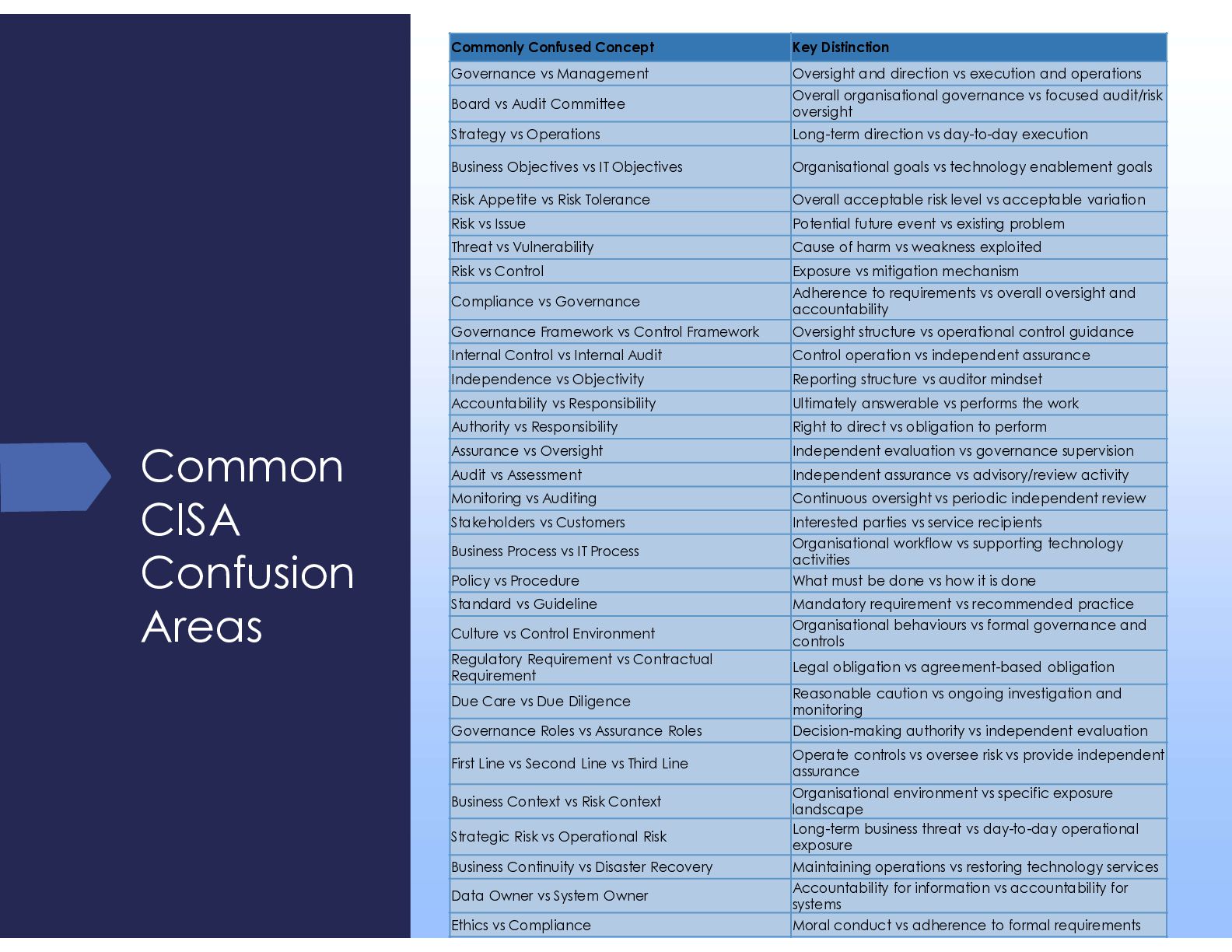

Part 2B of the CISA Audit Process series explores the governance and foundational concepts that support effective information systems auditing and risk-based assurance activities.

This presentation covers:

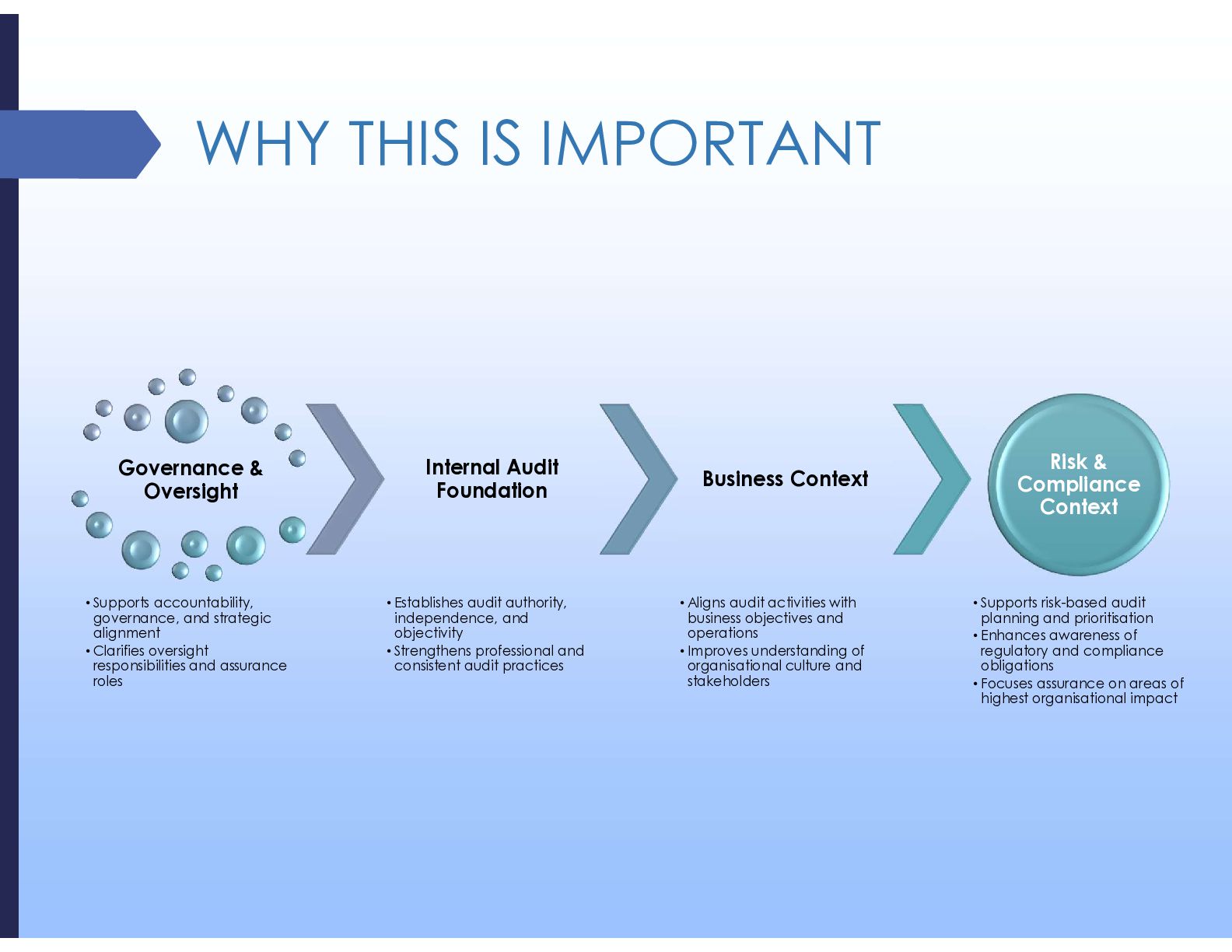

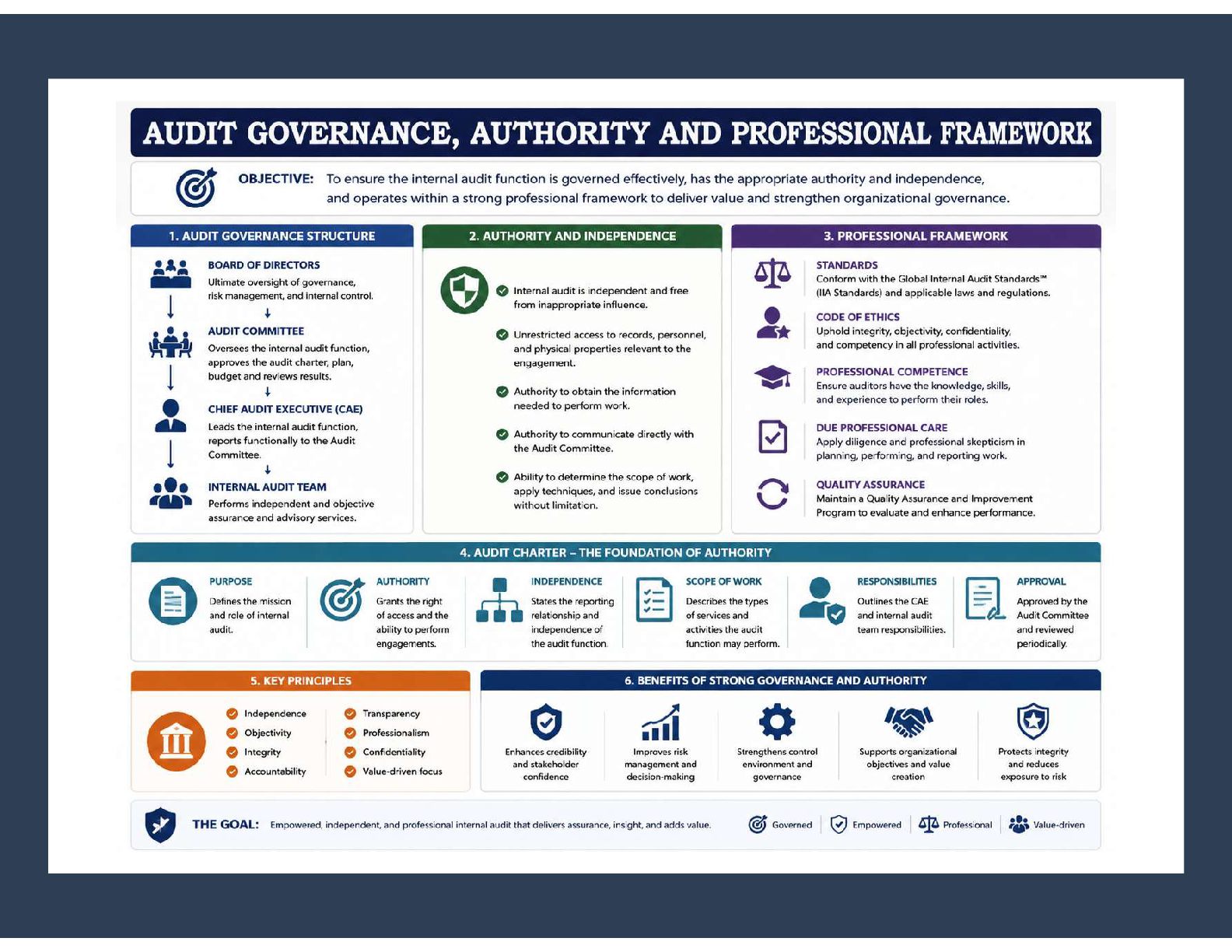

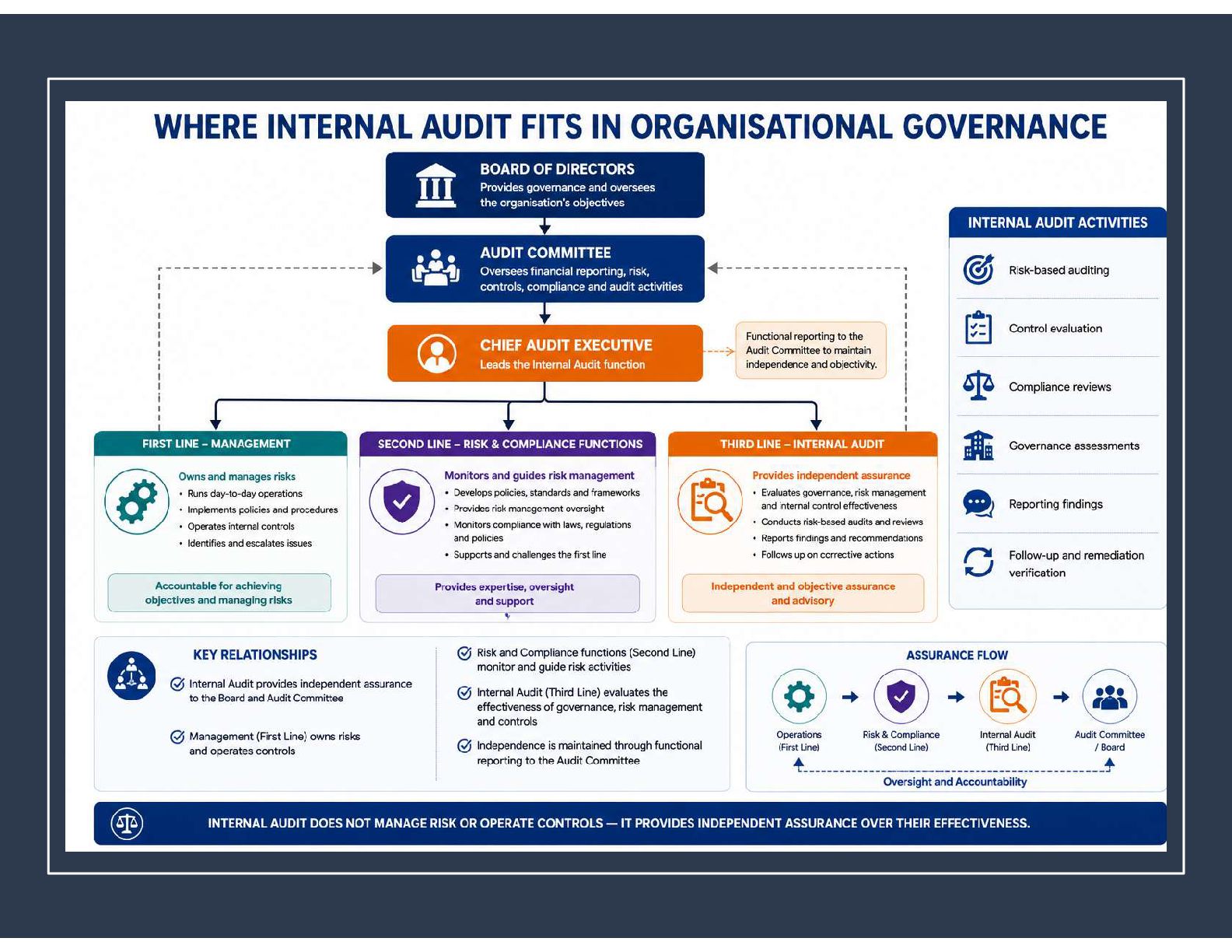

• Governance structures and oversight responsibilities

• The role of the Board, Audit Committee, and Chief Audit Executive

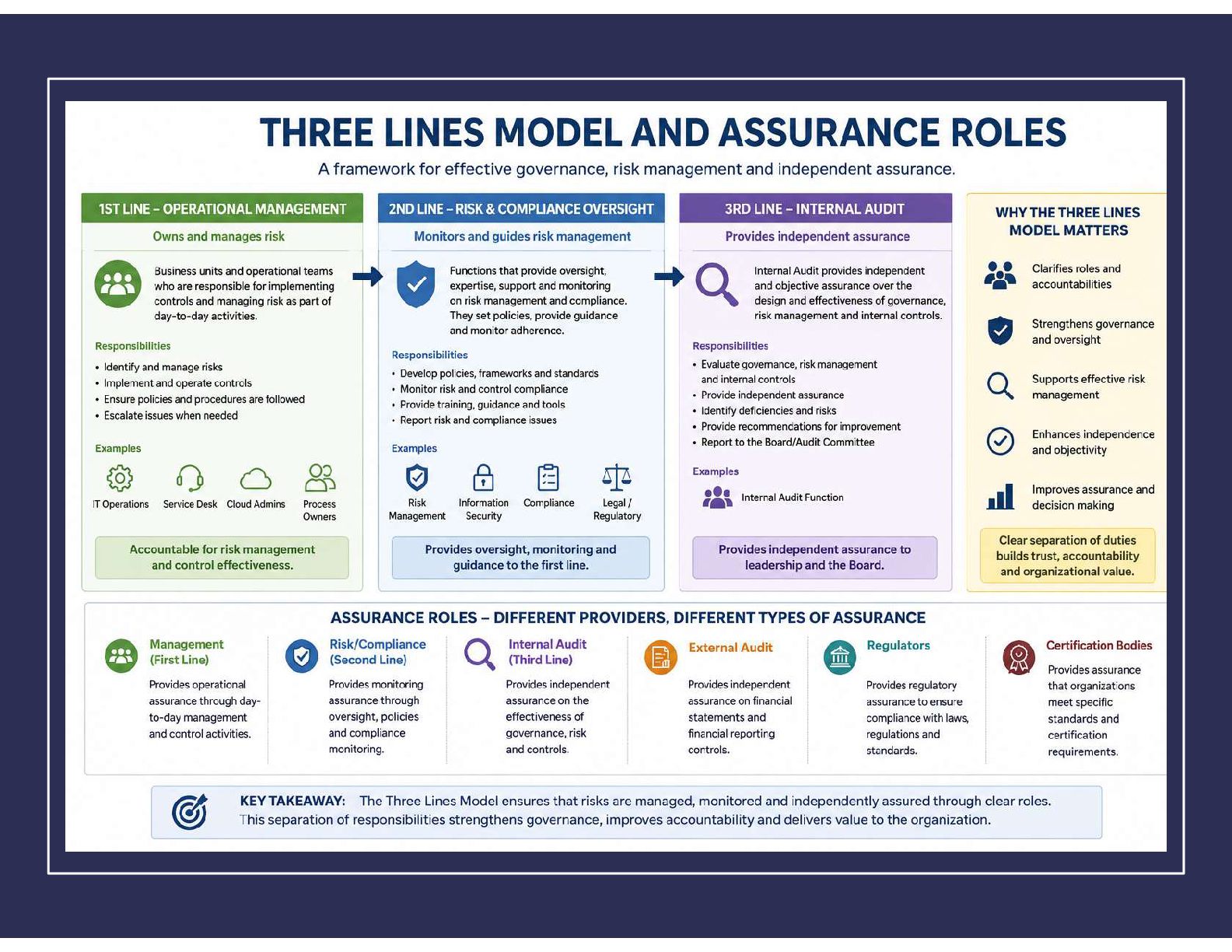

• The Three Lines Model and assurance responsibilities

• Audit authority, independence, and objectivity

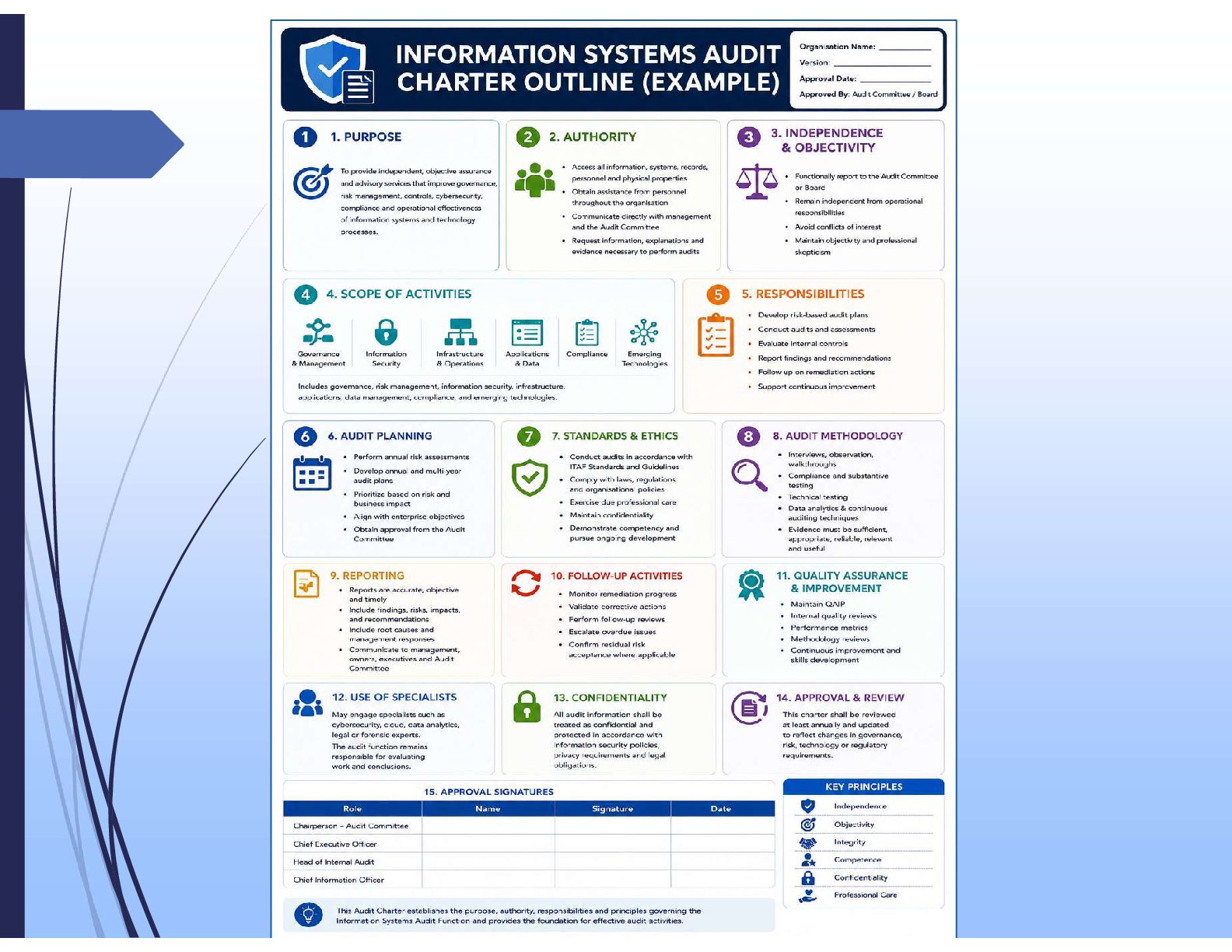

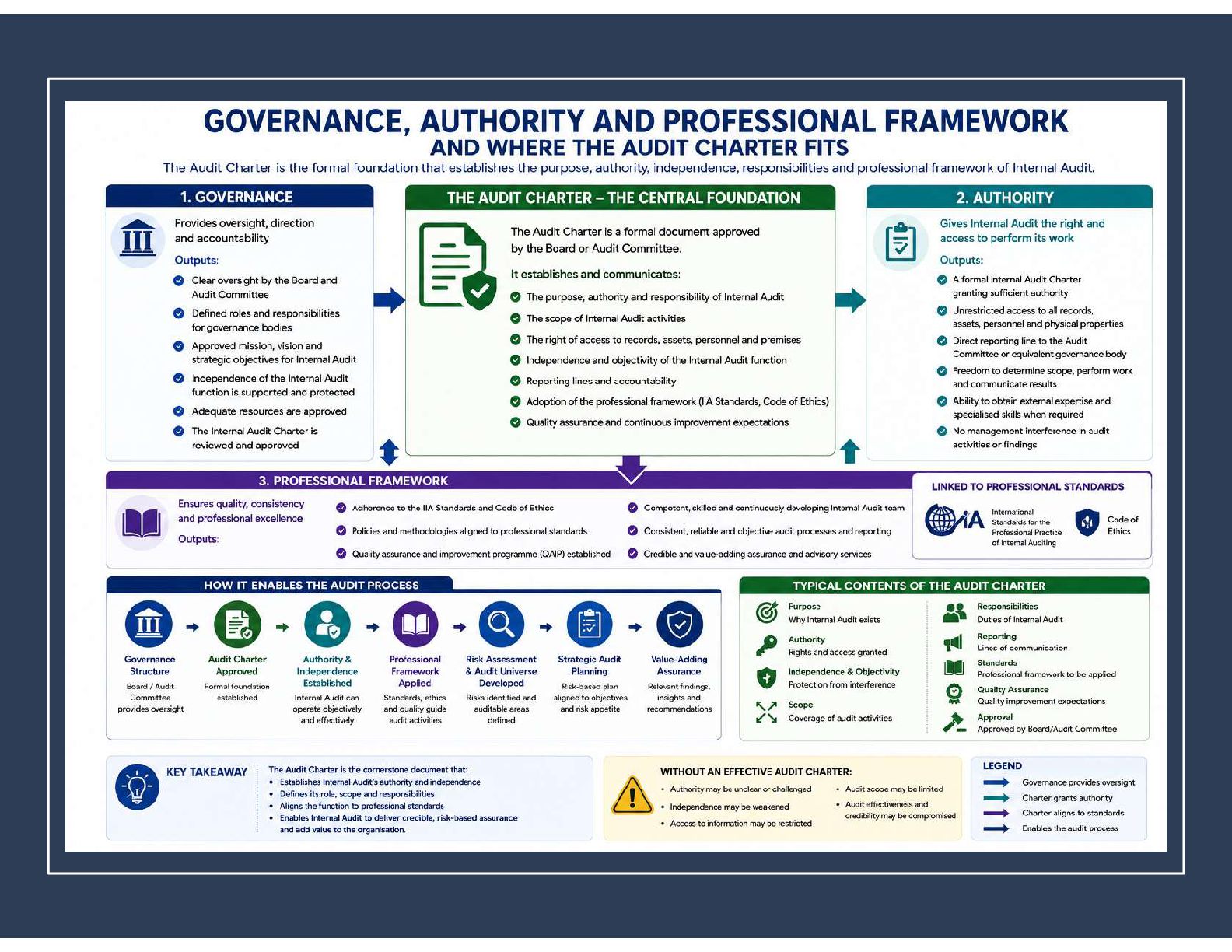

• The purpose and importance of the Audit Charter

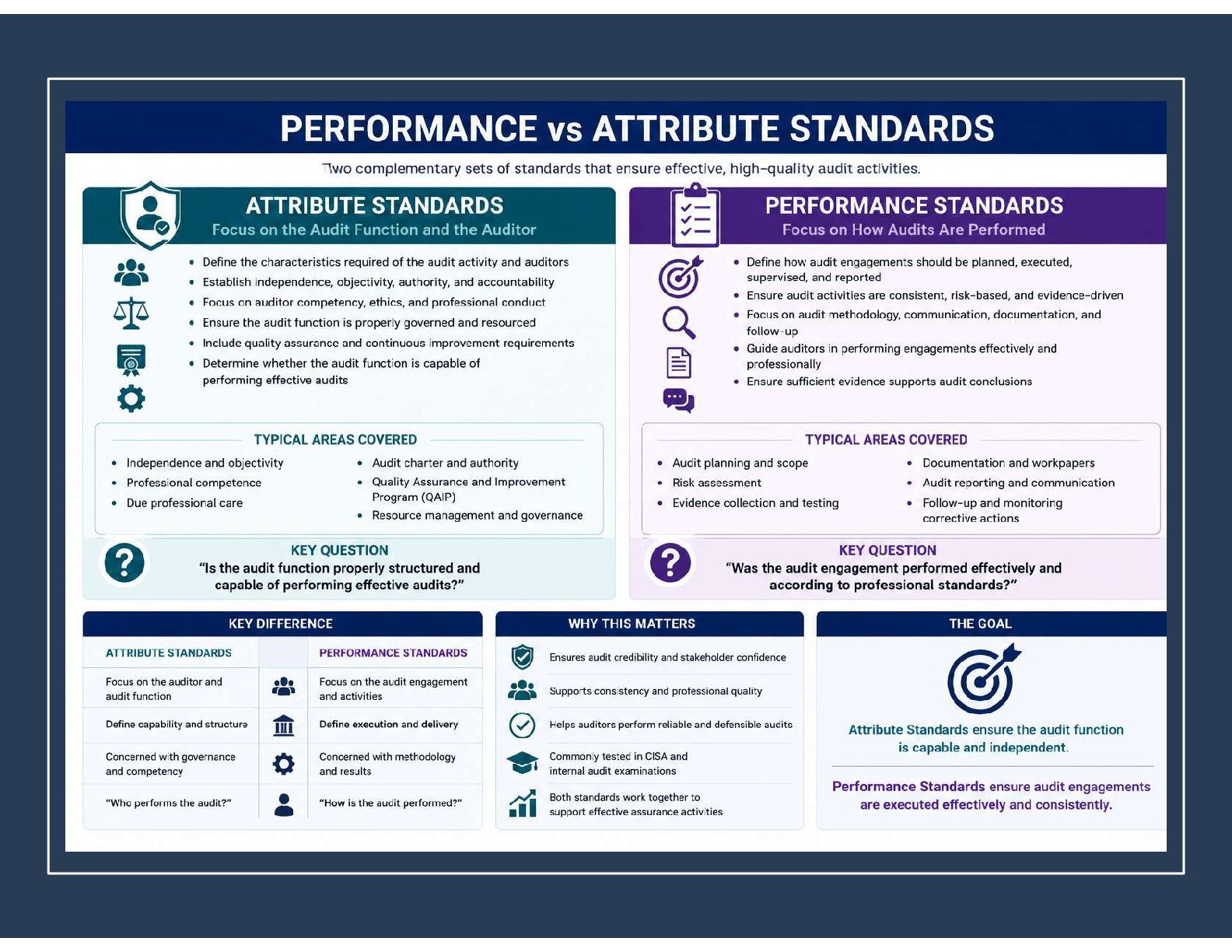

• Attribute vs Performance Standards

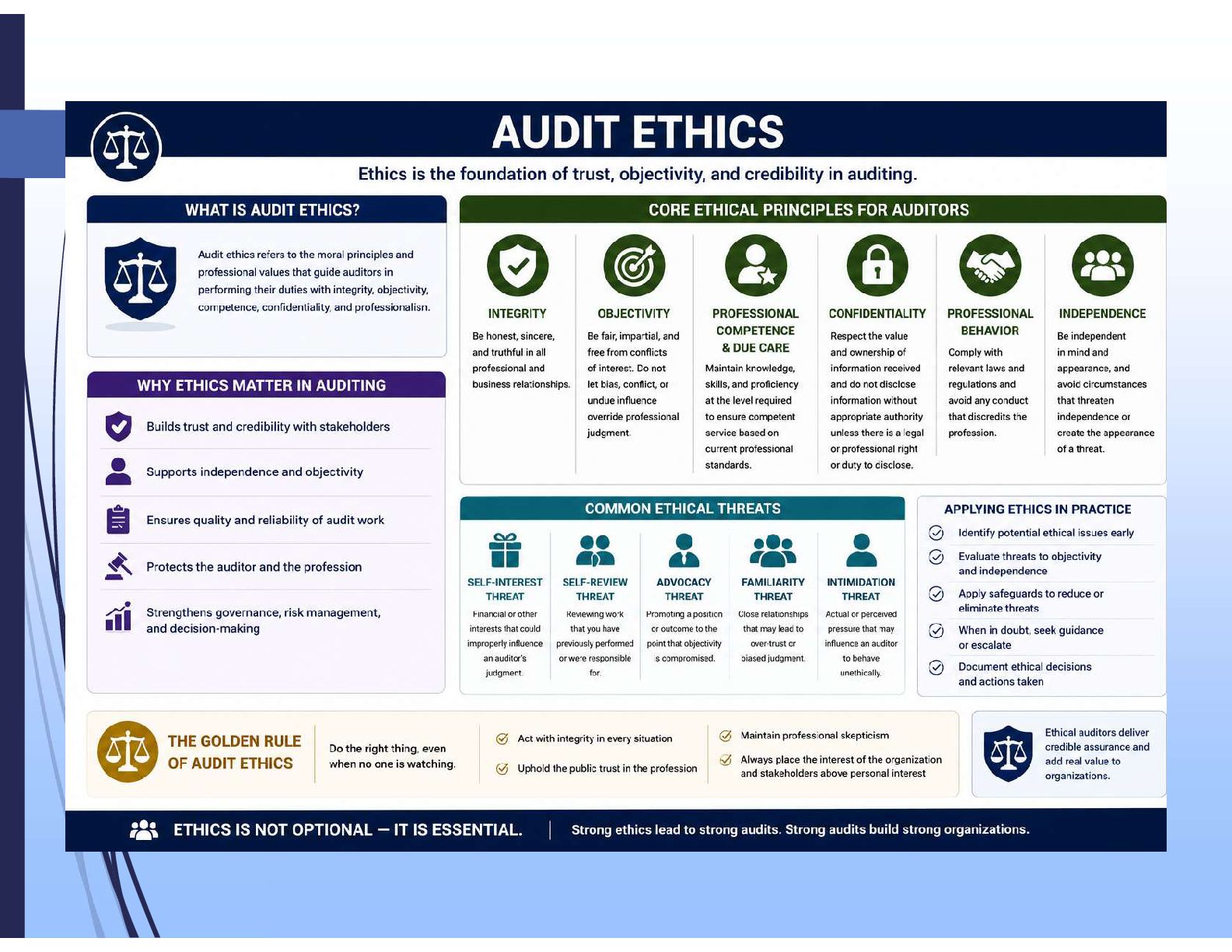

• Audit ethics and professional conduct

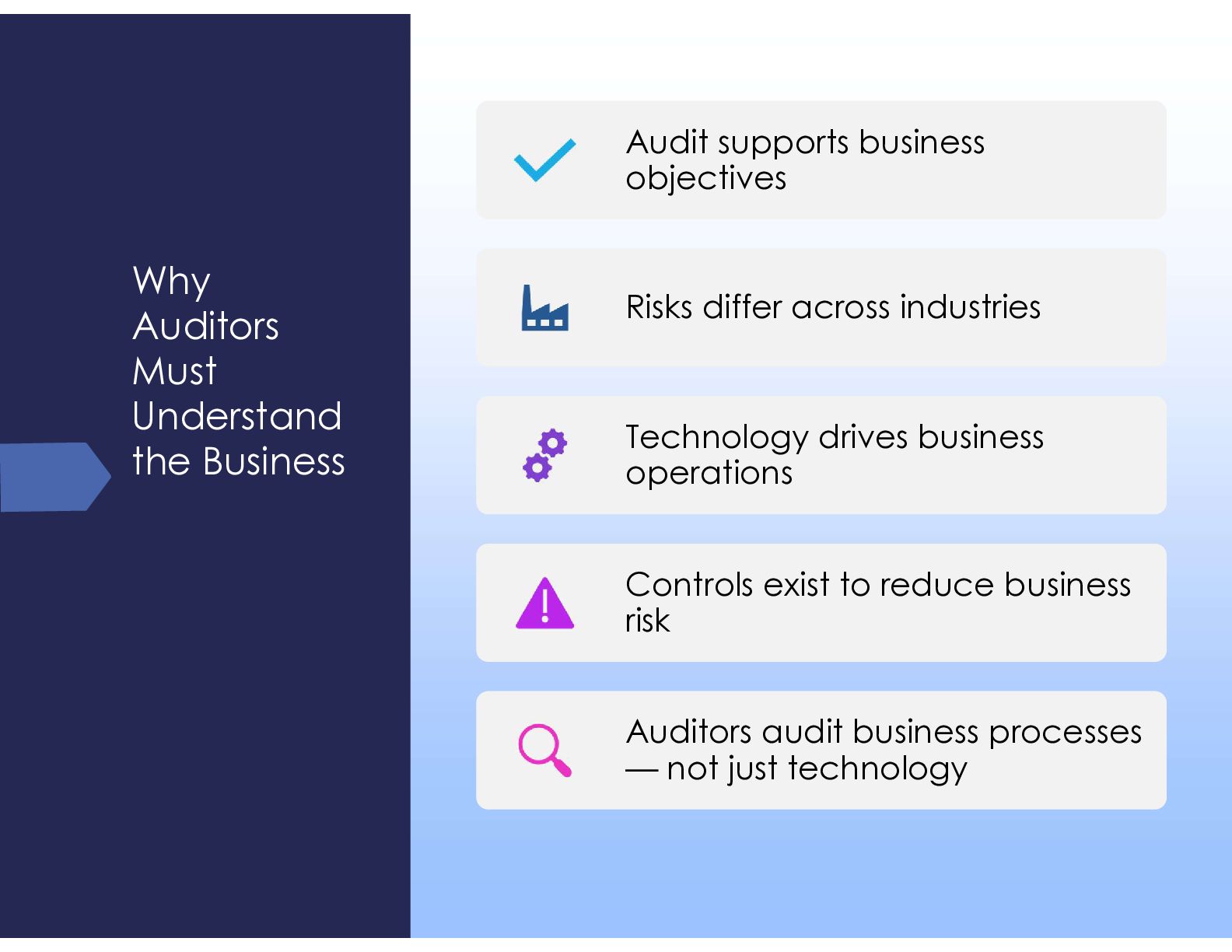

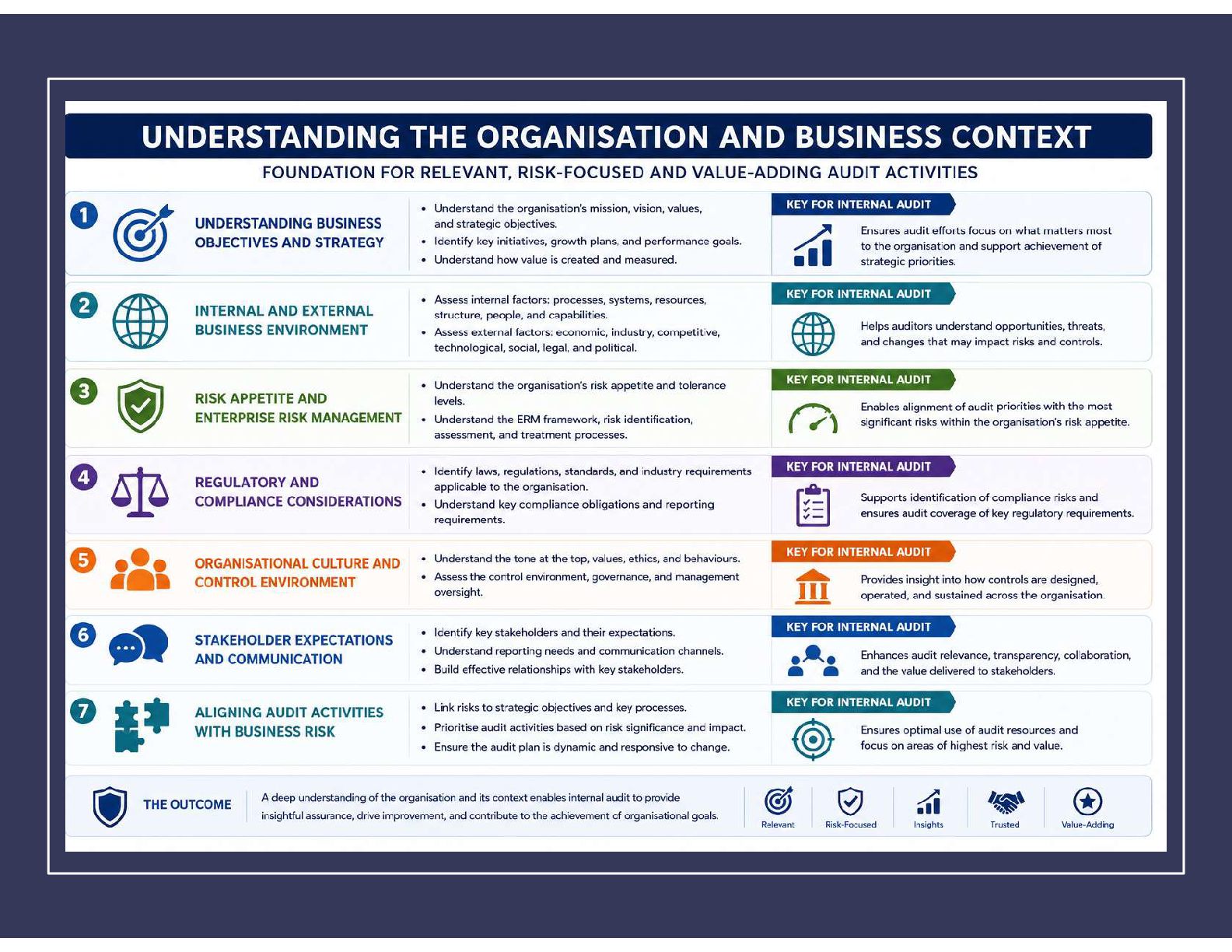

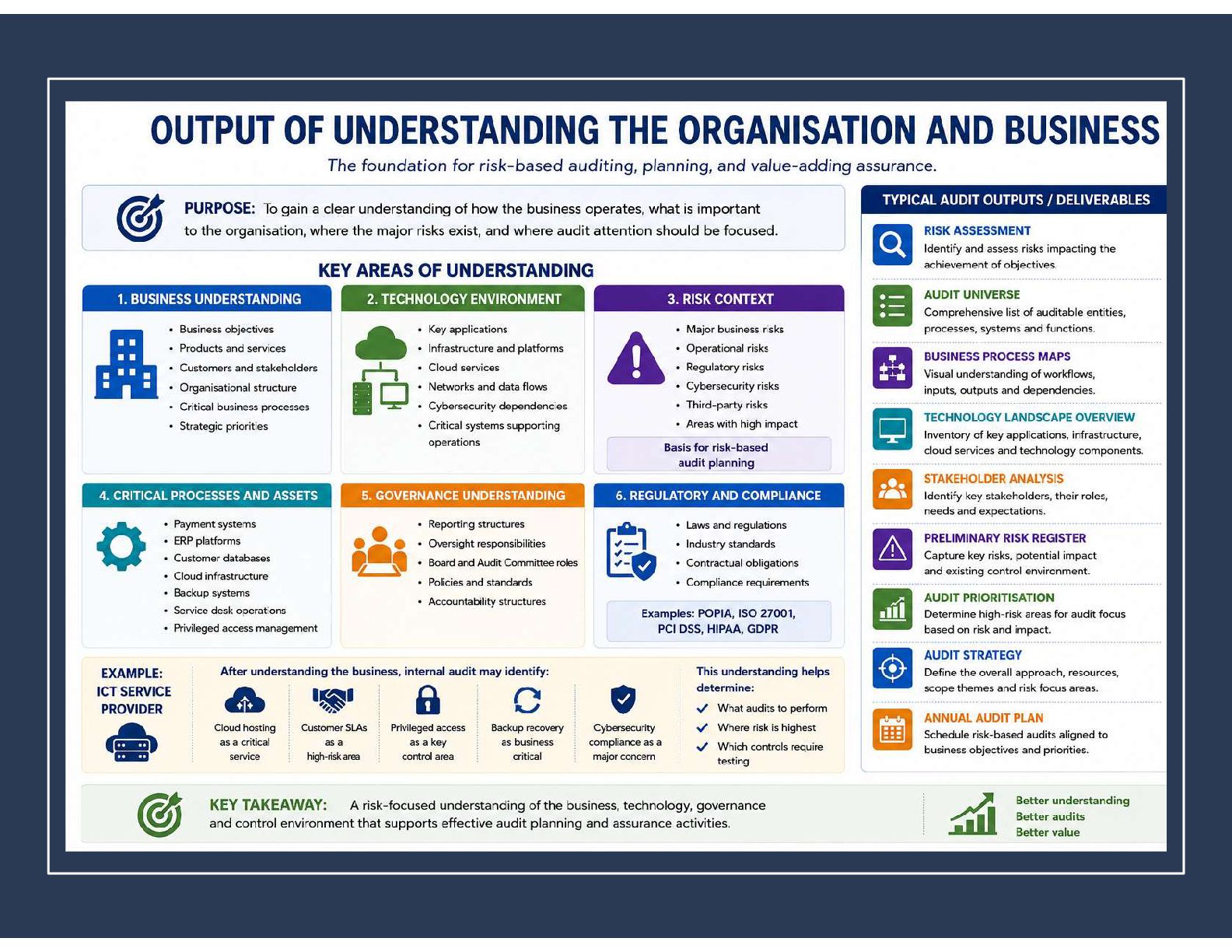

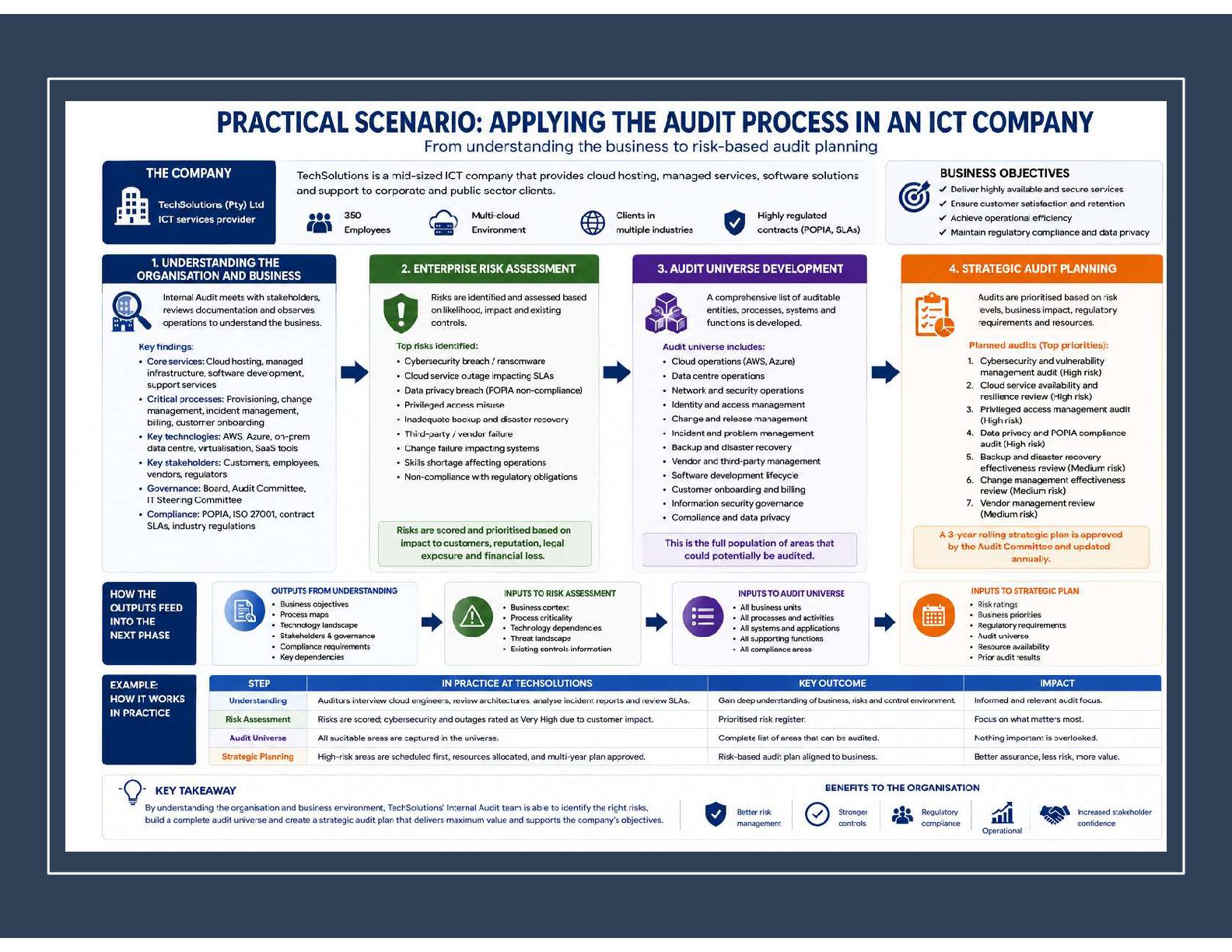

• Understanding the organisation and business environment

• How business understanding supports enterprise risk assessment, audit universe development, and strategic audit planning

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}