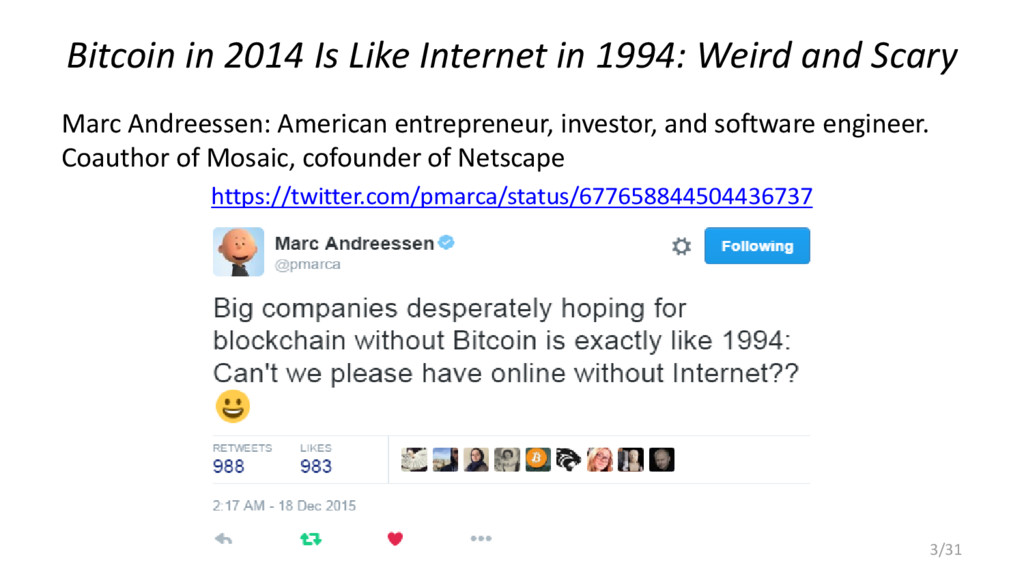

Scary Marc Andreessen: American entrepreneur, investor, and software engineer. Coauthor of Mosaic, cofounder of Netscape https://twitter.com/pmarca/status/677658844504436737 3/31

and services • Offered in the late ‘90s and early ‘00s by Compuserve, AOL (and to some extent MSN) • Corporates wanted to go online, but not in the wild unregulated internet, populated by anonymous agents • They eventually realized that perceived risks, which are real, are outweighed by benefits 4/31

however lags well behind the hype, amongst practitioners, policy makers and industry commentators alike. ‘Blockchain’ technology seems to promise major change for capital markets and other financial services – some say it may ultimately prove to be as important an innovation as the internet itself – but few can say exactly how or why. Michael Mainelli, Alistair Milne (2016) The Impact and Potential of Blockchain on the Securities Transaction Lifecycle http://ssrn.com/abstract=2777404 5/31

1. Game theory 2. Cryptography 3. Computer networking and data transmission 4. Economic and monetary theory Mainly not a technology, a cultural paradigm shift instead 6/31

blocks] • An append-only sequential data structure • New blocks can only be appended at the end of the chain • To change a block in the middle of the chain, all subsequent blocks need to be changed • Very inefficient compared to a relational database 7/31

transactions • Massively duplicated across network nodes • Shared with a P2P file transfer protocol • Updated by peculiar nodes, known as miners, appending new blocks of transactions 8/31

and clearing. • Miners perform the additional work required for settlement. How do they reach consensus on the transaction history? • Consensus in a distributed network with faulty (or malicious) nodes is a very hard problem known as Byzantine General Problem 9/31

incentive for the mining nodes to be honest • Miners are compensated for their proof-of- work using seigniorage revenues, i.e. with issuance of new bitcoins 10/31

asset available to reward miners Appointed validator officials required Why should validators use a blockchain, i.e. a subpar data structure, instead of a database? 11/31

of Blockchain and Virtual Currencies, Intesa Sanpaolo, discusses the relationship between bitcoin and blockchain, and outlines how banks can stay ahead of this evolving landscape. 12/31

by the first (and most relevant so far) blockchain • It exists only as scriptural asset, i.e. validated transaction recorded on the blockchain • It is a bearer instrument: the (private key) holder is the actual effective owner 13/31

realm, as nothing else before • It can be transferred but not duplicated • (i.e. it can be spent, but not double-spent) Bitcoin is digital gold: this is the brilliant groundbreaking achievement by Satoshi Nakamoto 14/31

• Its adoption was not centrally planned • For centuries it has been the most successful form of money • It has bootstrapped all monetary systems we know of • It has been surpassed by other kind of money without becoming obsolete bitcoin • Its adoption has not been centrally planned • It is the most successful form of cryptocurrency • It will bootstrap new monetary systems • It might be surpassed by more advanced type of cryptocurrencies without becoming obsolete 15/31

value (legal tender, social contract) • Currency based on paper/ink security • Discretionary governance • Wicksellian interest-rate approach bitcoin • No intrinsic value (digital gold) • Currency based on math/cryptographic security • Algorithmic governance • Deterministic supply 16/31

• Everything else tracked with blockchain technology is somebody’s liability A healthy digital transactional economy requires a native digital asset to be used for payment and collateral; it makes no sense to only have liabilities! the same is true for other native digital assets (ethereum, litecoin, etc.) of less secure blockchains 17/31

email was the killer Internet app • Impossible to imagine Google, Facebook, Amazon • 2016: bitcoin is the killer Blockchain app • More ambitious apps will be built on blockchain, but they have not been really imagined yet, and they will need a native digital asset 18/31

hashed to producing a short unique identifier, equivalent to its digital fingerprint. • Such a fingerprint can be associated to a bitcoin transaction (irrelevant amount) and hence registered on the blockchain • Blockchain immutability provides non-repudiable time-stamp, proving the existence of the data file in that specific status at that moment in time • This generic process is even undergoing some standardization to achieve third party auditable verification: broker-dealers could use it to satisfy regulatory prescriptions 19/31

is preserved by a computation power unparalleled in human history • Other transactional networks can tap into this security via anchoring (i.e. periodic time- stamping of the network status) • Bitcoin miners as global outsourced decentralized security of the future 20/31

and digital IDs [not really blockchain] As for the rest, it is basically hype. Questions always to be answered: • Can be achieved with a database? • What consensus is required? (distributed, bilateral, centralized) • What kind of security is required: preventive, detective, or corrective? (ok / yes today, probably not in the future/ no) • Blockchain is absolutely not suited for storing large amount of data 21/31

project intended to bring blockchains to finance” • Its Distributed Ledger Group is developing a proprietary platform, named Corda: “Corda is a distributed ledger platform […] we are not building a blockchain” • A revamped SWIFT secure messaging protocol on cryptographic proof & bilateral ledger steroids? 24/31

validated and cleared, then settled shortly thereafter, automatically without a central authority • In the financial world, cash transactions only are cleared and settled automatically without a central authority 25/31

execute, clear and settle in days • Not a technological problem • Consensus by reconciliation of multiple independent ledgers: a checks and balances system that allows for prescriptions, corrections, and restrictions 26/31

short selling and netting almost impossible • Instant settlement (e.g. for payments) has costs: who should pay for them? • Cash-on-the-ledger is imperative for Delivery vs Payment 27/31

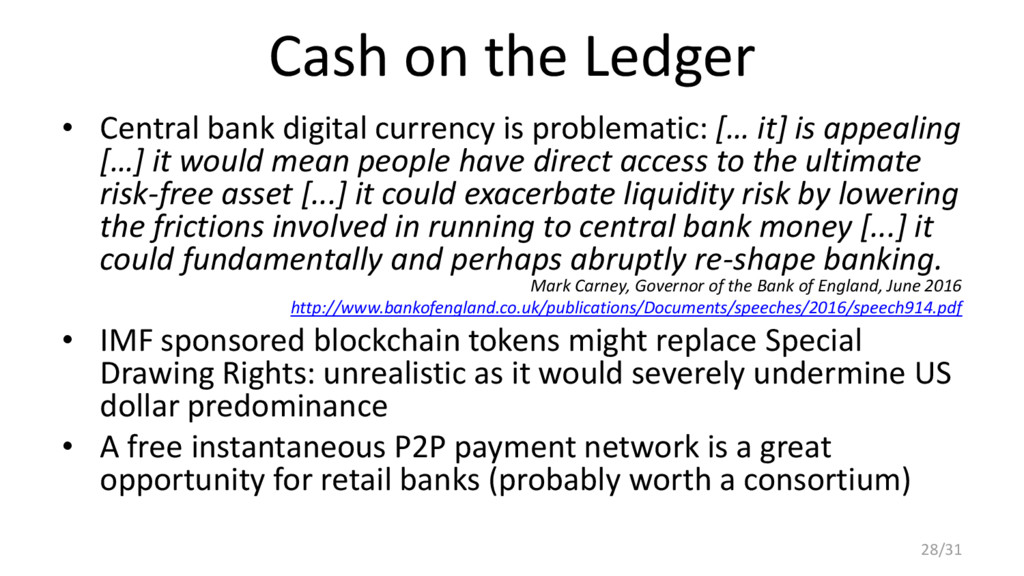

problematic: [… it] is appealing […] it would mean people have direct access to the ultimate risk-free asset [...] it could exacerbate liquidity risk by lowering the frictions involved in running to central bank money [...] it could fundamentally and perhaps abruptly re-shape banking. Mark Carney, Governor of the Bank of England, June 2016 http://www.bankofengland.co.uk/publications/Documents/speeches/2016/speech914.pdf • IMF sponsored blockchain tokens might replace Special Drawing Rights: unrealistic as it would severely undermine US dollar predominance • A free instantaneous P2P payment network is a great opportunity for retail banks (probably worth a consortium) 28/31

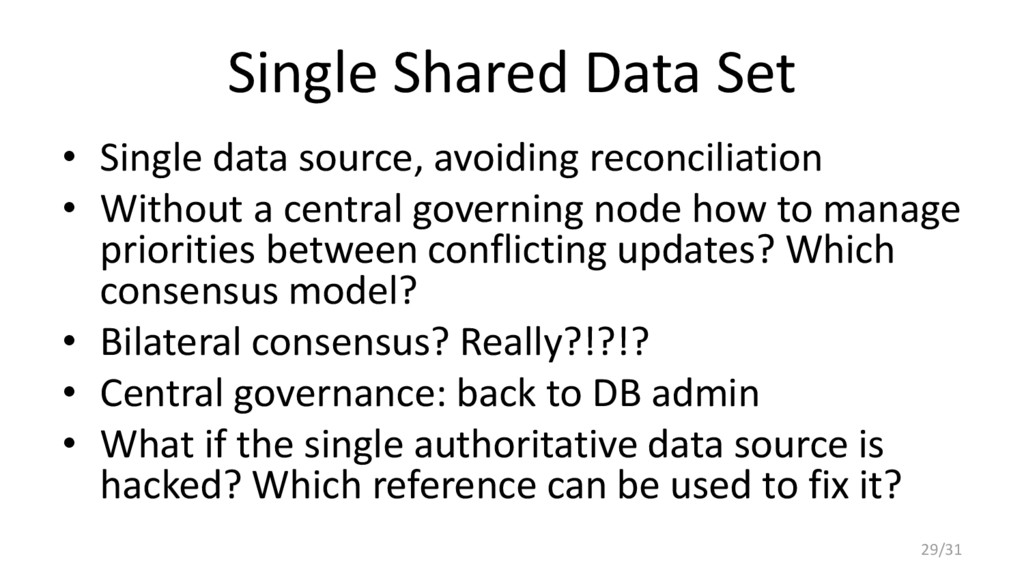

• Without a central governing node how to manage priorities between conflicting updates? Which consensus model? • Bilateral consensus? Really?!?!? • Central governance: back to DB admin • What if the single authoritative data source is hacked? Which reference can be used to fix it? 29/31

the main Ethereum project, it raised >$160m as leaderless Venture Capital • The terms of The DAO are set forth in the smart contract code […] Nothing […] may modify or add any additional obligations or guarantees beyond those set forth in The DAO’s code • Based on its self-executing nature an agent diverted about $50m from The DAO to its own child-DAO start-up • If code is law, then this is not a theft: it is a feature • Beware of extreme automation 30/31

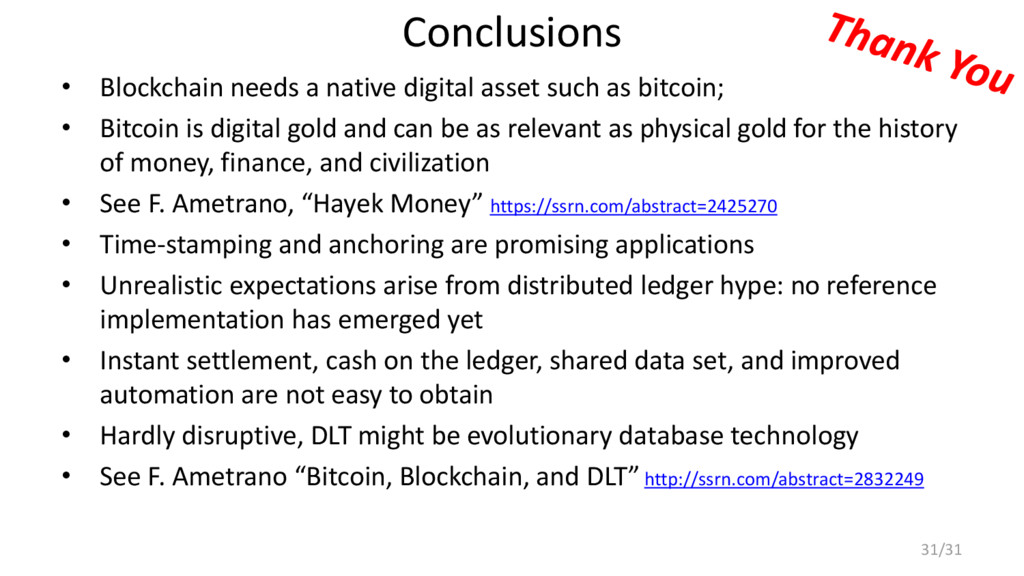

bitcoin; • Bitcoin is digital gold and can be as relevant as physical gold for the history of money, finance, and civilization • See F. Ametrano, “Hayek Money” https://ssrn.com/abstract=2425270 • Time-stamping and anchoring are promising applications • Unrealistic expectations arise from distributed ledger hype: no reference implementation has emerged yet • Instant settlement, cash on the ledger, shared data set, and improved automation are not easy to obtain • Hardly disruptive, DLT might be evolutionary database technology • See F. Ametrano “Bitcoin, Blockchain, and DLT” http://ssrn.com/abstract=2832249 31/31

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}