The K-12 Education Technology (EdTech) market is on a strong growth path, expected to rise from USD 78.2 billion in 2023 to around USD 253.9 billion by 2033, advancing at a steady CAGR of 12.5% during the forecast period. This upward trend is fueled by increased digital adoption in classrooms, growing internet accessibility, and the need for personalized learning experiences.

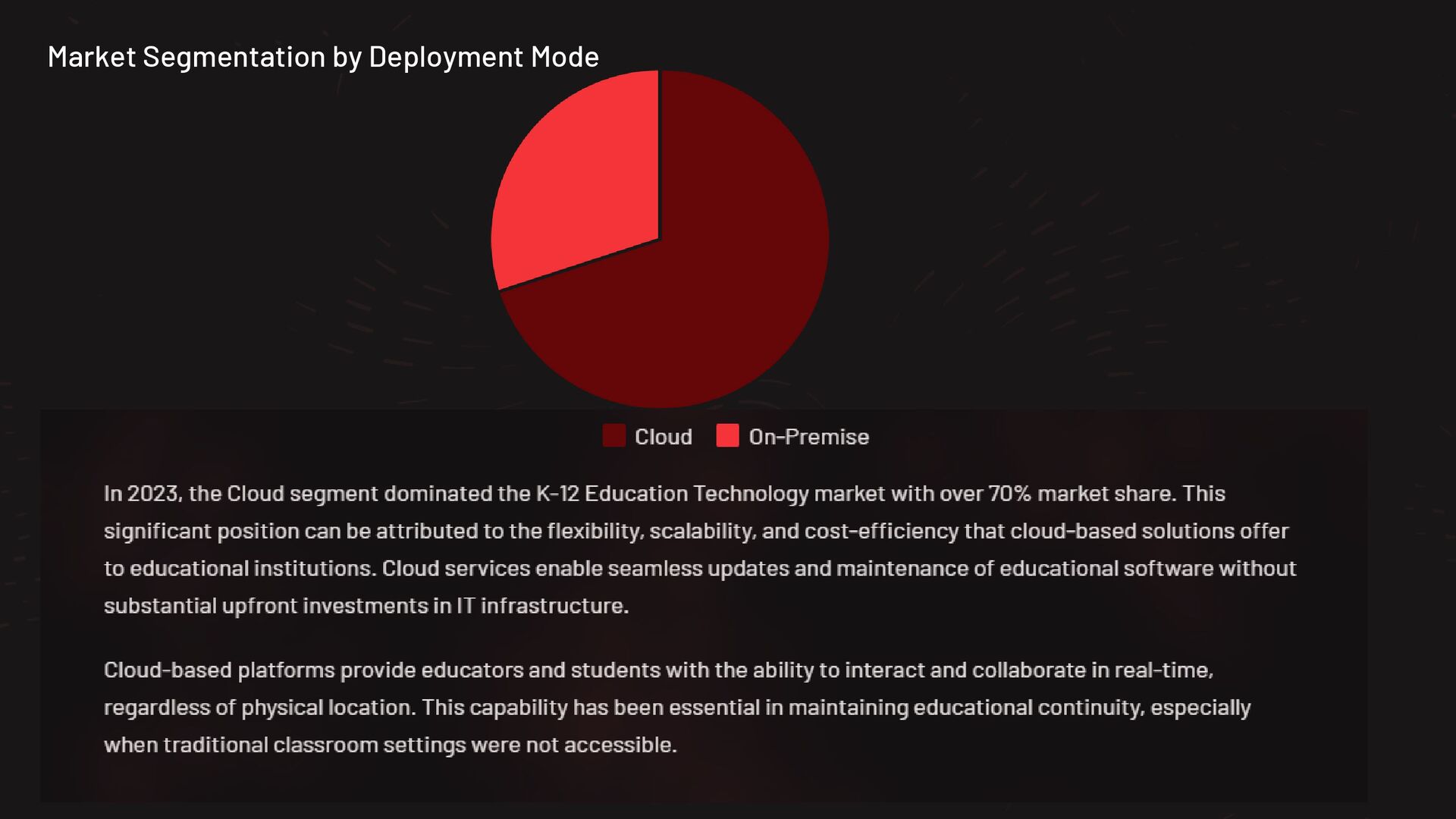

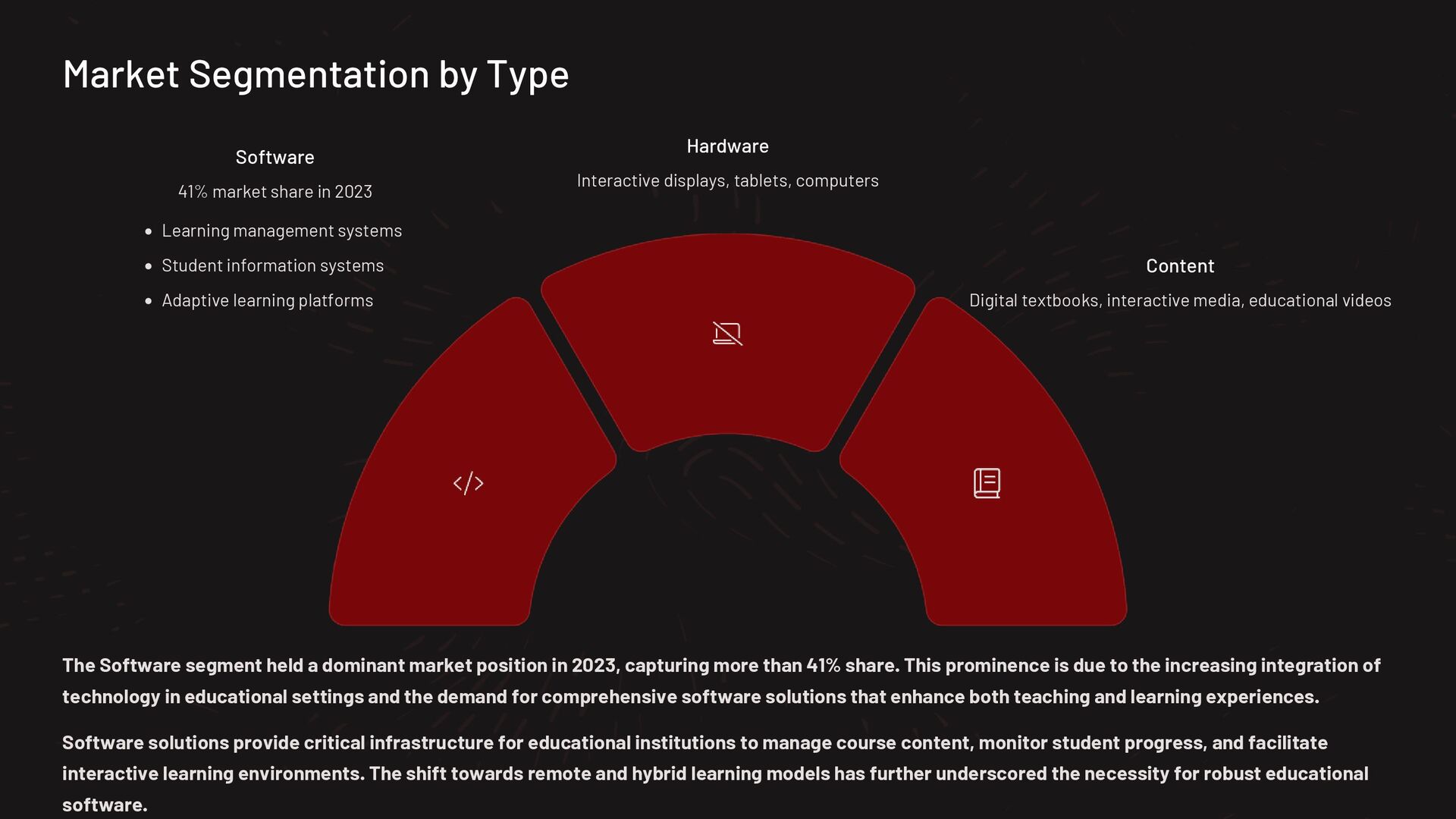

In 2023, the Cloud segment emerged as a key enabler of scalability and accessibility, capturing over 70% share, driven by the widespread integration of online platforms and learning management systems. Simultaneously, the Software segment held a significant share of more than 41%, reflecting the demand for digital curriculum tools, virtual classrooms, and assessment platforms.

The K-12 level continued to dominate the market structure, accounting for over 70% share, as schools increasingly invest in digital infrastructure and interactive content delivery. The Consumer segment led in terms of end-user adoption, holding a substantial share of over 80%, reflecting the growing reliance on home-based learning tools by parents and students.

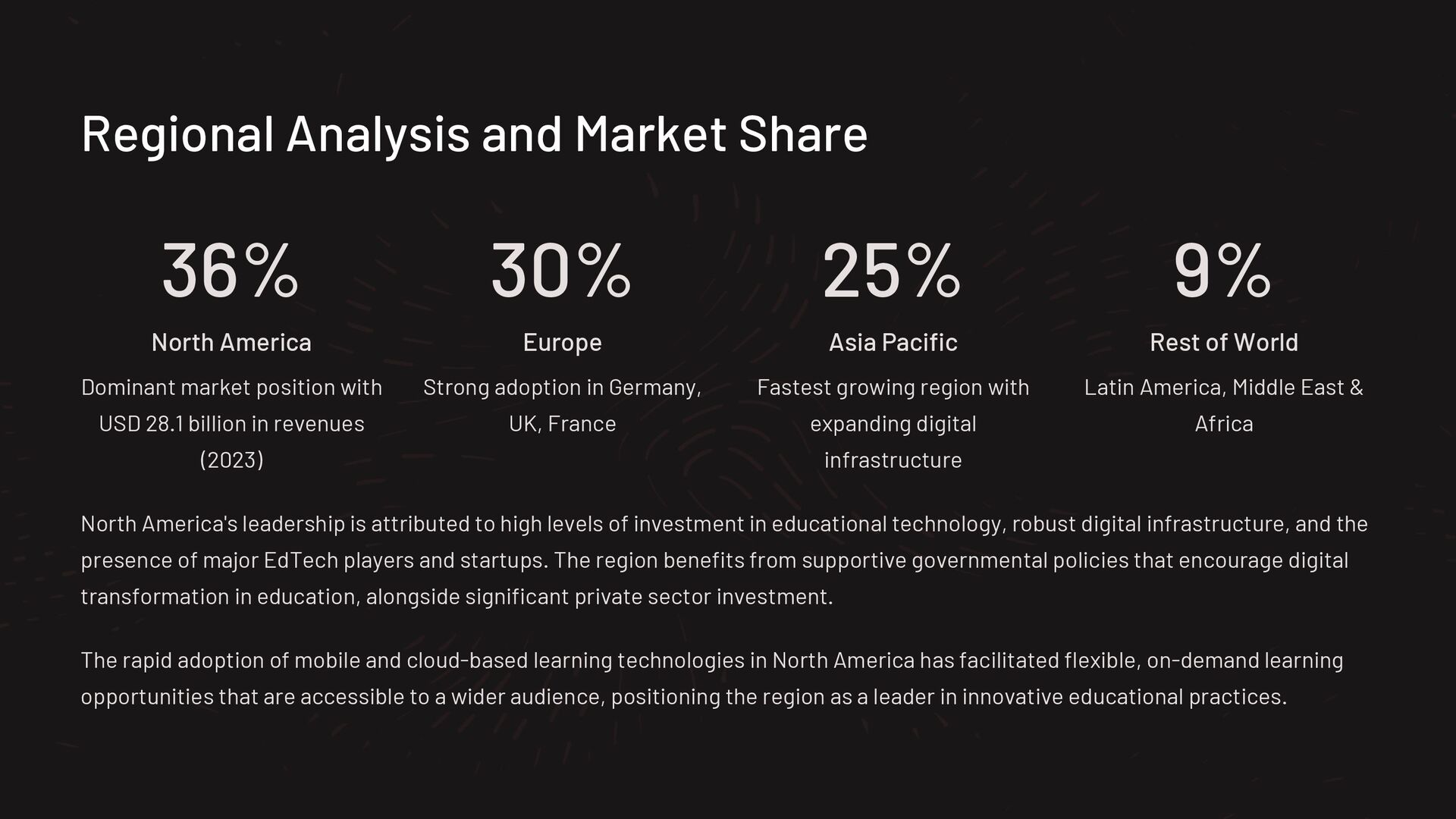

Regionally, North America remained the leading market in 2023, with over 36% share and revenues reaching approximately USD 28.1 billion, supported by advanced educational infrastructure, strong government funding, and high digital literacy across the region.

Read More - https://market.us/report/primary-edtech-market/

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}