The AI chip market is experiencing remarkable expansion, projected to reach USD 341 billion by 2033, driven by an impressive CAGR of 31.2% during the forecast period. This growth is largely supported by rapid AI integration across industries and rising demand for high-performance computing hardware.

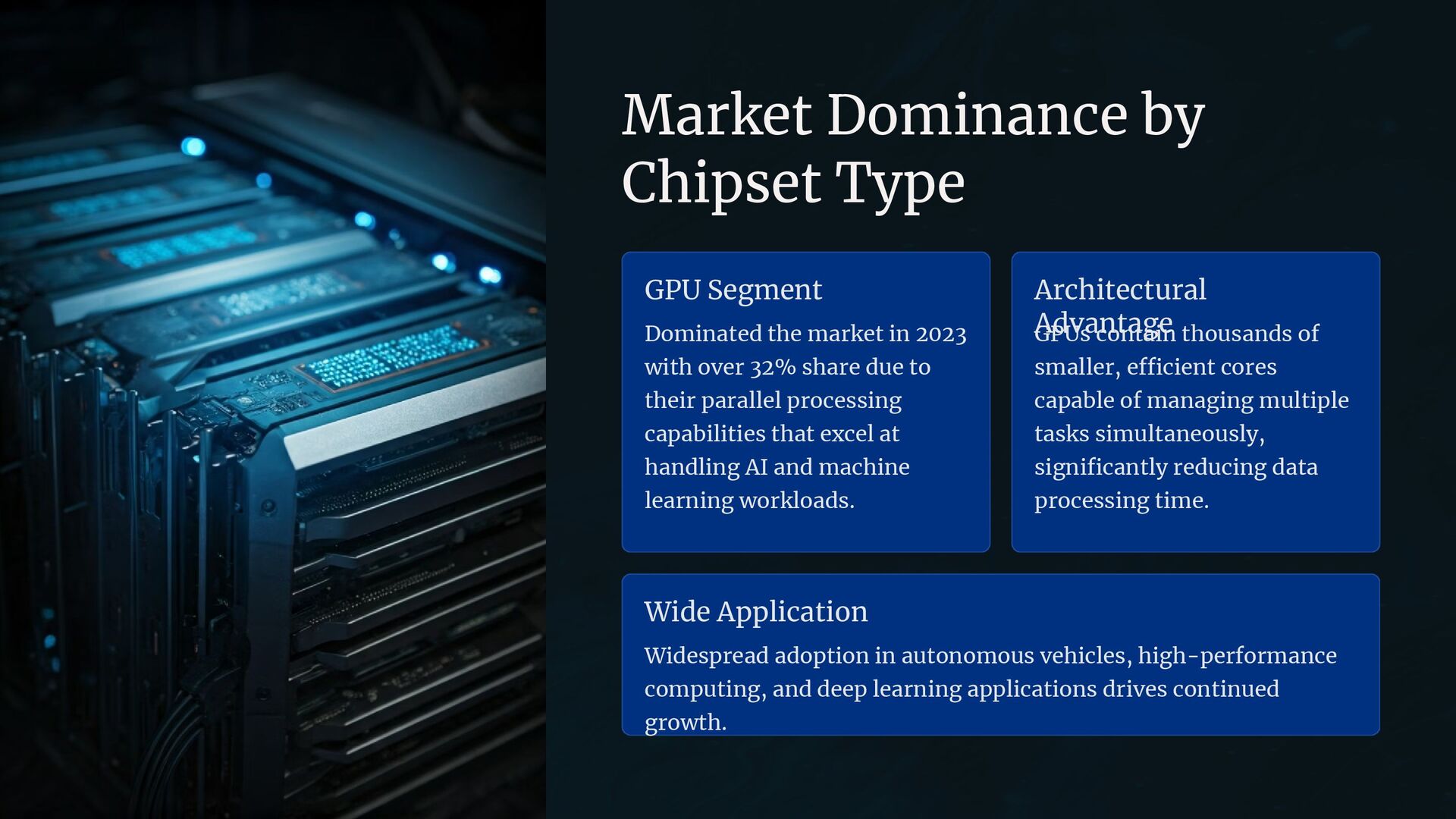

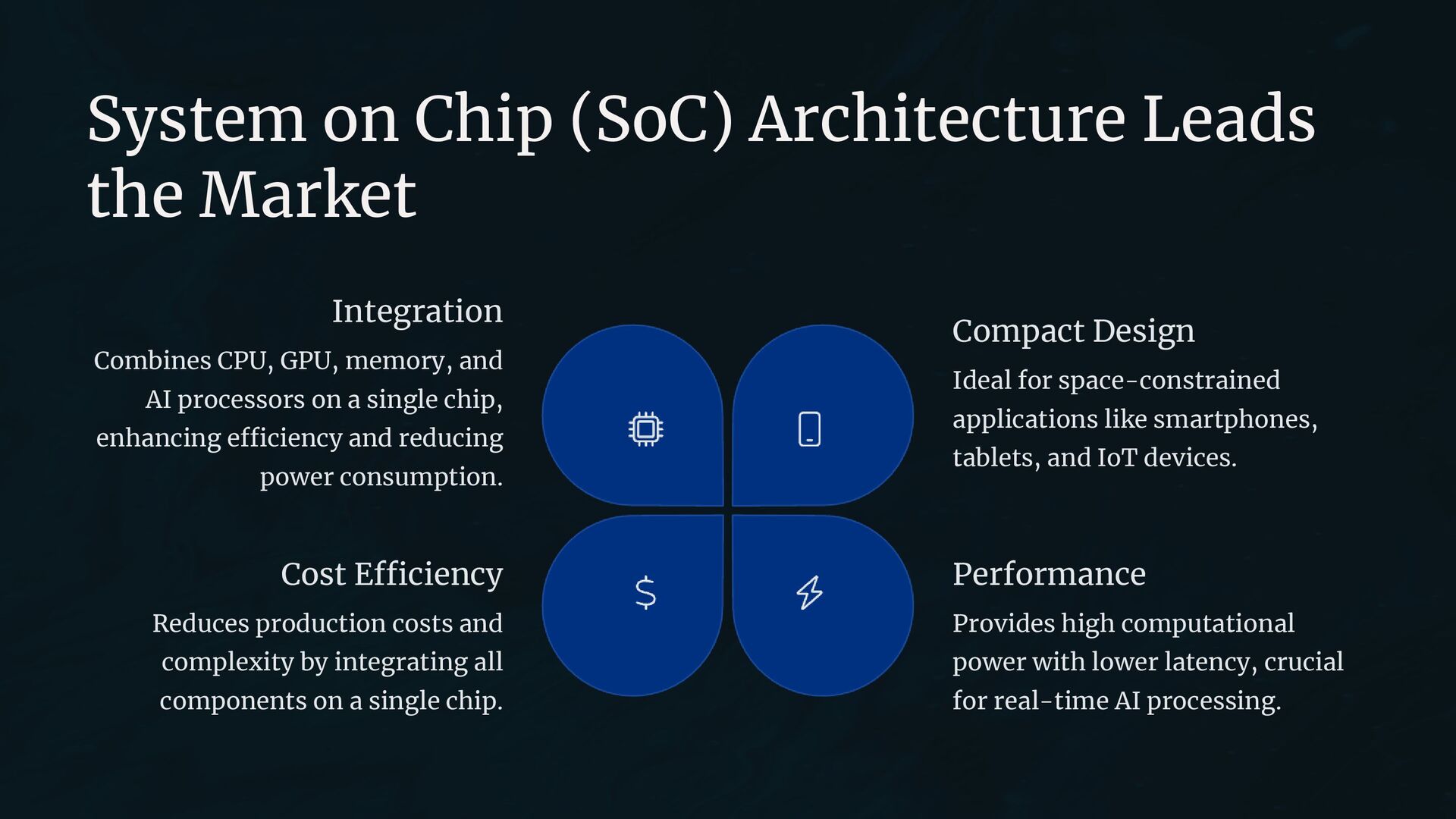

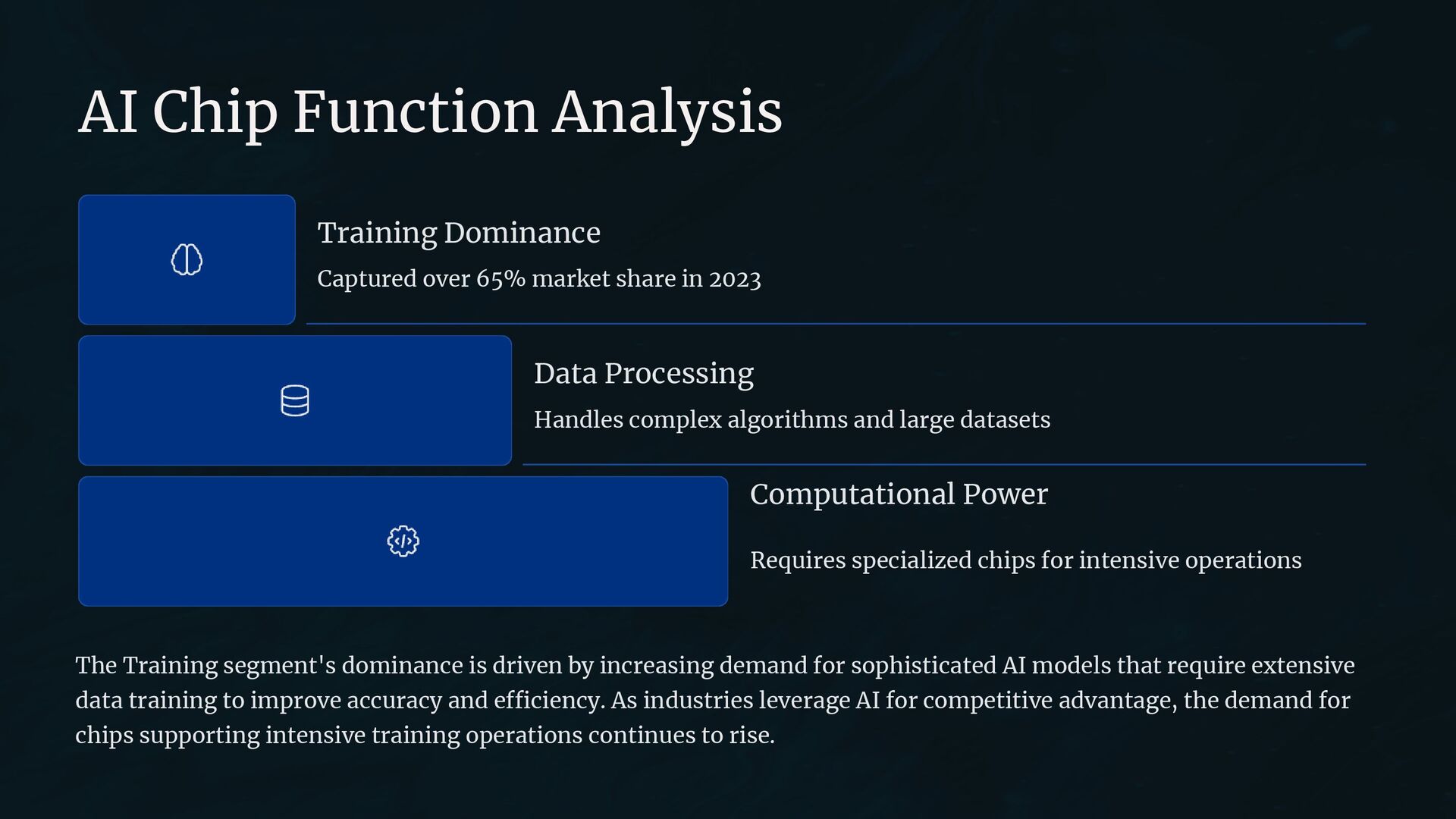

In 2023, the System on Chip (SoC) segment held the leading position with over 36% market share, reflecting its growing use in integrated AI solutions. Meanwhile, GPUs continued to dominate specialized AI workloads, accounting for more than 32% share. On the application side, the Training segment led the market with a commanding 65% share, emphasizing the need for powerful computational resources to develop AI models.

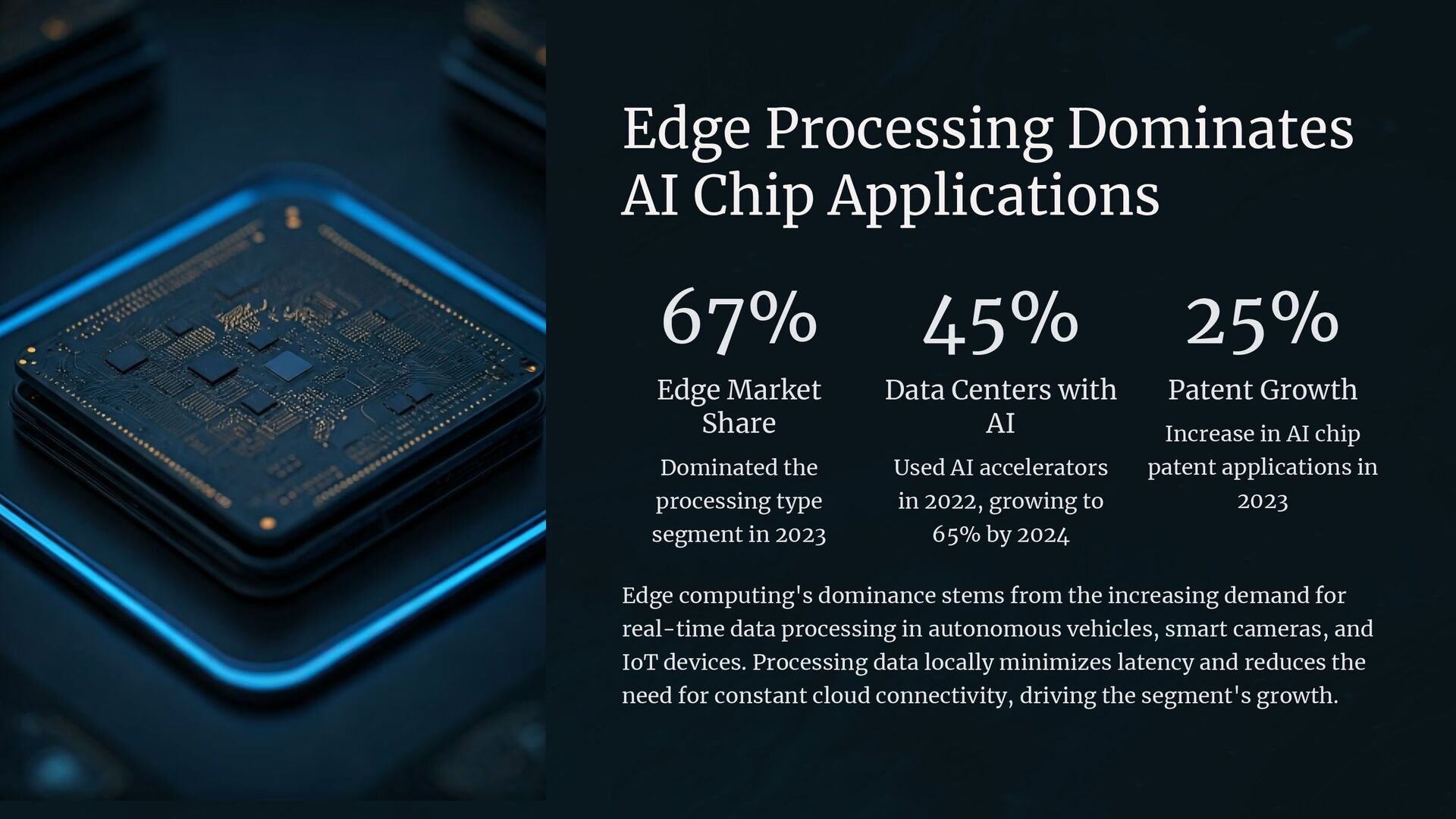

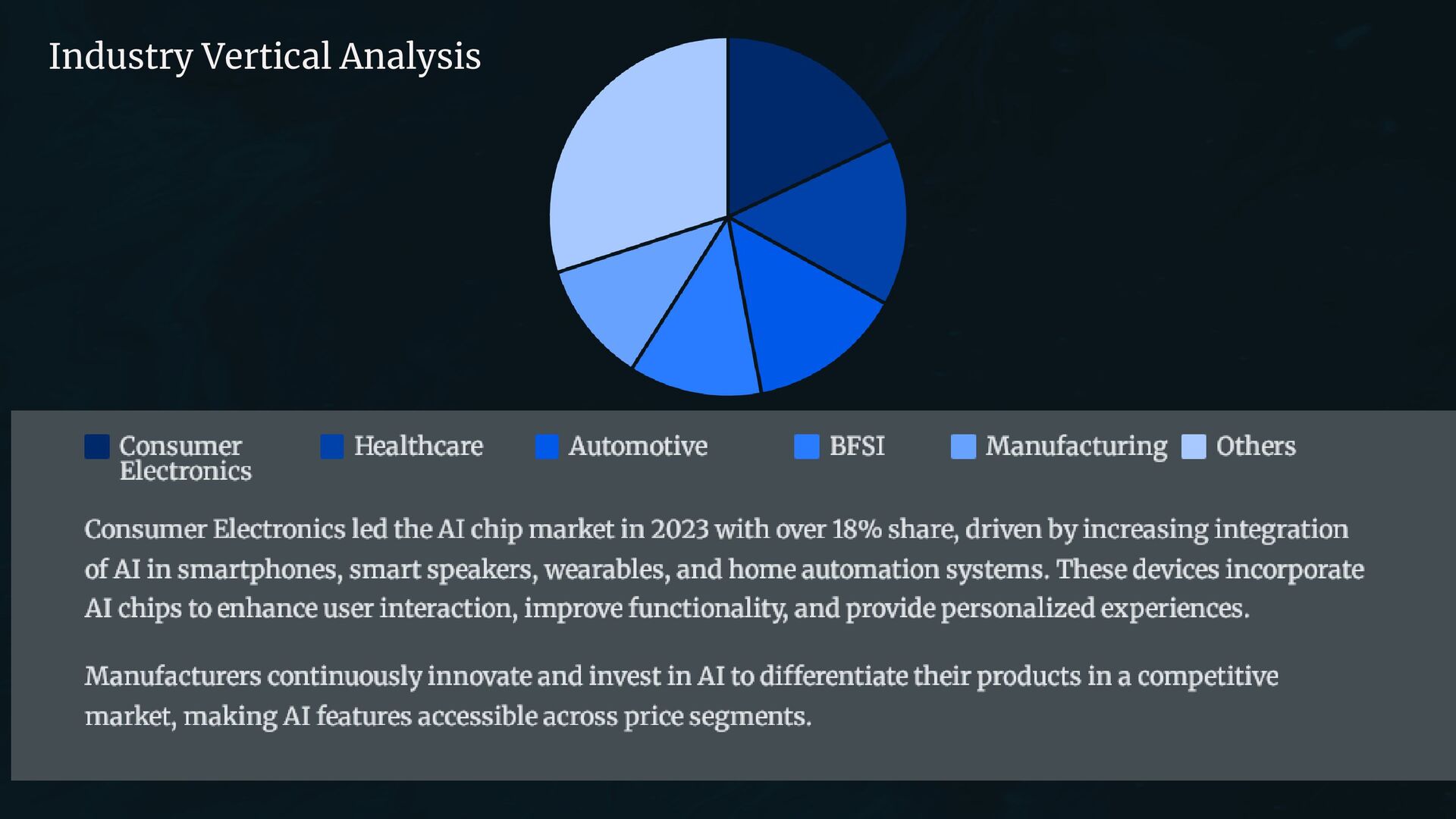

The Edge segment also secured a dominant share of more than 67%, indicating the increasing preference for real-time AI processing on devices. Within end-use sectors, Consumer Electronics emerged as the top contributor, holding over 18% market share, supported by AI features in smartphones, wearables, and smart home devices.

Discover More - https://market.us/report/ai-chip-market/

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}