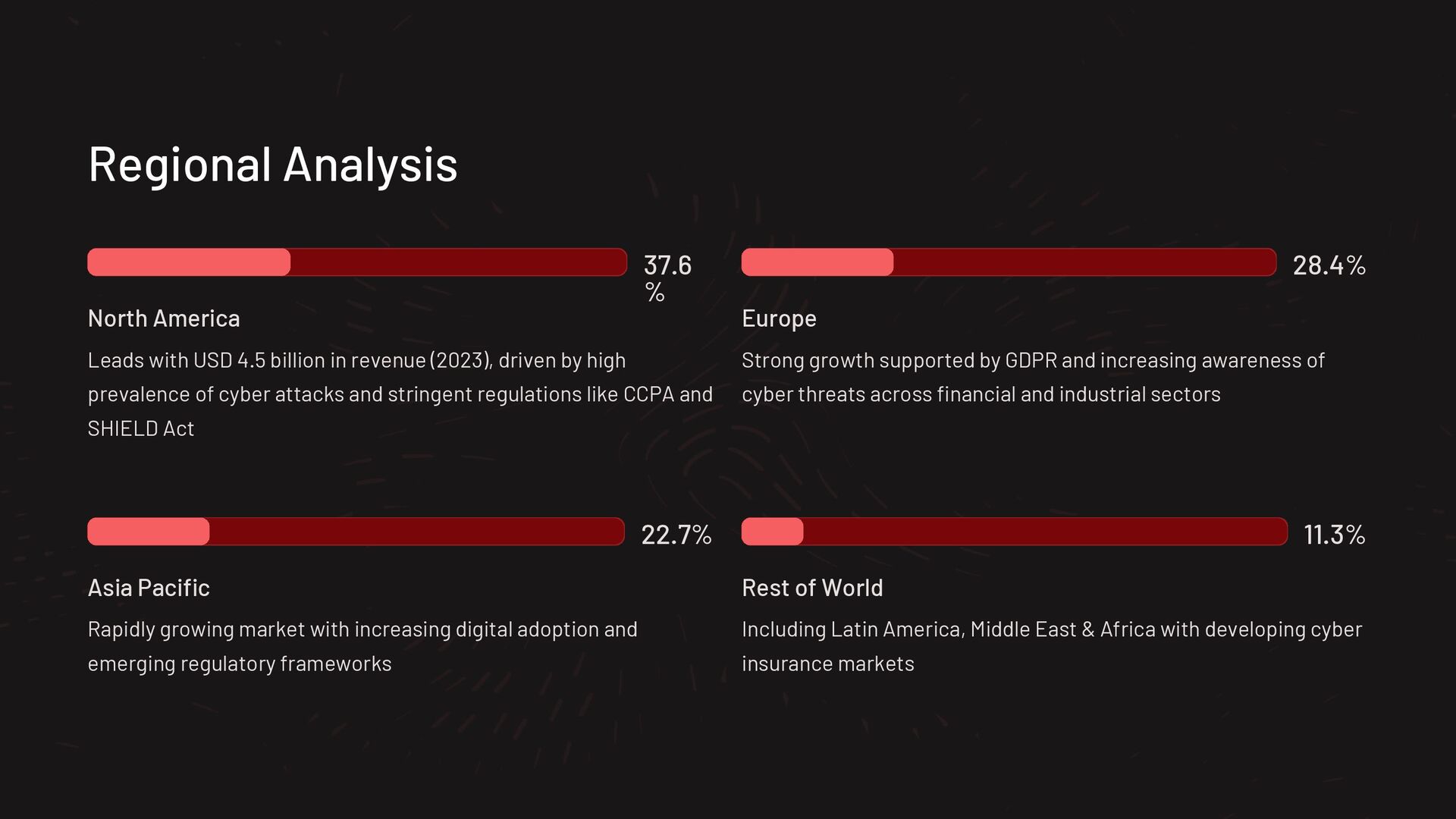

The global cyber insurance market is on a strong growth trajectory, projected to reach USD 90.6 billion by 2033, up from USD 12.1 billion in 2023, expanding at a CAGR of 22.3%. This surge reflects rising digitalization, heightened cyber risk exposure, and growing regulatory pressure across industries. As cyberattacks become more frequent and sophisticated, businesses are increasingly viewing cyber insurance not just as an option but as a core component of their risk management strategy.

In 2023, standalone cyber insurance policies led the market, accounting for over 68.2% share. This dominance underscores the shift in organizational mindset, where tailored, dedicated policies are preferred over bundled coverages. Companies are seeking more precise protection against targeted threats such as ransomware, data exfiltration, and network interruption, all of which demand standalone coverage for clarity and adequacy.

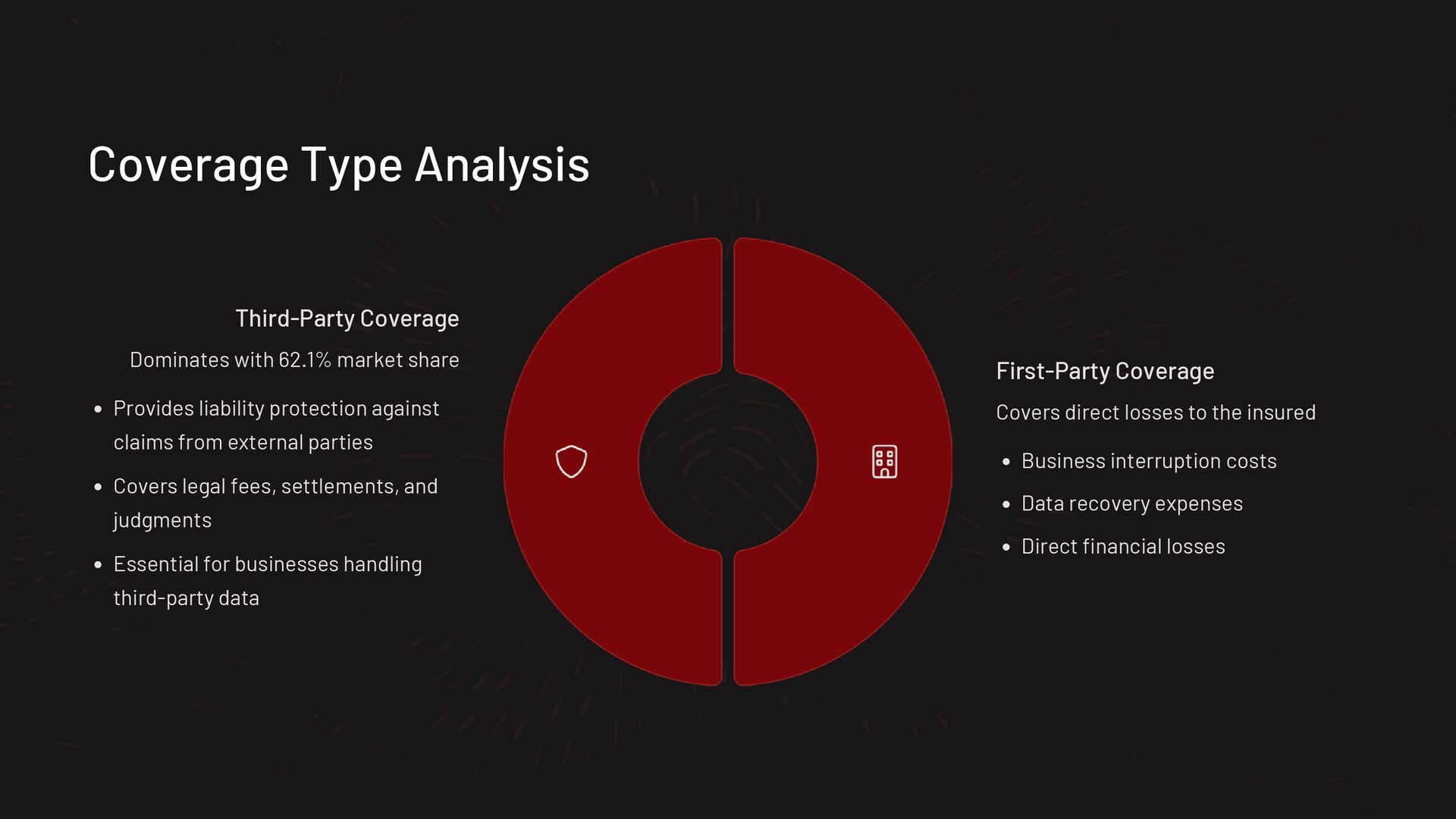

Third-party coverage remains crucial in the cyber insurance landscape, holding a share of over 62.1%. This reflects the growing importance of liability protection against legal and financial claims from clients, partners, or customers affected by a cyber breach. As regulations like GDPR and data privacy acts intensify, demand for third-party risk coverage continues to rise, especially among companies that handle large volumes of consumer data.

Large enterprises dominate the cyber insurance market with more than 72.4% share. Their proactive stance is driven by the need to protect against reputational and financial fallout from cyber events. In contrast, SMEs lag in adoption, largely due to budgetary and awareness challenges, although they remain equally vulnerable to threats. This gap presents a major growth opportunity for insurers offering scalable, affordable solutions to smaller businesses.

The BFSI sector leads all industry verticals, capturing over 28.3% share of the market. With its constant exposure to sensitive financial data and the high cost of data breaches, the sector has become a primary adopter of comprehensive cyber risk policies. Insurers have tailored offerings to meet the sector’s specific compliance and incident response needs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}