an upward trajectory since the last trading update (+10% as at 25 Feb).” “Overall market seat supply remains strong heading into the summer, with over 70m seats from UK departure points to European destinations.” swipe >> On the Beach interim results – May 25

was +0% Year on year, and 64% sold (in line with last year). Average Price is 4% up on prior year. Booking pattern is later.” “TUI has held flat on risk capacity. Any growth will come from lower-risk dynamic packaging.” TUI Q2 trading update – May 25

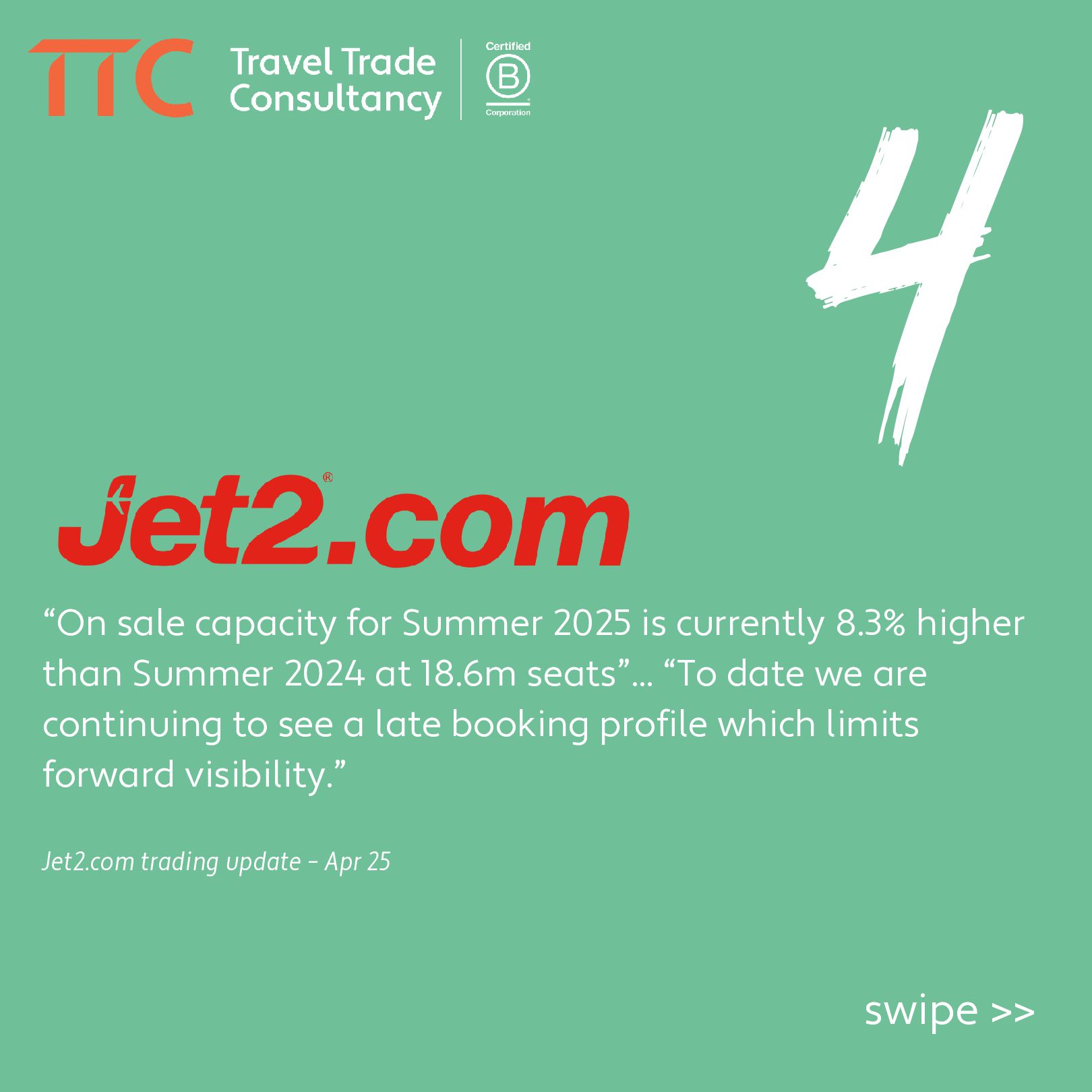

capacity for Summer 2025 is currently 8.3% higher than Summer 2024 at 18.6m seats”... “To date we are continuing to see a late booking profile which limits forward visibility.”

rebounded and recovered in March, such that the full quarter was generally in line with our expectations… I wouldn’t say that April is necessarily below. There has been some week-to-week and month-to-month volatility since the beginning of the year.” Airbnb Q1 earnings webcast – May 25

Additionally, during April, the company's bookings were greater than the same period last year, including continued strength in close-in bookings. Booked load factors remain in line with prior years and at higher rates.” Royal Caribbean Q1 update – Apr 25

the second quarter, with revenue ahead of last year, and 29% booked for the second half, broadly in line with last year... Capacity increase of c.3% is unchanged.” swipe >> IAG results update – May 25

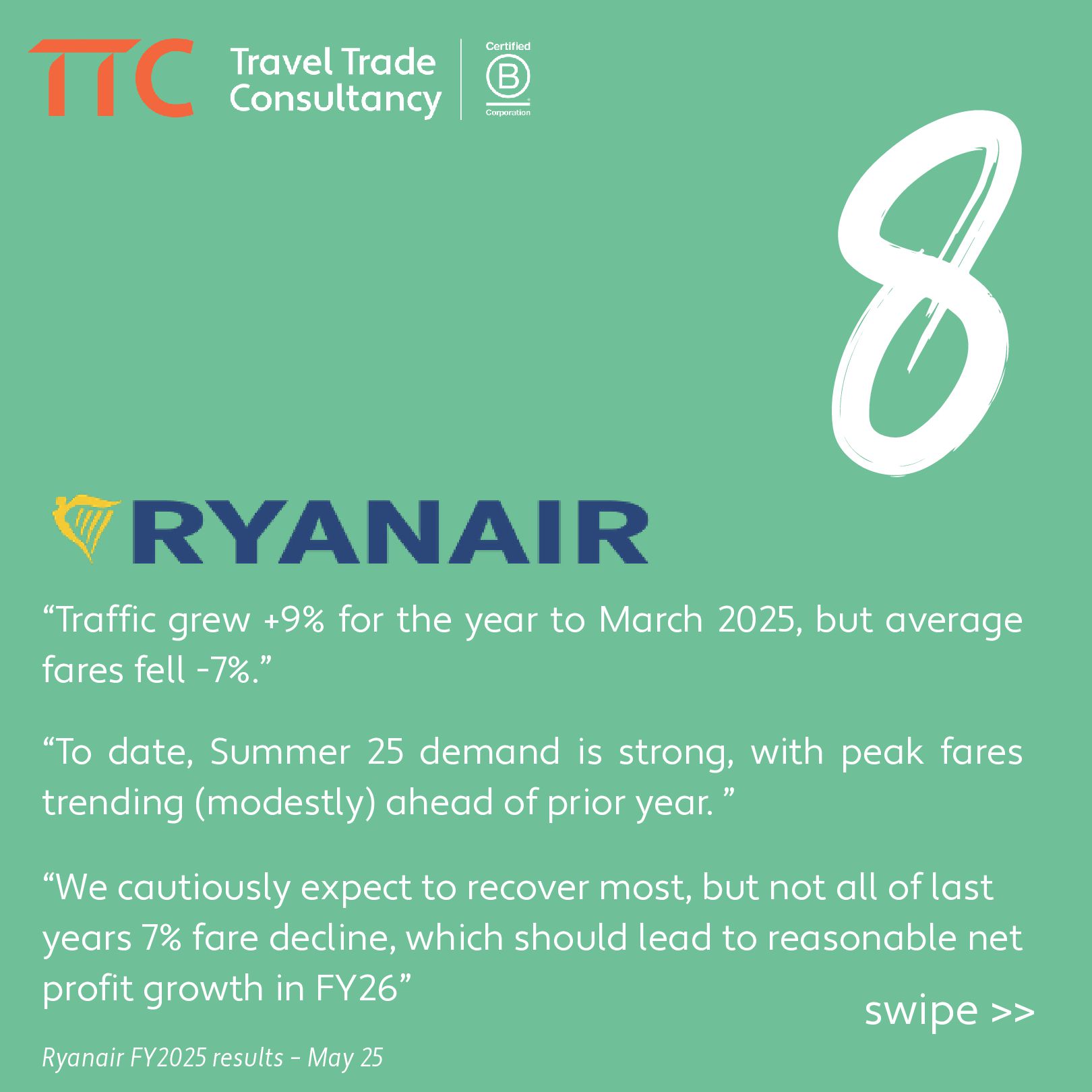

all of last years 7% fare decline, which should lead to reasonable net profit growth in FY26” Ryanair FY2025 results – May 25 “Traffic grew +9% for the year to March 2025, but average fares fell -7%.” “To date, Summer 25 demand is strong, with peak fares trending (modestly) ahead of prior year. ”

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}