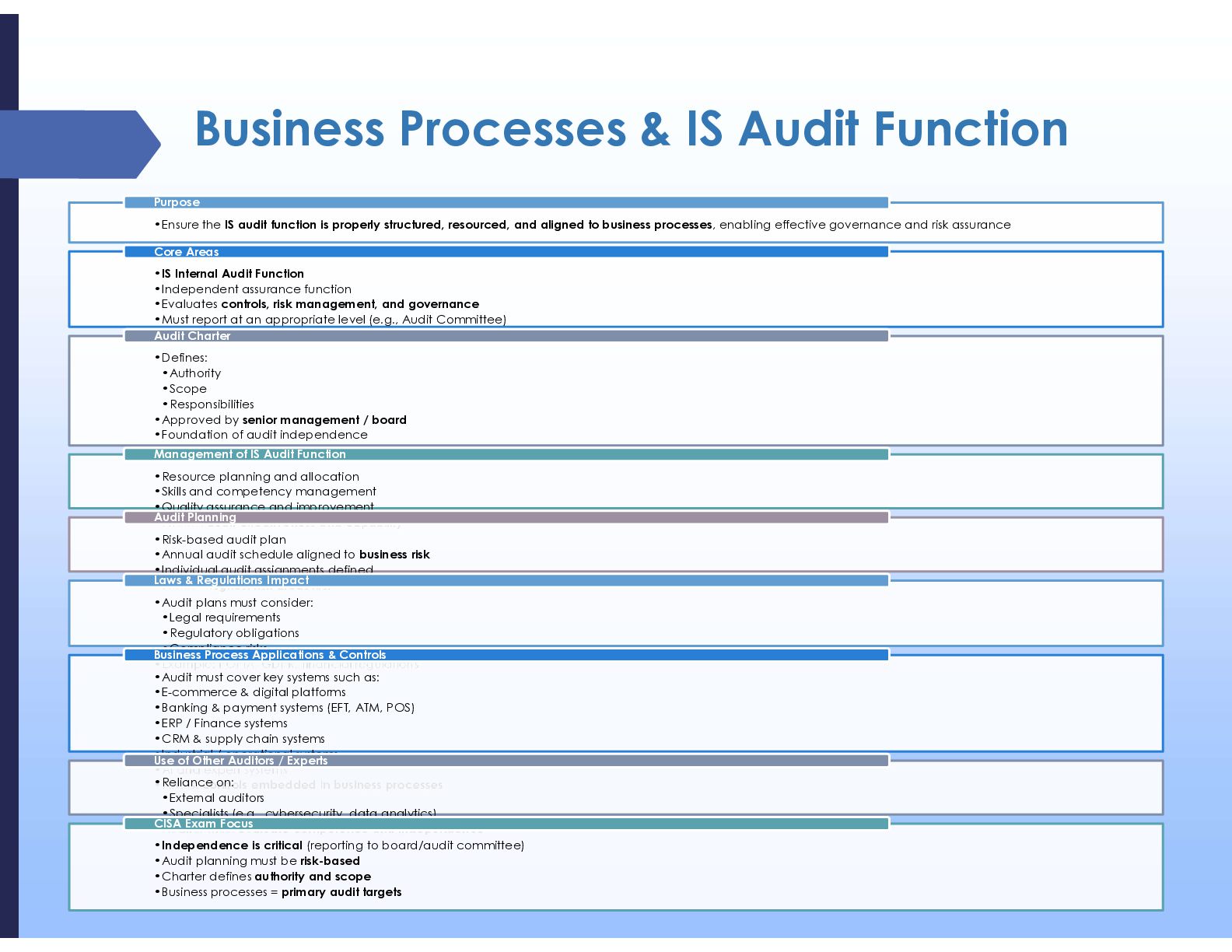

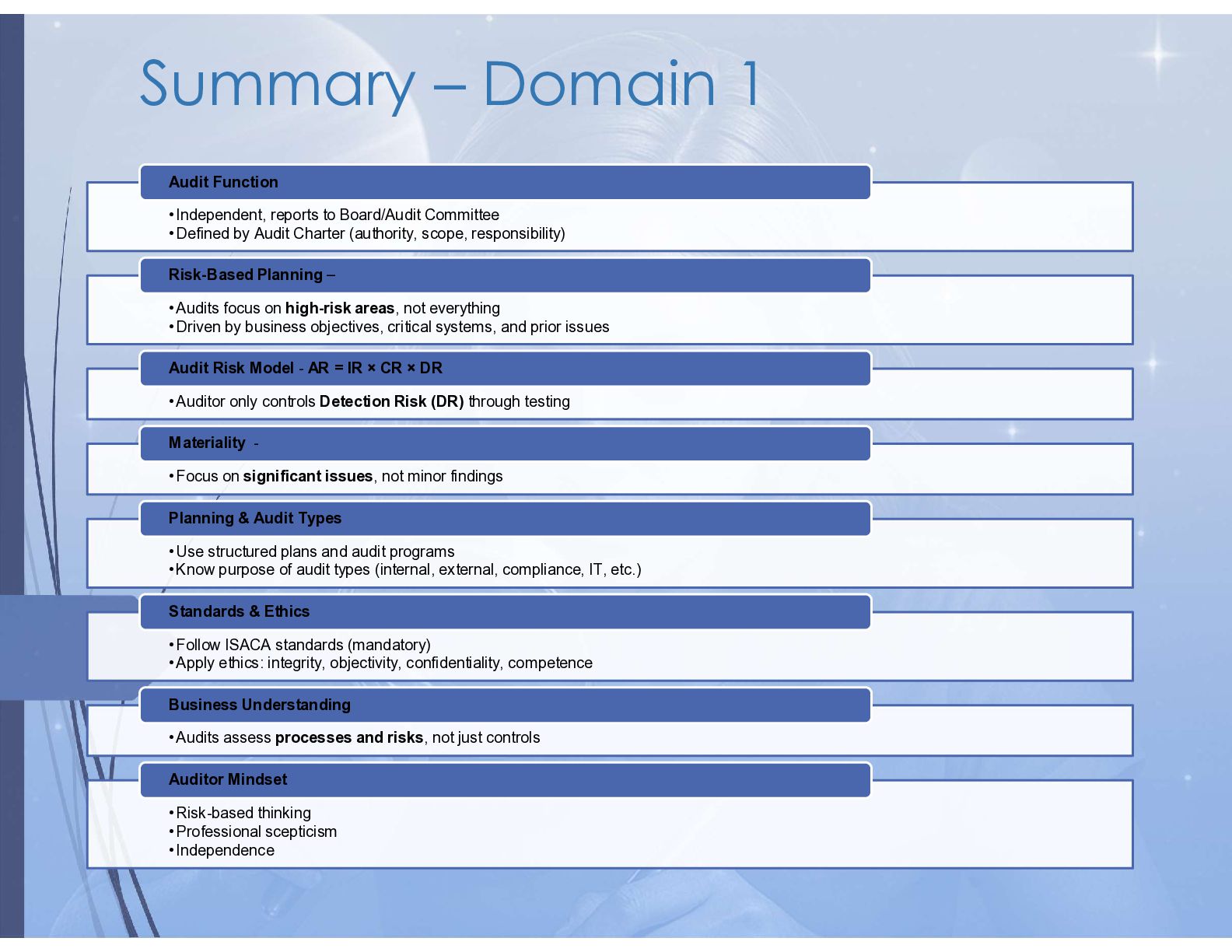

This This presentation is part of my CISA Exam Preparation Series, and in this section we take a deeper dive into Domain 1: Information System Auditing Process — focusing on how audits are actually planned, executed, and evaluated in practice.

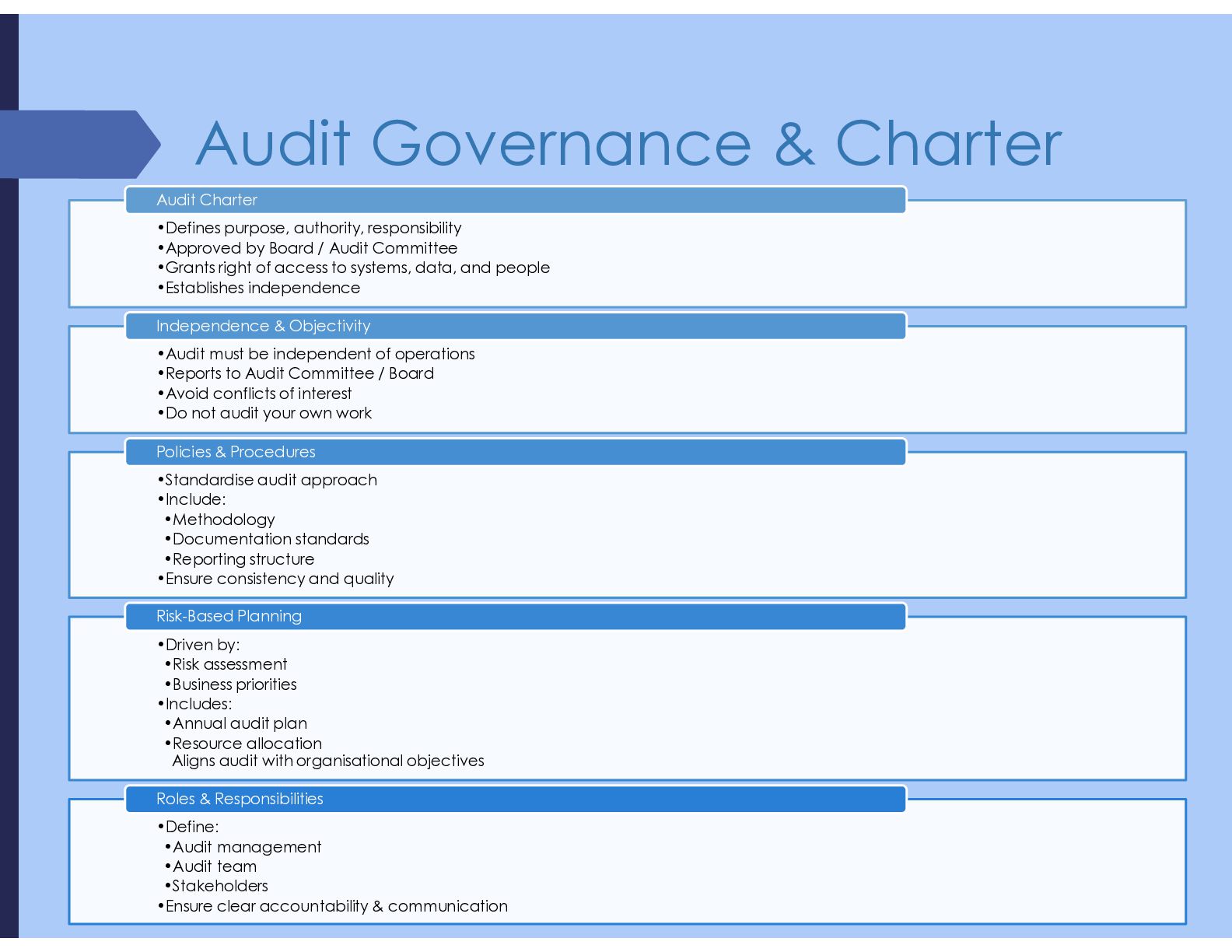

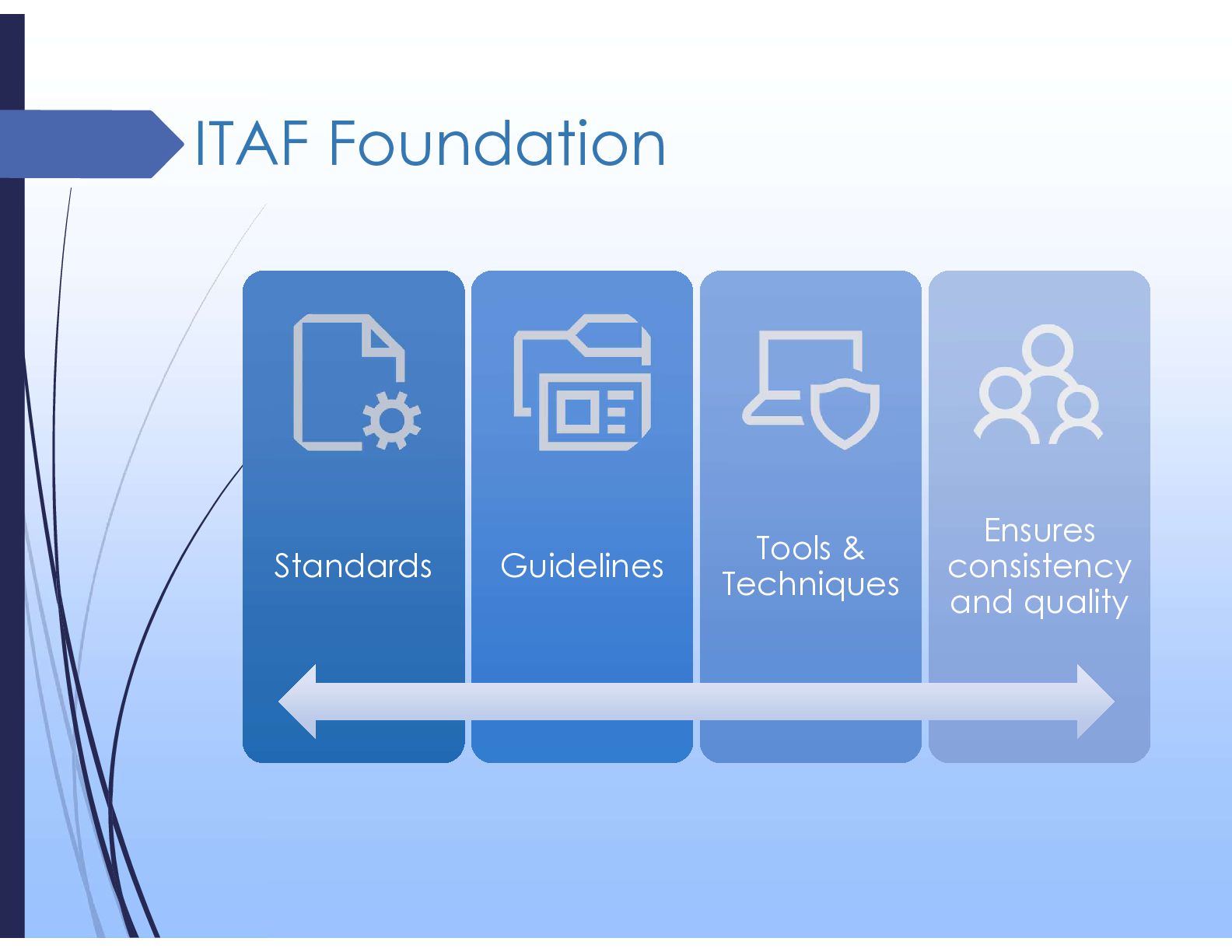

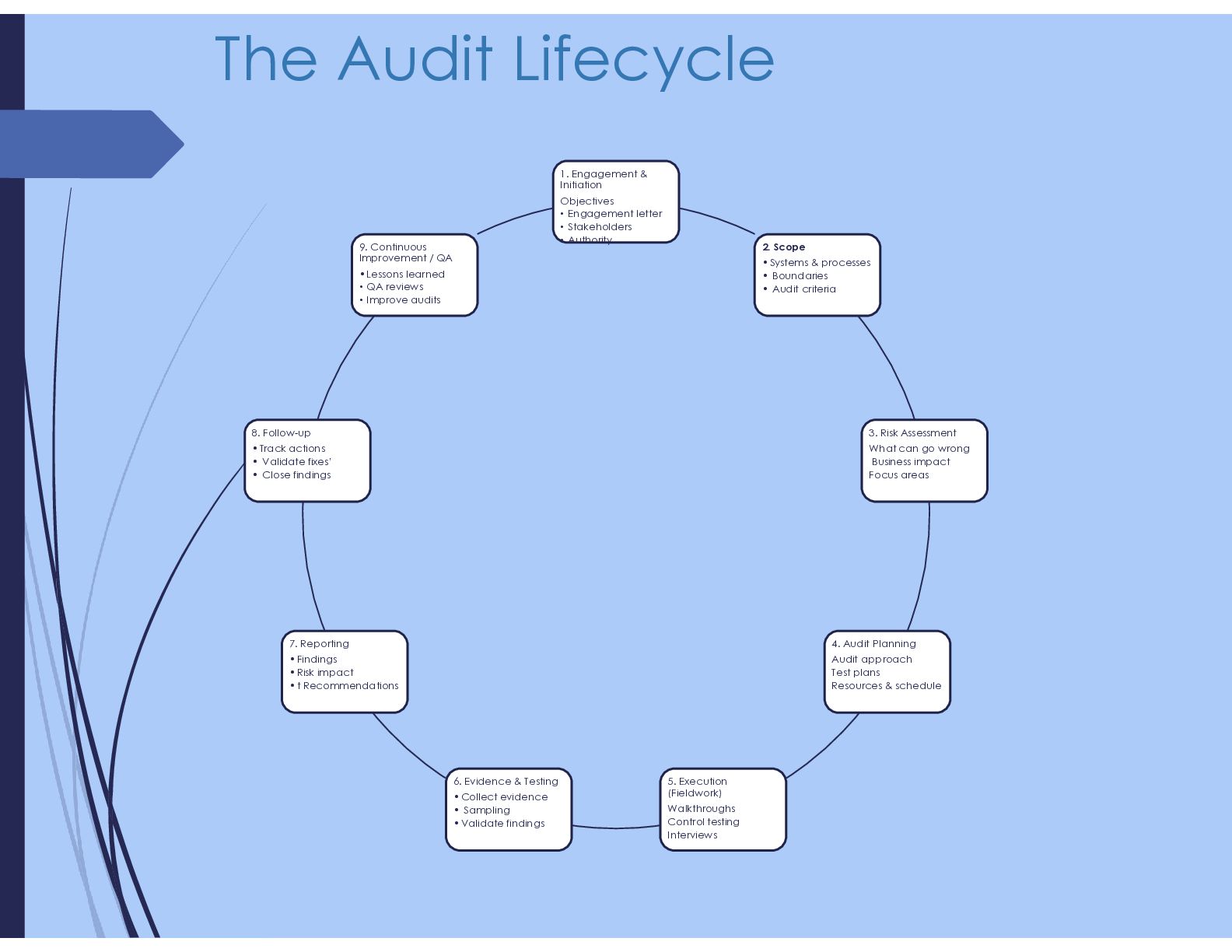

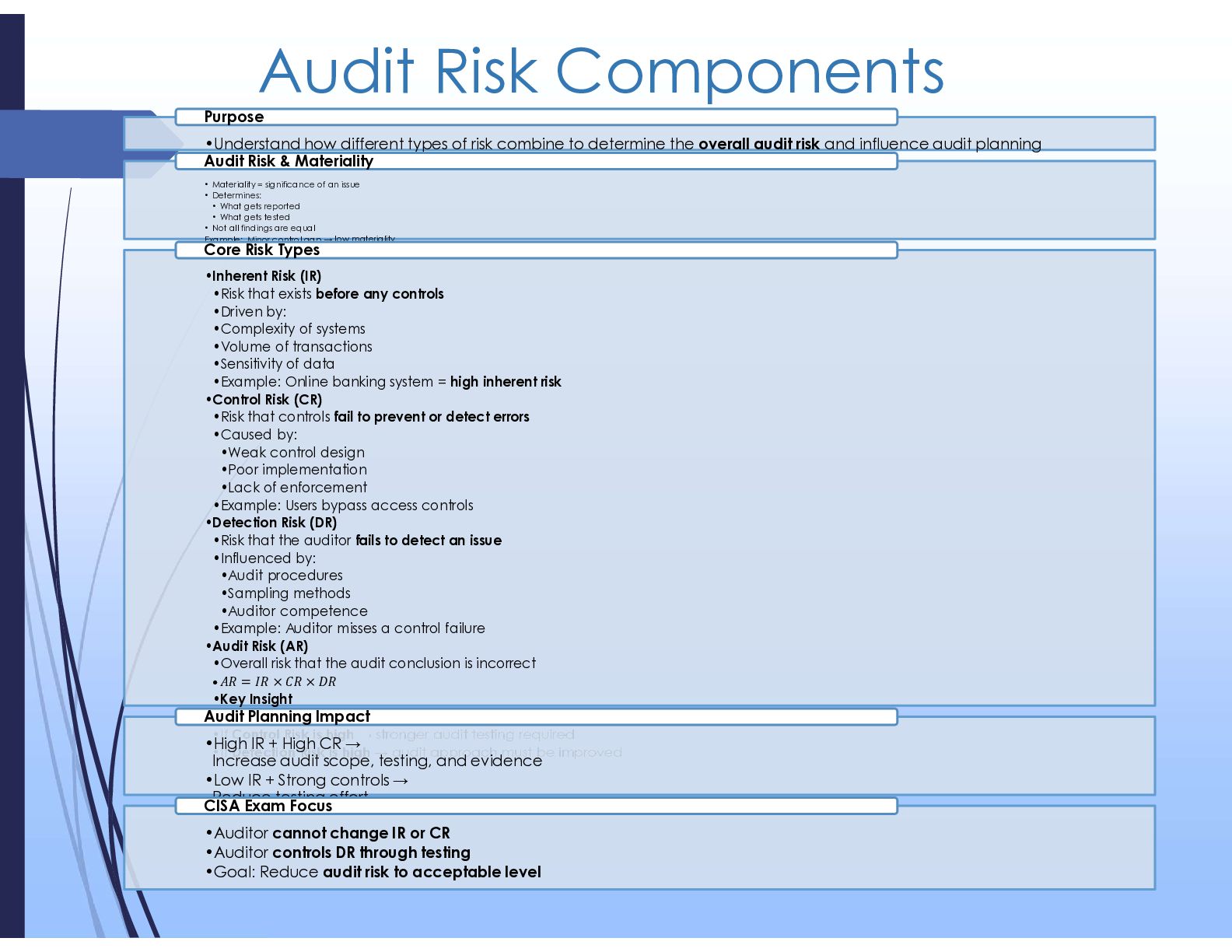

We move beyond theory and break down key areas such as the audit lifecycle, risk-based planning, audit risk components, evidence collection, sampling techniques, and reporting. The aim is to build a clear understanding of how an auditor thinks — from identifying risk, to testing controls, to forming defensible conclusions.

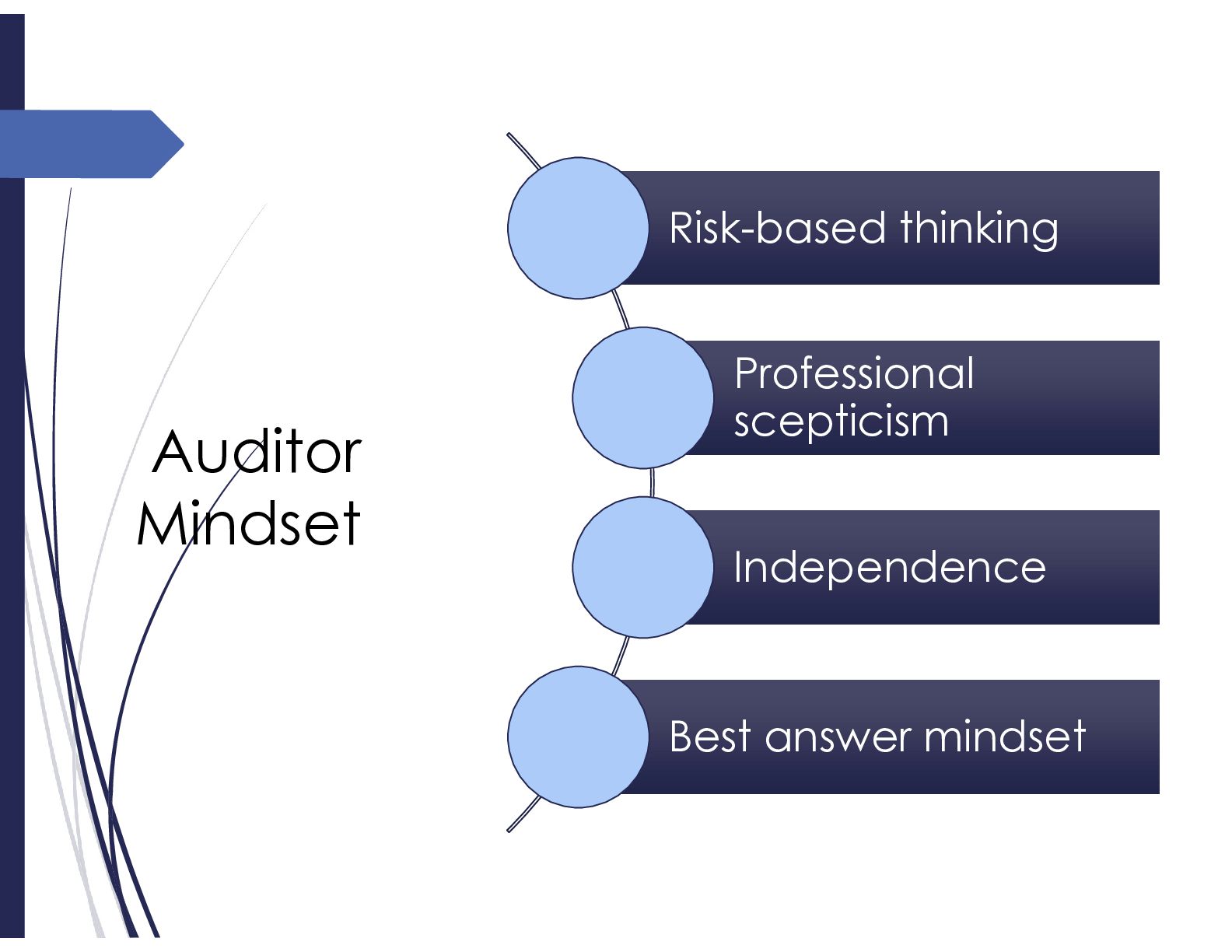

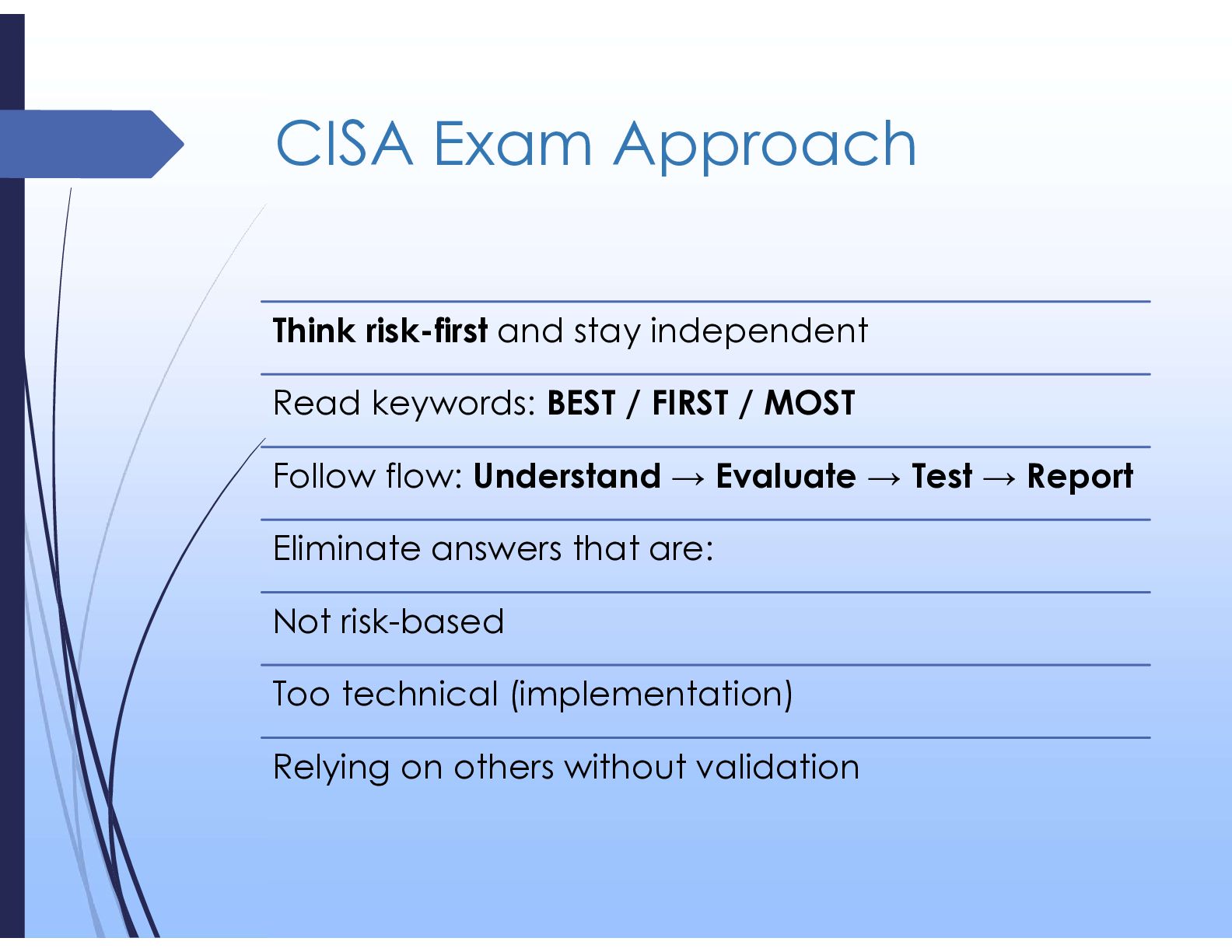

This part also emphasises the auditor mindset, including independence, professional scepticism, and the importance of selecting the best answer in exam scenarios — not just a technically correct one.

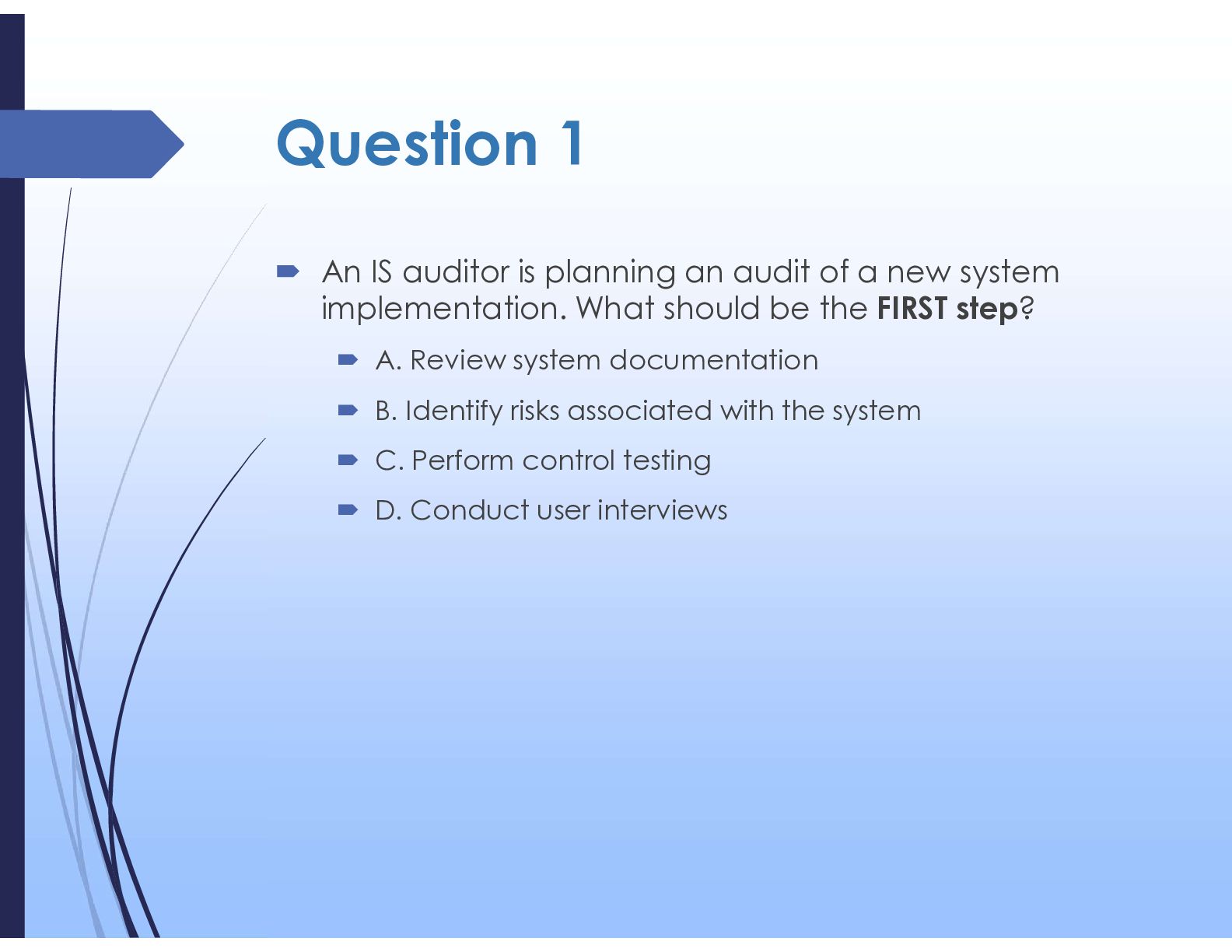

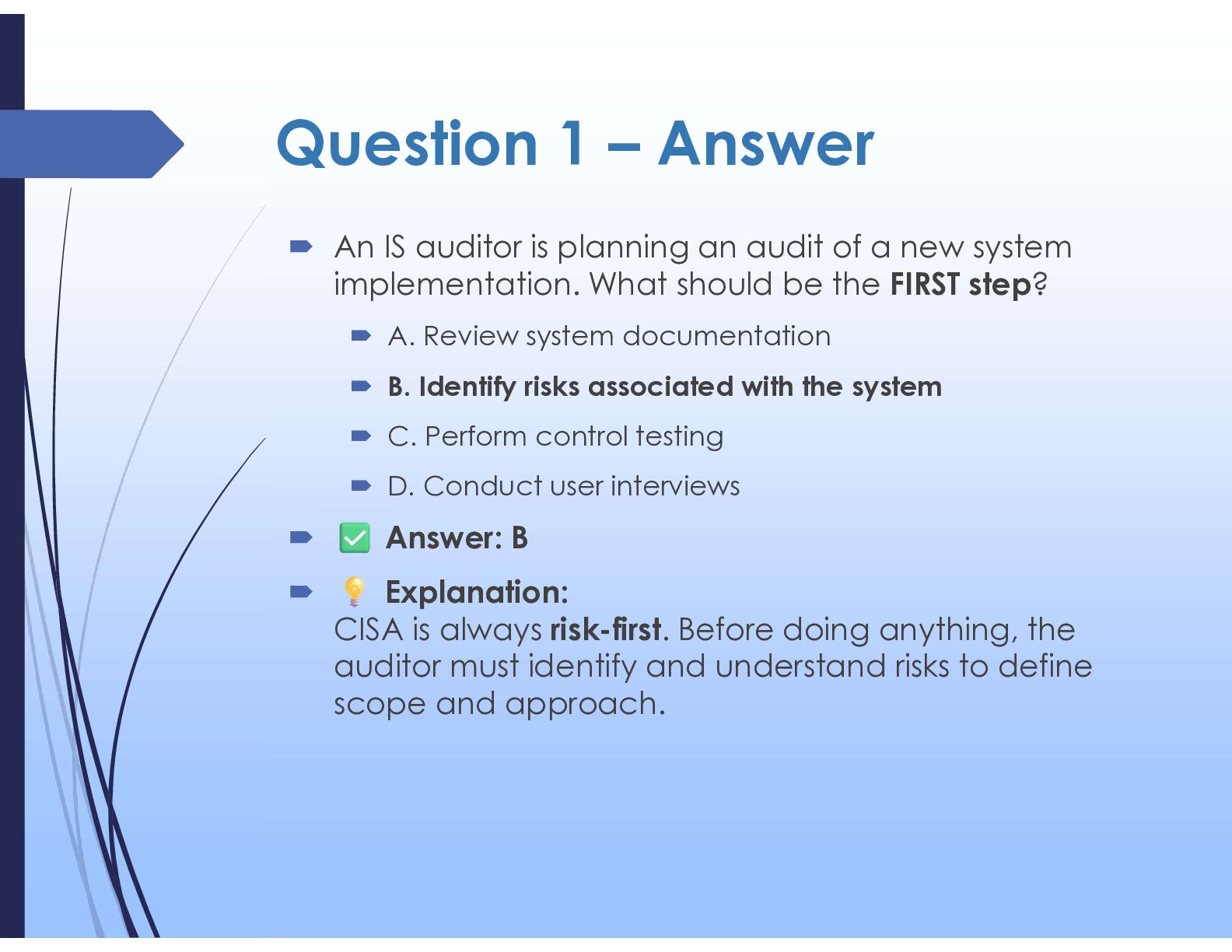

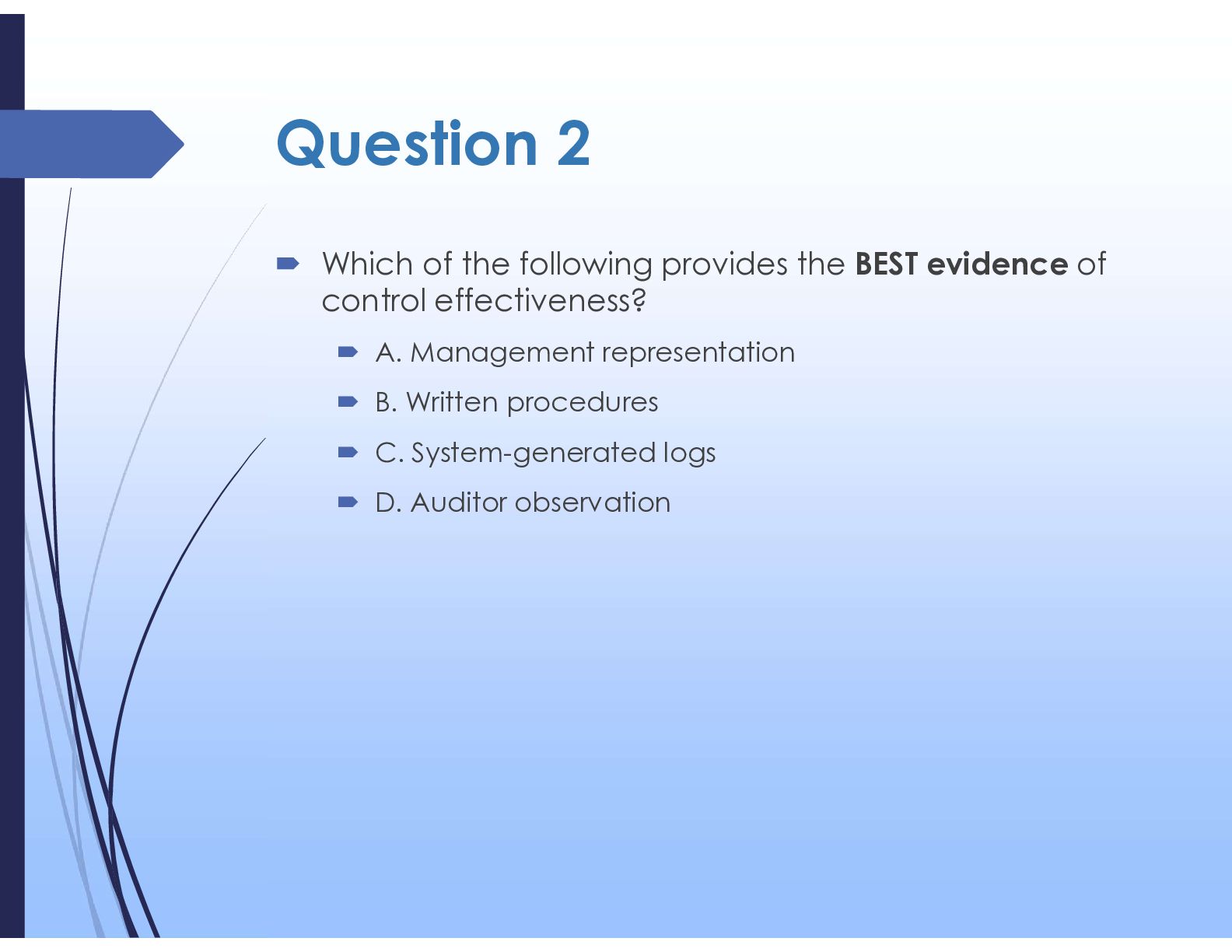

Throughout the video, I link concepts to practical examples and include CISA-style questions to reinforce how these topics are tested in the exam.

This is part of my personal learning journey, and I’m sharing it in case it helps others preparing for the CISA exam.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}