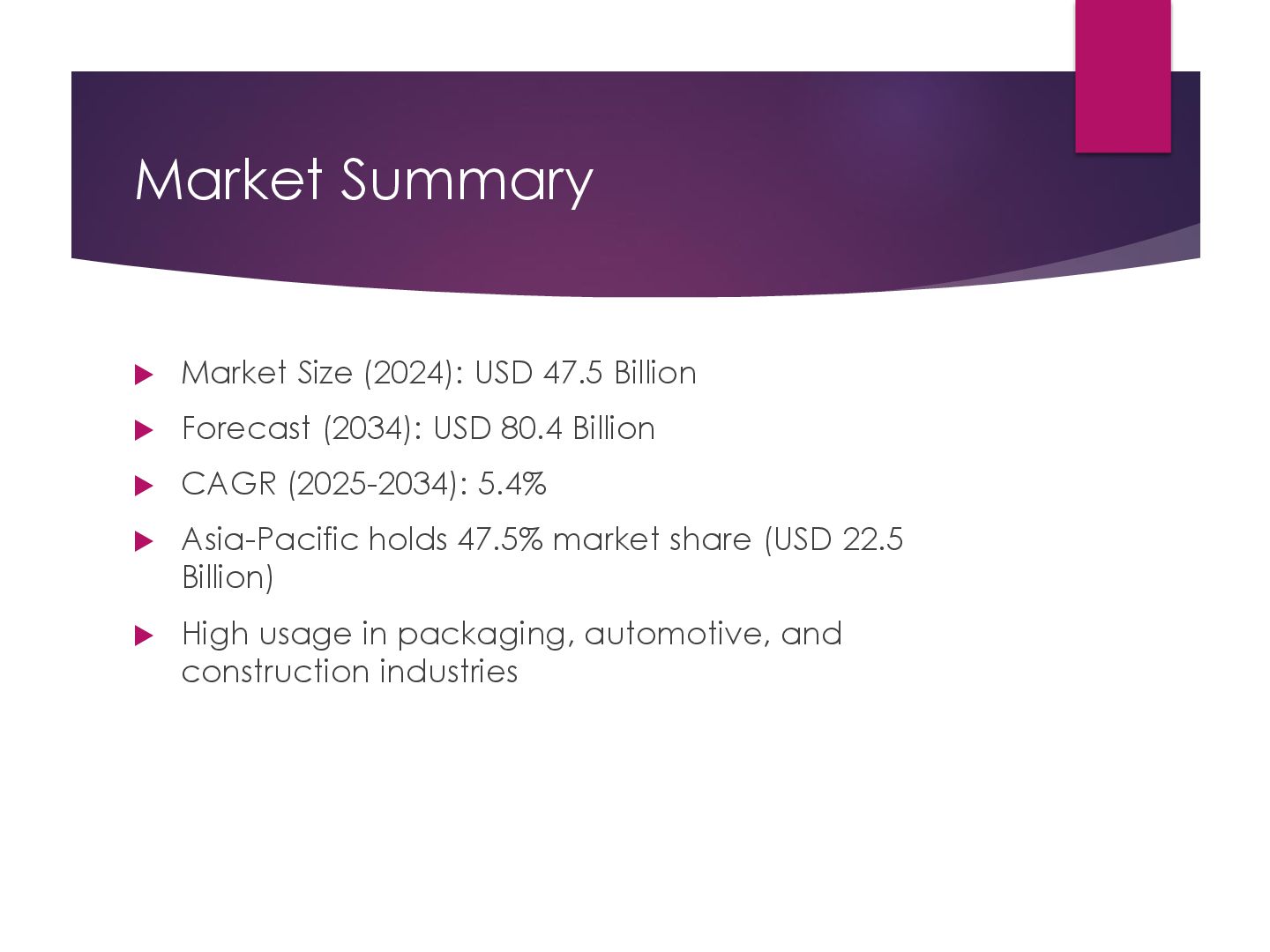

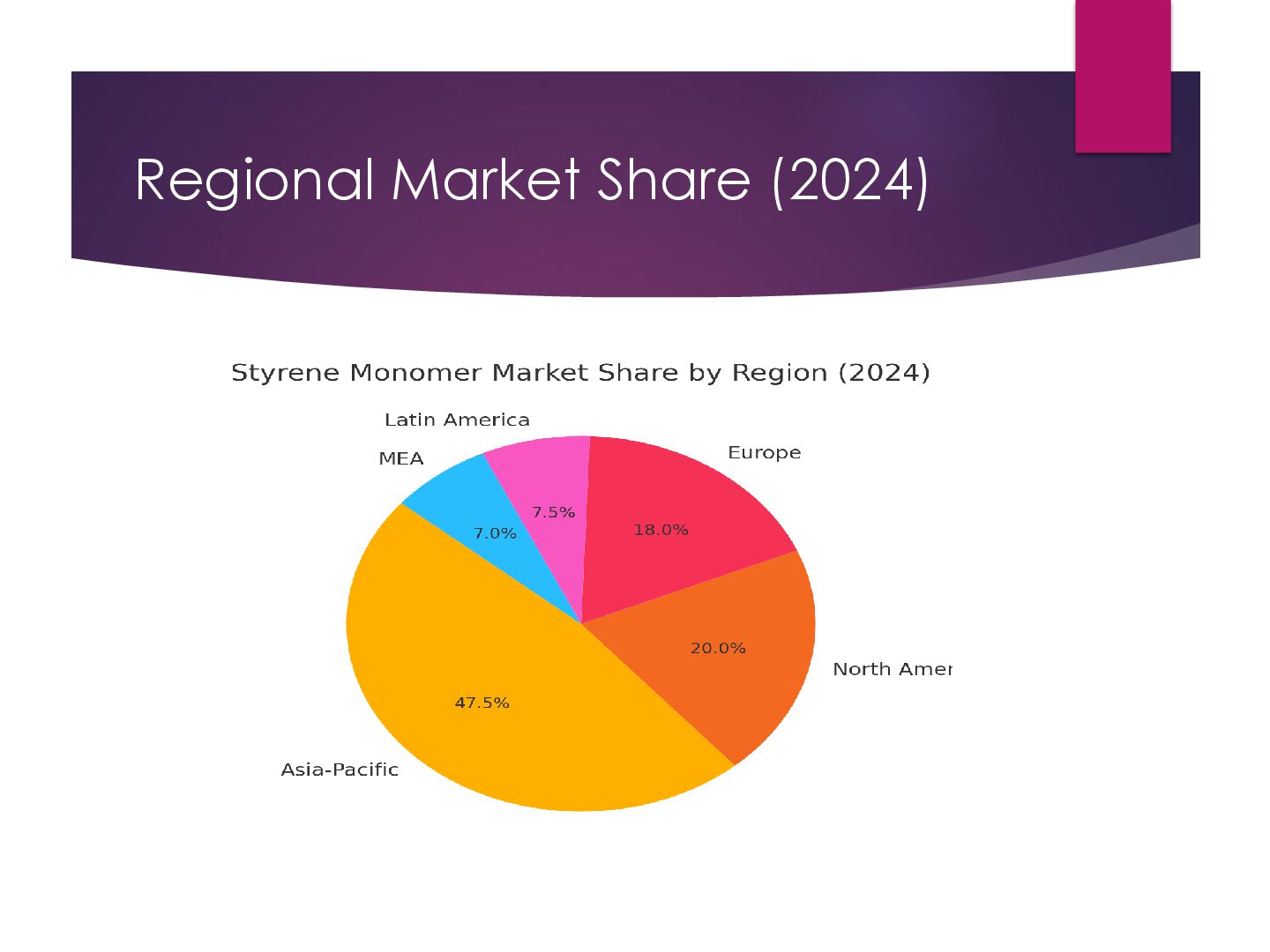

The global Styrene Monomer Market was valued at USD 47.5 billion in 2024 and is projected to reach approximately USD 80.4 billion by 2034, growing at a compound annual growth rate (CAGR) of 5.4% from 2025 to 2034. In 2024, the Asia-Pacific region held a leading market share of 47.5%, which translated to a market valuation of around USD 22.5 billion. This dominance is mainly driven by demand in packaging, automotive, and construction industries in countries such as China and India.

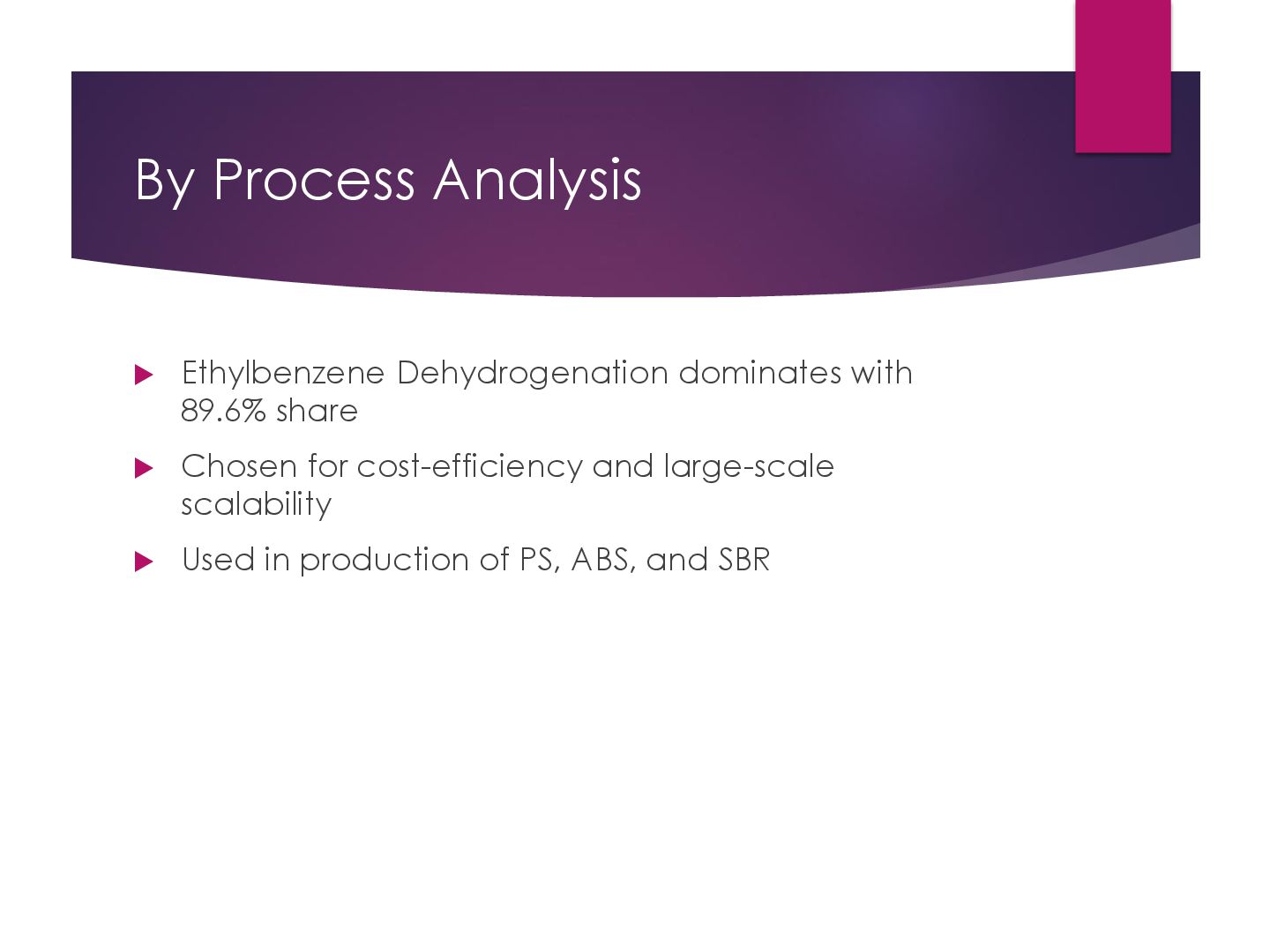

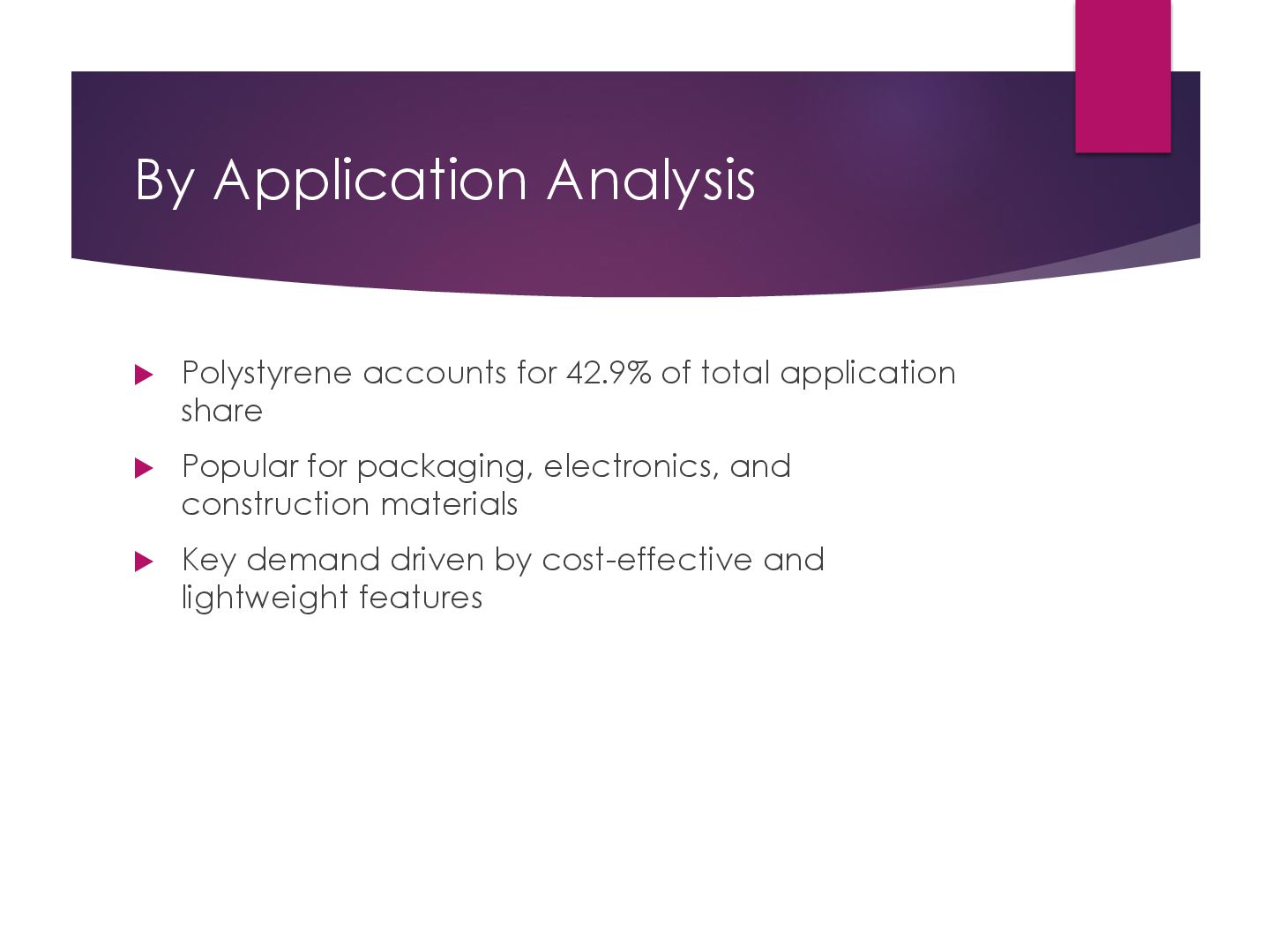

From a production perspective, Ethylbenzene Dehydrogenation is the dominant process, accounting for 89.6% of global styrene production in 2024, owing to its cost-efficiency and scalability. In terms of applications, Polystyrene (PS) leads with a 42.9% share, making it the most common use of styrene monomer globally due to its utility in packaging, electronics, and insulation.

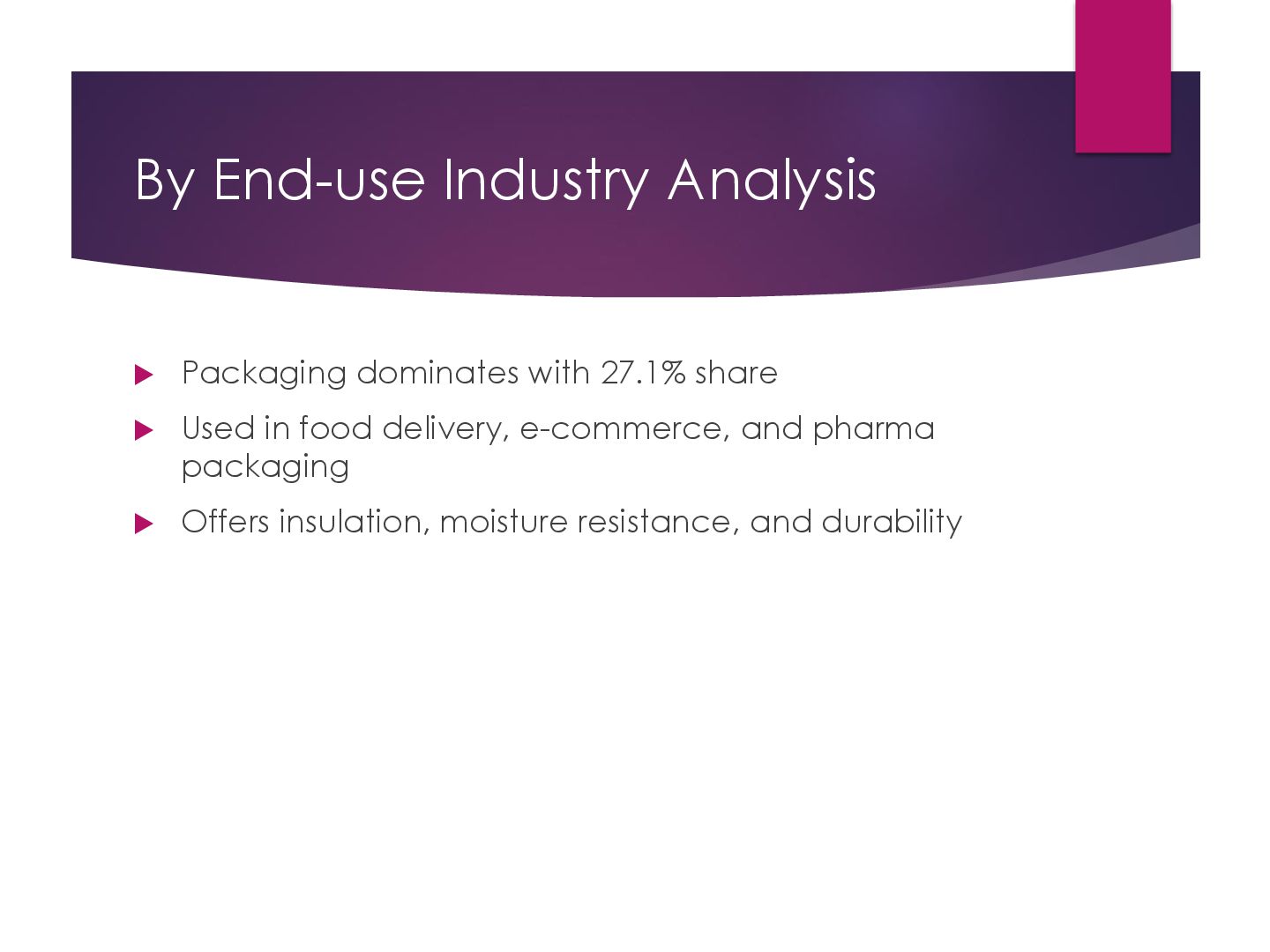

Among end-use industries, packaging holds the highest share at 27.1%, with extensive use in foam trays, containers, and other protective materials.India is investing significantly in domestic styrene production through a major project by Indian Oil Corporation Limited (IOCL), with a planned capacity of 387,000 tonnes annually, expected to be operational by 2026-27, and an investment of approximately INR 4,495 crore.

Meanwhile, the Chemicals and Petrochemicals Association of India (CPAI) projects a 15% increase in national styrene demand between FY2024-25 and FY2025-26, from 1.22 million tonnes to 1.40 million tonnes. These developments highlight strong regional growth and the emphasis on self-reliance and infrastructure expansion.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}