their thoughts, sensitivities and talents to any and all that are in need of them. Our hope is that our service gives way to new projects, ideas and activities, as well as fair compensation for our valued merchants. Means of payment should be available to everyone in the world and beyond. As a company, we aim to provide each and every individual with the opportunity to freely transform their potential into value. Creating an economy for People through the Power of Payment. Payment to the People, Power to the People.

individuals at the forefront of society. We believe. Economic activity starts with the individual, supporting each and every person in their pursuit of happiness. What BASE makes are more than just tools. They are a social infrastructure, empowering people to be proactive and live life to the fullest, empowering people to be "owners of their lives". Together we thrive. We are All Owners. We are All Owners Foundation

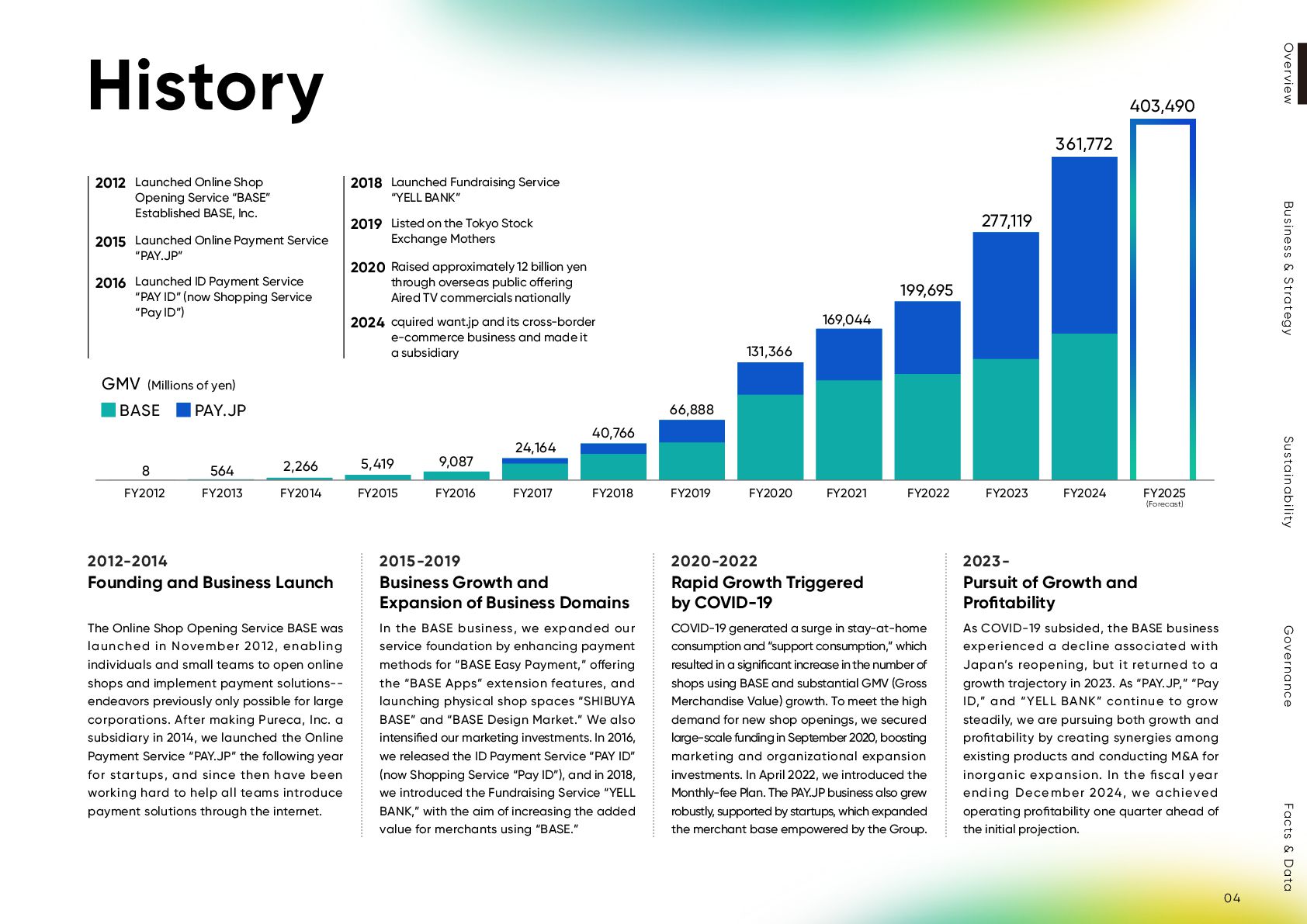

Shop Opening Service “BASE” Established BASE, Inc. 2015 Launched Online Payment Service “PAY.JP” 2016 Launched ID Payment Service “PAY ID” (now Shopping Service “Pay ID”) 2018 Launched Fundraising Service “YELL BANK” 2019 Listed on the Tokyo Stock Exchange Mothers 2020 Raised approximately 12 billion yen through overseas public o ering Aired TV commercials nationally 2024 cquired want.jp and its cross-border e-commerce business and made it a subsidiary 2012-2014 Founding and Business Launch 2015-2019 Business Growth and Expansion of Business Domains 2020-2022 Rapid Growth Triggered by COVID-19 2023- Pursuit of Growth and Profitability The Online Shop Opening Service BASE was launched in November 2012, enabling individuals and small teams to open online shops and implement payment solutions-- endeavors previously only possible for large corporations. After making Pureca, Inc. a subsidiary in 2014, we launched the Online Payment Service “PAY.JP” the following year for startups, and since then have been working hard to help all teams introduce payment solutions through the internet. In the BASE business, we expanded our service foundation by enhancing payment methods for “BASE Easy Payment,” o ering the “BASE Apps” extension features, and launching physical shop spaces “SHIBUYA BASE” and “BASE Design Market.” We also intensified our marketing investments. In 2016, we released the ID Payment Service “PAY ID” (now Shopping Service “Pay ID”), and in 2018, we introduced the Fundraising Service “YELL BANK,” with the aim of increasing the added value for merchants using “BASE.” COVID-19 generated a surge in stay-at-home consumption and “support consumption,” which resulted in a significant increase in the number of shops using BASE and substantial GMV (Gross Merchandise Value) growth. To meet the high demand for new shop openings, we secured large-scale funding in September 2020, boosting marketing and organizational expansion investments. In April 2022, we introduced the Monthly-fee Plan. The PAY.JP business also grew robustly, supported by startups, which expanded the merchant base empowered by the Group. As COVID-19 subsided, the BASE business experienced a decline associated with Japan’s reopening, but it returned to a growth trajectory in 2023. As “PAY.JP,” “Pay ID,” and “YELL BANK” continue to grow steadily, we are pursuing both growth and profitability by creating synergies among existing products and conducting M&A for inorganic expansion. In the fiscal year ending December 2024, we achieved operating profitability one quarter ahead of the initial projection. FY2012 FY2013 FY2014 FY2015 FY2016 FY2017 FY2018 FY2019 FY2020 FY2021 FY2022 FY2023 FY2025 (Forecast) FY2024 403,490 277,119 199,695 169,044 131,366 66,888 40,766 24,164 9,087 5,419 2,266 564 8 361,772 04 Business & Strategy Governance Sustainability Facts & Data Overview

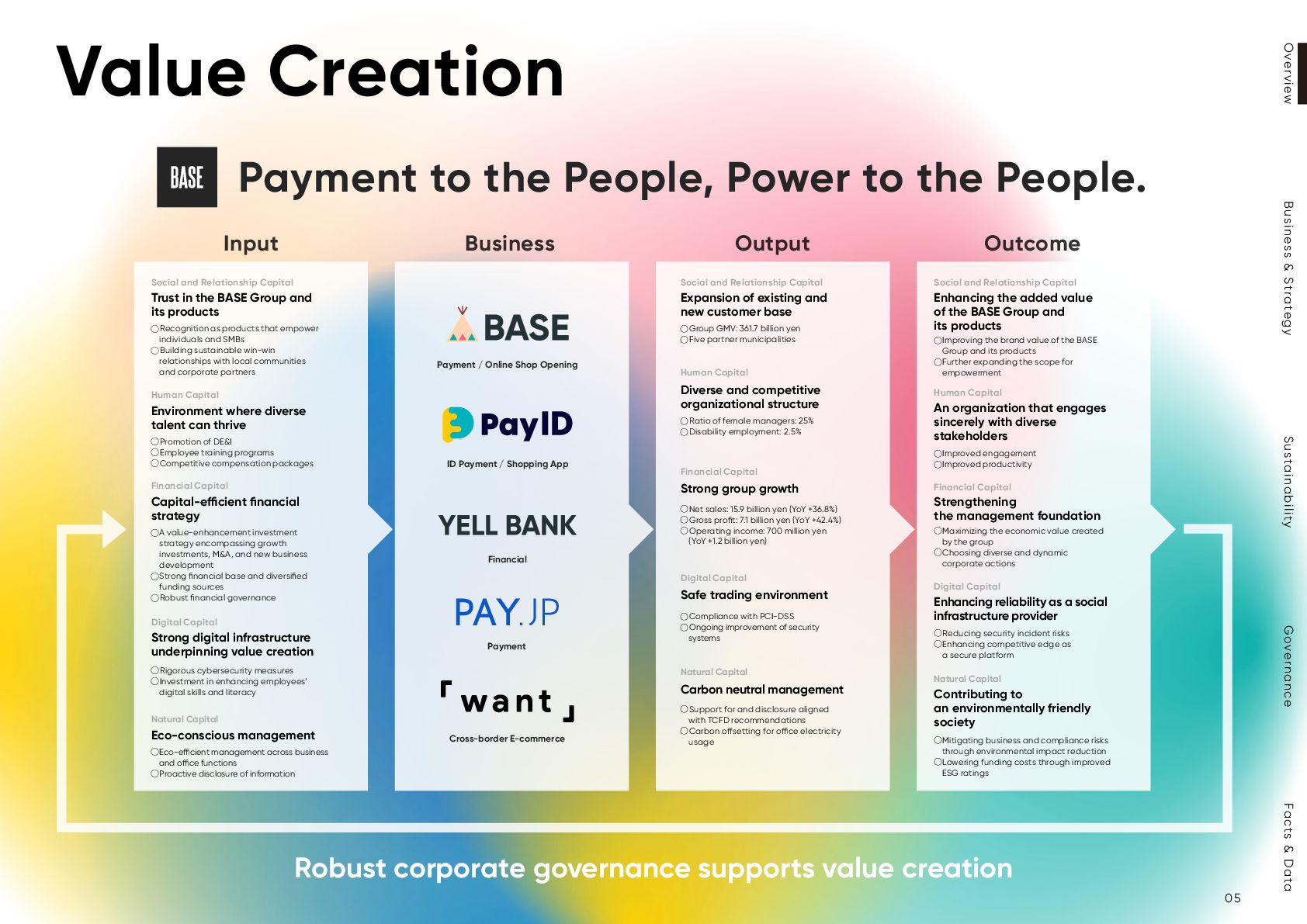

products ˓Further expanding the scope for ɹempowerment Input Business Output Outcome Value Creation Social and Relationship Capital Enhancing the added value of the BASE Group and its products ˓Improved engagement ˓Improved productivity Human Capital An organization that engages sincerely with diverse stakeholders ˓Maximizing the economic value created ɹby the group ˓Choosing diverse and dynamic ɹcorporate actions Financial Capital Strengthening the management foundation ˓Reducing security incident risks ˓Enhancing competitive edge as ɹa secure platform Digital Capital Enhancing reliability as a social infrastructure provider ˓Mitigating business and compliance risks ɹthrough environmental impact reduction ˓Lowering funding costs through improved ɹESG ratings Natural Capital Contributing to an environmentally friendly society Payment to the People, Power to the People. Robust corporate governance supports value creation ˓Group GMV: 361.7 billion yen ˓Five partner municipalities Social and Relationship Capital Expansion of existing and new customer base ˓Ratio of female managers: 25% ˓Disability employment: 2.5% Human Capital Diverse and competitive organizational structure ˓Net sales: 15.9 billion yen (YoY +36.8%) ˓Gross profit: 7.1 billion yen (YoY +42.4%) ˓Operating income: 700 million yen (YoY +1.2 billion yen) Financial Capital Strong group growth ˓Compliance with PCI-DSS ˓Ongoing improvement of security ɹsystems Digital Capital Safe trading environment ˓Support for and disclosure aligned ɹwith TCFD recommendations ˓Carbon o setting for o ce electricity ɹusage Natural Capital Carbon neutral management ID Payment / Shopping App Cross-border E-commerce Financial Payment / Online Shop Opening Payment ˓Recognition as products that empower ɹindividuals and SMBs ˓Building sustainable win-win ɹrelationships with local communities ɹand corporate partners Social and Relationship Capital Trust in the BASE Group and its products ˓Promotion of DE&I ˓Employee training programs ˓Competitive compensation packages Human Capital Environment where diverse talent can thrive ˓A value-enhancement investment ɹstrategy encompassing growth ɹinvestments, M&A, and new business ɹdevelopment ˓Strong financial base and diversified ɹfunding sources ˓Robust financial governance Financial Capital Capital-e cient financial strategy ˓Rigorous cybersecurity measures ˓Investment in enhancing employees’ ɹdigital skills and literacy Digital Capital Strong digital infrastructure underpinning value creation ˓Eco-e cient management across business ɹand o ce functions ˓Proactive disclosure of information Natural Capital Eco-conscious management 05 Business & Strategy Governance Sustainability Facts & Data Overview

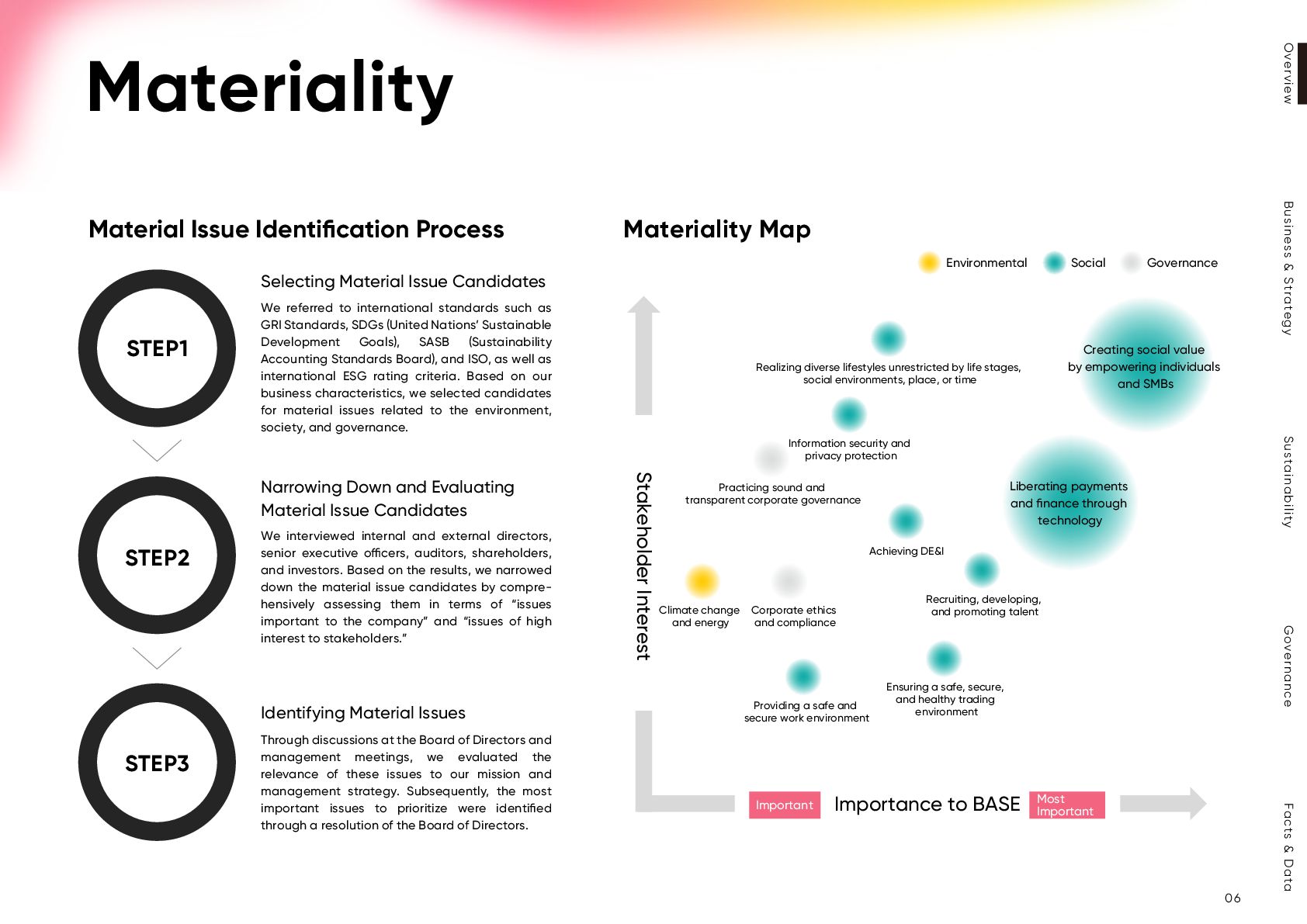

(United Nations’ Sustainable Development Goals), SASB (Sustainability Accounting Standards Board), and ISO, as well as international ESG rating criteria. Based on our business characteristics, we selected candidates for material issues related to the environment, society, and governance. Selecting Material Issue Candidates Materiality Through discussions at the Board of Directors and management meetings, we evaluated the relevance of these issues to our mission and management strategy. Subsequently, the most important issues to prioritize were identified through a resolution of the Board of Directors. Identifying Material Issues We interviewed internal and external directors, senior executive o cers, auditors, shareholders, and investors. Based on the results, we narrowed down the material issue candidates by compre- hensively assessing them in terms of “issues important to the company” and “issues of high interest to stakeholders.” Narrowing Down and Evaluating Material Issue Candidates STEP1 STEP2 STEP3 Material Issue Identification Process Environmental Social Governance Ensuring a safe, secure, and healthy trading environment Corporate ethics and compliance Practicing sound and transparent corporate governance Information security and privacy protection Climate change and energy Achieving DE&I Providing a safe and secure work environment Creating social value by empowering individuals and SMBs Liberating payments and finance through technology Realizing diverse lifestyles unrestricted by life stages, social environments, place, or time Materiality Map Importance to BASE Stakeholder Interest Important Most Important Recruiting, developing, and promoting talent 06 Business & Strategy Governance Sustainability Facts & Data Overview

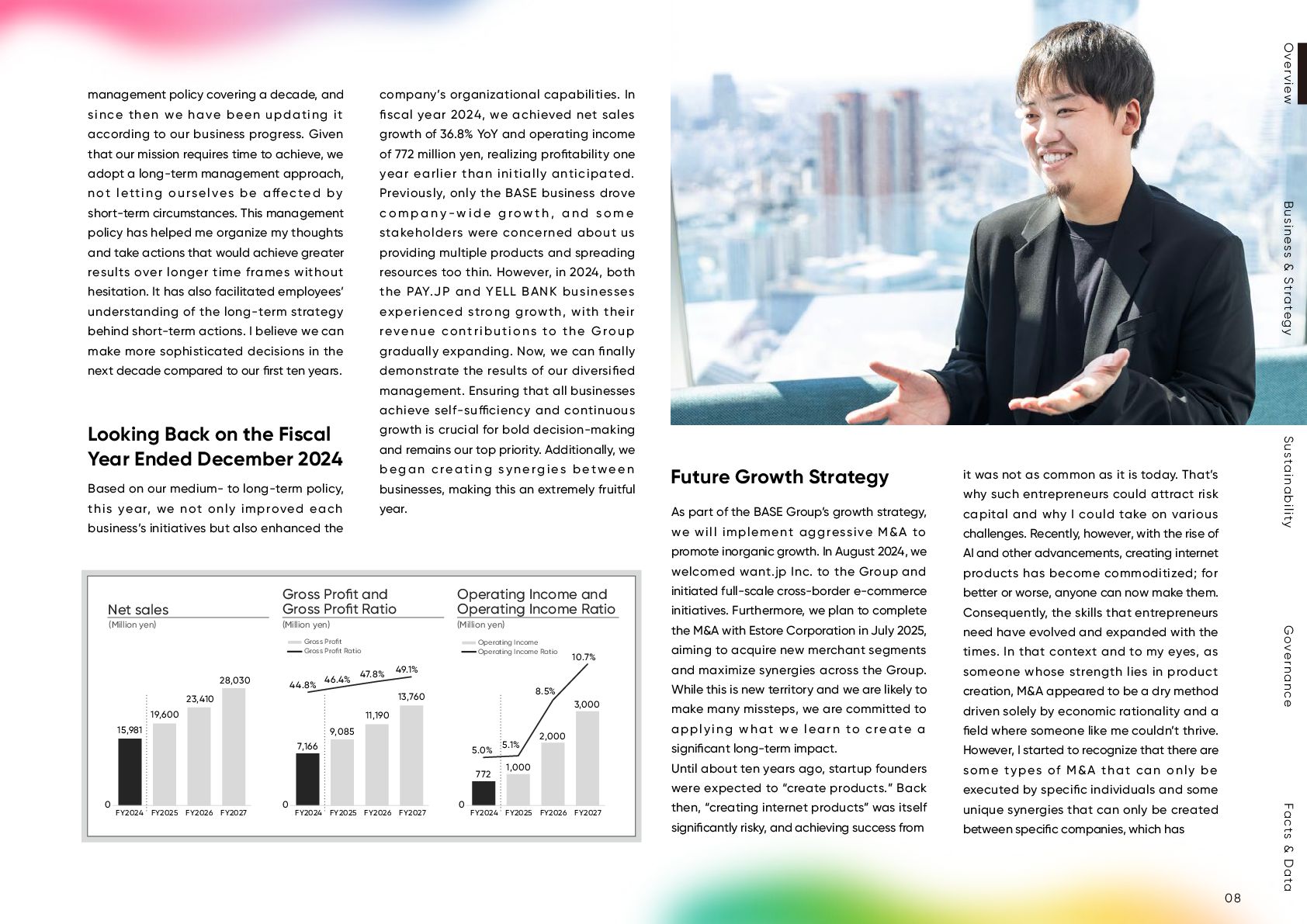

Expanding the BASE Group’s growth and profitability while restructuring the e-commerce and payment sectors to sustainably deliver value to society CEO Message Under our mission, “Payment to the People, Power to the People.” we uphold our core principle of empowering individuals, small teams, and startups. Our medium- to long-term management policy is founded on this mission, and we are committed to navigating the complex challenge of balancing top-line growth with improved profitability while delivering substantial value to society in a sustainable manner. Furthermore, in February 2025, we disclosed our first medium-term management plan. The plan targets net sales of 28 billion yen, gross profit of 13.7 billion yen, and operating income of 3 billion yen for the fiscal year ending December 2027. When BASE had approached its 10th anniversary, we developed a very long-term Medium- to Long-term Management Policy and Medium-term Management Plan Disclosure Objectives 07 Business & Strategy Governance Sustainability Facts & Data Overview

been updating it according to our business progress. Given that our mission requires time to achieve, we adopt a long-term management approach, not letting ourselves be a ected by short-term circumstances. This management policy has helped me organize my thoughts and take actions that would achieve greater results over longer time frames without hesitation. It has also facilitated employees’ understanding of the long-term strategy behind short-term actions. I believe we can make more sophisticated decisions in the next decade compared to our first ten years. Based on our medium- to long-term policy, this year, we not only improved each business’s initiatives but also enhanced the company’s organizational capabilities. In fiscal year 2024, we achieved net sales growth of 36.8% YoY and operating income of 772 million yen, realizing profitability one year earlier than initially anticipated. Previously, only the BASE business drove c o m p a n y - w i d e g ro w t h , a n d s o m e stakeholders were concerned about us providing multiple products and spreading resources too thin. However, in 2024, both the PAY.JP and YELL BANK businesses experienced strong growth, with their revenue contributions to the Group gradually expanding. Now, we can finally demonstrate the results of our diversified management. Ensuring that all businesses achieve self-su ciency and continuous growth is crucial for bold decision-making and remains our top priority. Additionally, we began creating synergies between businesses, making this an extremely fruitful year. Looking Back on the Fiscal Year Ended December 2024 As part of the BASE Group’s growth strategy, we will implement aggressive M&A to promote inorganic growth. In August 2024, we welcomed want.jp Inc. to the Group and initiated full-scale cross-border e-commerce initiatives. Furthermore, we plan to complete the M&A with Estore Corporation in July 2025, aiming to acquire new merchant segments and maximize synergies across the Group. While this is new territory and we are likely to make many missteps, we are committed to applying what we learn to create a significant long-term impact. Until about ten years ago, startup founders were expected to “create products.” Back then, “creating internet products” was itself significantly risky, and achieving success from it was not as common as it is today. That’s why such entrepreneurs could attract risk capital and why I could take on various challenges. Recently, however, with the rise of AI and other advancements, creating internet products has become commoditized; for better or worse, anyone can now make them. Consequently, the skills that entrepreneurs need have evolved and expanded with the times. In that context and to my eyes, as someone whose strength lies in product creation, M&A appeared to be a dry method driven solely by economic rationality and a field where someone like me couldn’t thrive. However, I started to recognize that there are some types of M&A that can only be executed by specific individuals and some unique synergies that can only be created between specific companies, which has Future Growth Strategy 772 1,000 2,000 3,000 5.0% 5.1% 8.5% 10.7% 0 FY2024 FY2025 FY2026 FY2027 Operating Income Operating Income Ratio (Million yen) (Million yen) (Million yen) 15,981 19,600 23,410 28,030 0 FY2024 FY2025 FY2026 FY2027 7,166 9,085 11,190 13,760 44.8% 46.4% 47.8% 49.1% 0 FY2024 FY2025 FY2026 FY2027 Gross Profit Gross Profit Ratio Net sales Gross Profit and Gross Profit Ratio Operating Income and Operating Income Ratio 08 Business & Strategy Governance Sustainability Facts & Data Overview

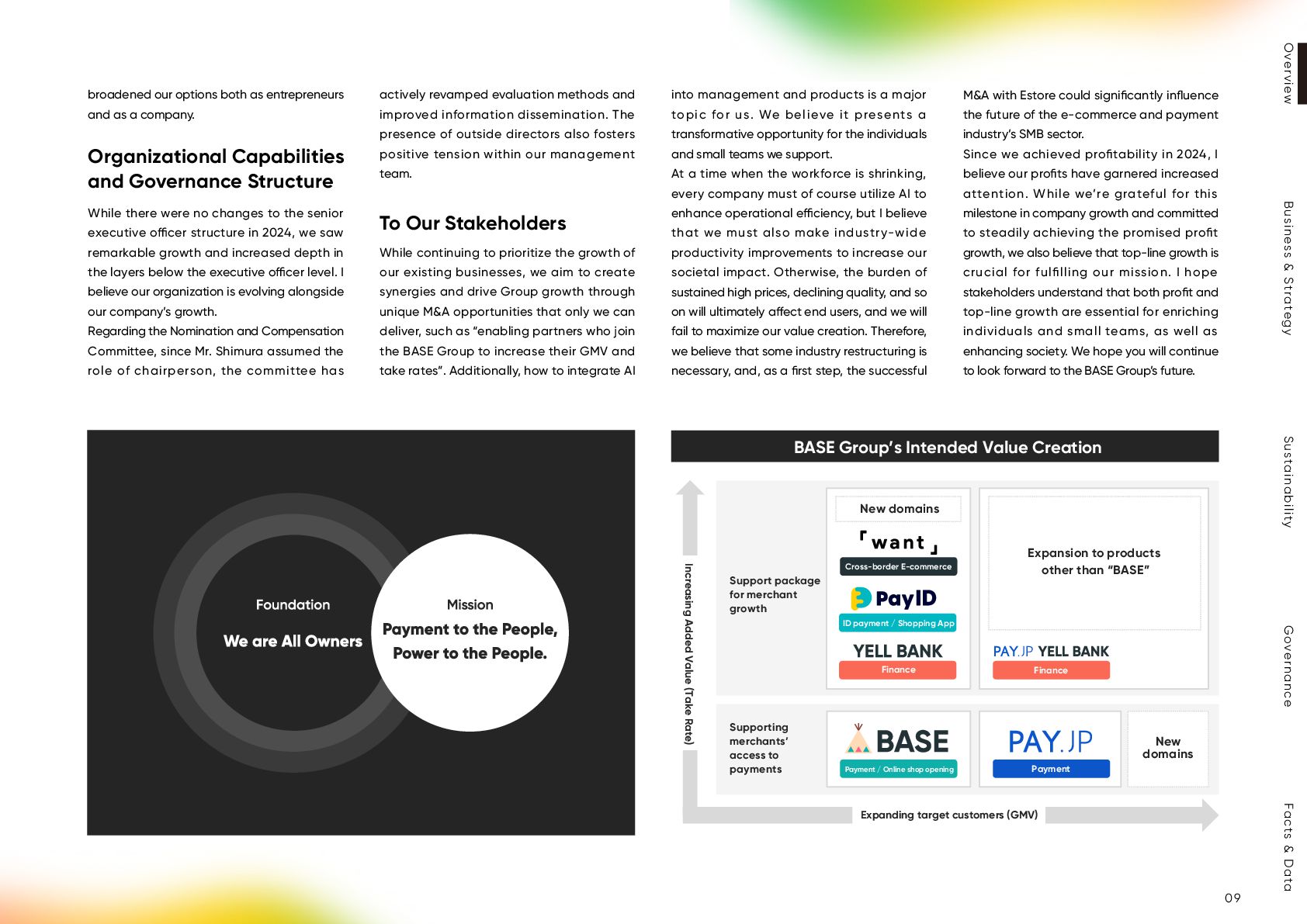

While there were no changes to the senior executive o cer structure in 2024, we saw remarkable growth and increased depth in the layers below the executive o cer level. I believe our organization is evolving alongside our company’s growth. Regarding the Nomination and Compensation Committee, since Mr. Shimura assumed the role of chairperson, the committee has actively revamped evaluation methods and improved information dissemination. The presence of outside directors also fosters positive tension within our management team. While continuing to prioritize the growth of our existing businesses, we aim to create synergies and drive Group growth through unique M&A opportunities that only we can deliver, such as “enabling partners who join the BASE Group to increase their GMV and take rates”. Additionally, how to integrate AI into management and products is a major topic for us. We believe it presents a transformative opportunity for the individuals and small teams we support. At a time when the workforce is shrinking, every company must of course utilize AI to enhance operational e ciency, but I believe that we must also make industry-wide productivity improvements to increase our societal impact. Otherwise, the burden of sustained high prices, declining quality, and so on will ultimately a ect end users, and we will fail to maximize our value creation. Therefore, we believe that some industry restructuring is necessary, and, as a first step, the successful M&A with Estore could significantly influence the future of the e-commerce and payment industry’s SMB sector. Since we achieved profitability in 2024, I believe our profits have garnered increased attention. While we’re grateful for this milestone in company growth and committed to steadily achieving the promised profit growth, we also believe that top-line growth is crucial for fulfilling our mission. I hope stakeholders understand that both profit and top-line growth are essential for enriching individuals and small teams, as well as enhancing society. We hope you will continue to look forward to the BASE Group’s future. Organizational Capabilities and Governance Structure To Our Stakeholders ID payment / Shopping App Expanding target customers (GMV) Expansion to products other than “BASE” Payment / Online shop opening New domains Payment Finance BASE Group’s Intended Value Creation Support package for merchant growth Increasing Added Value (Take Rate) New domains Cross-border E-commerce Finance Supporting merchants’ access to payments 09 Business & Strategy Governance Sustainability Facts & Data Overview

business and creating business synergies Overall, I believe we took the first step toward achieving a balance between growth and profitability this year. While we had previously focused on growth, we also began to improve profitability. Although they are in di erent growth phases, in 2024, we improved cost e ciency in both the BASE and PAY.JP businesses. For the BASE business, we focused on improving profitability through enhanced take rates and cost e ciency. Product upselling played a key role, with GMV increasing by 13% YoY and the take rate improving as expected. Consequently, we achieved growth exceeding the overall market average, which was encouraging. For the PAY.JP business, while the market’s average growth rate in the payment service provider (PSP) is 10-15%, we achieved remarkable top-line growth of 47% YoY. By optimizing both pricing and costs, we secured a 130% YoY increase in gross profit, driving the Group’s top-line growth. Additionally, as our first attempt to create synergies between Group businesses, we Senior Executive O cer COO Nao Takahashi COO Message Looking Back on the Fiscal Year Ended December 2024 10 Business & Strategy Governance Sustainability Facts & Data Overview

PAY.JP’s functionality, adding financial capabilities alongside standard payment processing updates has been a major milestone. It’s rare for a PSP in Japan to expand into in-house financial services, and we were able to take the lead in this area. While the PAY.JP business drove top-line growth, the YELL BANK business contributed to profits over the year. It’s well known that we significantly expanded the existing YELL BANK service for shops using BASE. In addition to that, we have developed a comprehensive product lineup, including PoC, that contributes in many ways to cash flow improvements for the long-tail segment. Factoring alone remains a niche with limited target shops, but we’re working on product additions and updates to expand its user base. Rather than assembling a full lineup like a bank, we’re adding products that seem likely to contribute significantly to the long tail and SMEs. With YELL BANK alone, we can only support the deposit side for shops, which is insu cient; however, by expanding to withdrawal-side products, we believe our overall financial capabilities have increased. In 2024, we launched Pay ID 3-installment Post Pay, a BNPL installment payment service for Pay ID. While this business is in an earlier phase compared to our other products, we’re steadily moving toward our Group goal of building a “two-sided network” of merchants and purchasers to provide in-house payment services. As standard functions for payment products in the Japanese market, we need to support not only convenience store payments but also account transfers, and not just lump-sum payments (monthly clearance) but also installment payments. With these releases, we now o er the same functionality as credit cards, the most widely used payment method in Japan. In this sense, Pay ID Post Pay has finally become a full-fledged payment service this year. Furthermore, we’re preparing for shopping app monetization and associated product and perception improvements. For the BASE business, I believe the growth factor was that the value proposition of our product exceeded market expectations. For the PAY.JP business, even as payment processing industry players, including US companies, increasingly target enterprises, our consistent niche strategy of focusing on long-tail merchants has proven successful. Over the past several years, we’ve acquired merchants with significant future growth potential, and the robust growth of these promising merchants has greatly enhanced PAY.JP’s business growth. We will continue to aim for maximizing value creation through (1) expanding our target customers and (2) enhancing added value. Primarily, BASE and PAY.JP will drive (1), while YELL BANK and Pay ID will lead (2). The BASE business will pursue GMV growth while expanding the added value of its products and introducing new add-on features. Monetizing the Pay ID App will also help improve the take rate. To achieve this, we’ll continue to enhance our products so that shops can experience the customer acquisition benefits of the app. The PAY.JP business will continue to pursue growth in GMV while also seeking synergies across the Group in financial and other areas. Additionally, with METI leading e orts to strengthen countermeasures against fraudulent payments, we will also emphasize fraud detection. Furthermore, as our target users have broadened, increasing the diversity of payment method needs, we’re considering expanding beyond credit cards. We’re also promoting product enhancements and marketing strategies to improve new merchant acquisition. By adopting alternative approaches to bolster the PAY.JP business, distinct from the brand awareness strategies that we implemented for the BASE business until a few years ago, we’re now gradually starting to see results. For the YELL BANK business, we will enhance our e orts for product lineup expansion and external deployment. While YELL BANK has experienced strong growth recently, it remains a niche service within the broader financial services sector, with a limited user base. Therefore, when deploying externally, we aim to o er comprehensive financial services for the long tail and SMEs, addressing wider user needs. External deployment will require some time, but we plan to move forward steadily. From the business progress of PAY.JP YELL BANK, launched in 2024, we have learned that adjusting services according to merchant sales scale is essential. We will modify service design, rates, and other factors to suit the characteristics of merchants on each platform. For the want.jp business, we’ll proceed with development on schedule to provide features jointly developed with the BASE business. We expect to deliver these several years earlier than if the BASE business proceeded alone. We aim to leverage want.jp’s expertise in international shipping and platform deployment in various countries for shops that use BASE as well. Balancing growth and profitability is not easy, but group management makes this an attainable goal. It’s crucial to have multiple businesses in di erent phases, each growing steadily. As the new COO, I believe I’m expected to consolidate business decision-making and accelerate execution, so I’ll focus on these areas. Furthermore, I will regain momentum by refocusing on our mission. By leveraging synergies with Estore and other initiatives, we’ll progressively address the gaps in our value creation strategy diagram and build a sustainable growth foundation. We look forward to your continued support and expectations. To Our Stakeholders, as the New COO Reasons for Above-Market Growth Medium- to Long-term Management Policy and Fiscal Year Ending December 2025 Policy 11 Business & Strategy Governance Sustainability Facts & Data Overview

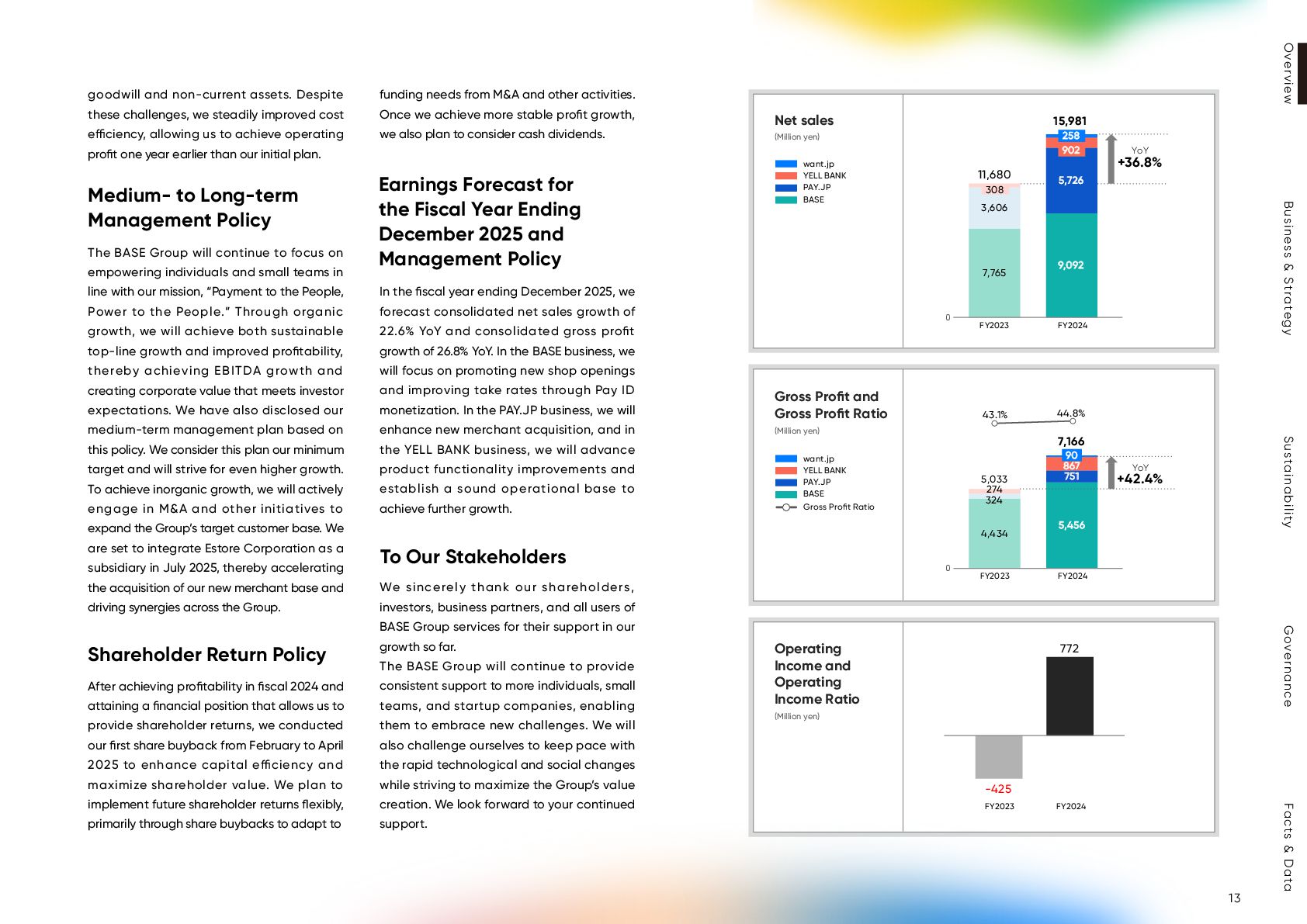

both top-line growth and improved profitability across the entire Group. Group-wide GMV saw strong year-over-year growth, and the YELL BANK business exceeded our anticipated growth rates, resulting in consolidated net sales of 36.8% YoY and consolidated gross profit of 42.4% YoY, surpassing our performance forecasts. Meanwhile, external environmental changes such as sudden fluctuations in foreign exchange rates and operational policy adjustments at certain overseas e-commerce platforms significantly impacted the want.jp business, leading to impairment of Director and Senior Executive O cer, CFO Ken Harada CFO Message Reflecting on the Fiscal Year Ended December 2024 Achieving sustainable growth and profitability improvement, expanding target customers, including through inorganic growth, and accelerating synergy creation 12 Business & Strategy Governance Sustainability Facts & Data Overview

more stable profit growth, we also plan to consider cash dividends. In the fiscal year ending December 2025, we forecast consolidated net sales growth of 22.6% YoY and consolidated gross profit growth of 26.8% YoY. In the BASE business, we will focus on promoting new shop openings and improving take rates through Pay ID monetization. In the PAY.JP business, we will enhance new merchant acquisition, and in the YELL BANK business, we will advance product functionality improvements and establish a sound operational base to achieve further growth. We sincerely thank our shareholders, investors, business partners, and all users of BASE Group services for their support in our growth so far. The BASE Group will continue to provide consistent support to more individuals, small teams, and startup companies, enabling them to embrace new challenges. We will also challenge ourselves to keep pace with the rapid technological and social changes while striving to maximize the Group’s value creation. We look forward to your continued support. goodwill and non-current assets. Despite these challenges, we steadily improved cost e ciency, allowing us to achieve operating profit one year earlier than our initial plan. The BASE Group will continue to focus on empowering individuals and small teams in line with our mission, “Payment to the People, Power to the People.” Through organic growth, we will achieve both sustainable top-line growth and improved profitability, thereby achieving EBITDA growth and creating corporate value that meets investor expectations. We have also disclosed our medium-term management plan based on this policy. We consider this plan our minimum target and will strive for even higher growth. To achieve inorganic growth, we will actively engage in M&A and other initiatives to expand the Group’s target customer base. We are set to integrate Estore Corporation as a subsidiary in July 2025, thereby accelerating the acquisition of our new merchant base and driving synergies across the Group. After achieving profitability in fiscal 2024 and attaining a financial position that allows us to provide shareholder returns, we conducted our first share buyback from February to April 2025 to enhance capital e ciency and maximize shareholder value. We plan to implement future shareholder returns flexibly, primarily through share buybacks to adapt to Medium- to Long-term Management Policy Shareholder Return Policy Earnings Forecast for the Fiscal Year Ending December 2025 and Management Policy To Our Stakeholders (Million yen) (Million yen) (Million yen) Net sales Gross Profit and Gross Profit Ratio Operating Income and Operating Income Ratio want.jp YELL BANK PAY.JP BASE want.jp YELL BANK PAY.JP BASE Gross Profit Ratio 4,434 5,456 324 751 274 867 90 5,033 7,166 43.1% 44.8% 0 FY2023 FY2024 YoY +36.8% YoY +42.4% 7,765 9,092 3,606 5,726 308 902 258 11,680 15,981 0 FY2023 FY2024 -425 772 FY2023 FY2024 13 Business & Strategy Governance Sustainability Facts & Data Overview

o ers optimal pricing plans to all individuals and small teams running online shops. The non monthly-fee plan, which incurs no fixed costs as shop owners pay fees only when they make sales, is perfect for small businesses and first-time online shop owners. For shops that exceed a certain sales volume, we o er a monthly-fee plan that includes a fixed monthly charge and, in return, features a lower sales fee, helping online businesses reduce operating costs as they scale. “BASE Easy Payment” – Instantly Ready for Use Our “BASE Easy Payment” system allows shops to start selling immediately after launch. It eliminates the need for complex screenings and procedures, and, once set up, supports a variety of payment methods, including credit cards, BNPL “Post Pay (Pay ID),” and bank transfers. This significantly shortens the time between opening an online shop and generating revenue. Wide-Ranging Features and Services Tailored to Sales Volume We provide a wide range of features tailored to each shop’s business scale. In addition to the standard features necessary for basic online shop management, advanced features can be easily added through the “BASE Apps” extensions. We also o er extensive support that includes assistance with opening o ine shops— such as pop-up stores—in addition to online shops, and access to our fundraising service “YELL BANK” that provides shop owners with funding by purchasing their future receivables. (See page 17 for details.) Shopping Service "Pay ID" We partner with “Pay ID,” a shopping service for purchasers that has over 16 million cumulative user registrations. Through “Pay ID,” purchasers enjoy a seamless online payment experience at the shops using “BASE.” At the same time, shops can leverage the service as a powerful sales promotion tool, driving repeat purchases and increasing the average order value. (See page 18 for details.) GMV Growth We will strengthen the opening of new shops by stepping up promotion e orts, including mass market-oriented initiatives, targeting a wide range of latent users. Furthermore, through joint development with the want.jp business, we aim to swiftly launch cross-border e-commerce services to attract overseas customers. Improving Profitability We will enhance extension features that boost shop sales and convenience, such as logistics, marketing, and cross-border e-commerce, through BASE’s proprietary tools and partnerships with external platforms. In addition, we will leverage the “Pay ID” shopping application to acquire new customers and increase the average purchase value. Characteristics Growth Strategy 15 Business & Strategy Governance Sustainability Facts & Data Overview

simple and highly flexible online payment system that enables startups to easily integrate payment services into their websites. Its intuitive dashboard and clear, well-designed API support a smooth implementation process from the initial steps, enabling a quick transition from account registration to integration and live operation. Even startups and companies in the early stages of launching a new business—who may not have the time and resources to integrate payment features—can swiftly begin operations using this system. Strengthening of Payment Features We will advance initiatives to introduce new payment methods, develop more easily-integrable payment systems, and strengthen fraud prevention measures. In addition, by expanding the “PAY.JP Platform,” we will actively work to attract new platform merchants. Upgrading the Group’s Unique Features We will di erentiate ourselves from the competition by strengthening value-added services in the financial domain, such as “PAY.JP YELL BANK.” Enhancing Marketing and Support for Existing Merchants We will diversify the merchant acquisition channels through enhanced sales and marketing measures, while also promoting continued use by building stronger relationships with existing large-scale merchants. Flexible and Reasonable Pricing Structure The system o ers a flexible pricing structure tailored to business size, with a range of options, from a no-monthly fee Standard Plan to an Enterprise Plan designed for high-volume merchants. Robust Security Compliant with Global Standards “PAY.JP” is fully compliant with PCI DSS Version 4.0, the global security standard for the industry, ensuring the highest level of information security. Since credit card information is tokenized and transmitted directly to “PAY.JP,” merchants are not required to retain or process any card data, significantly lowering the risk of information leakage. Furthermore, by consistently strengthening security measures, such as real-time fraud monitoring and regular security audits, the system provides a reliable infrastructure that ensures safe use at all times. Characteristics Growth Strategy 16 Business & Strategy Governance Sustainability Facts & Data Overview

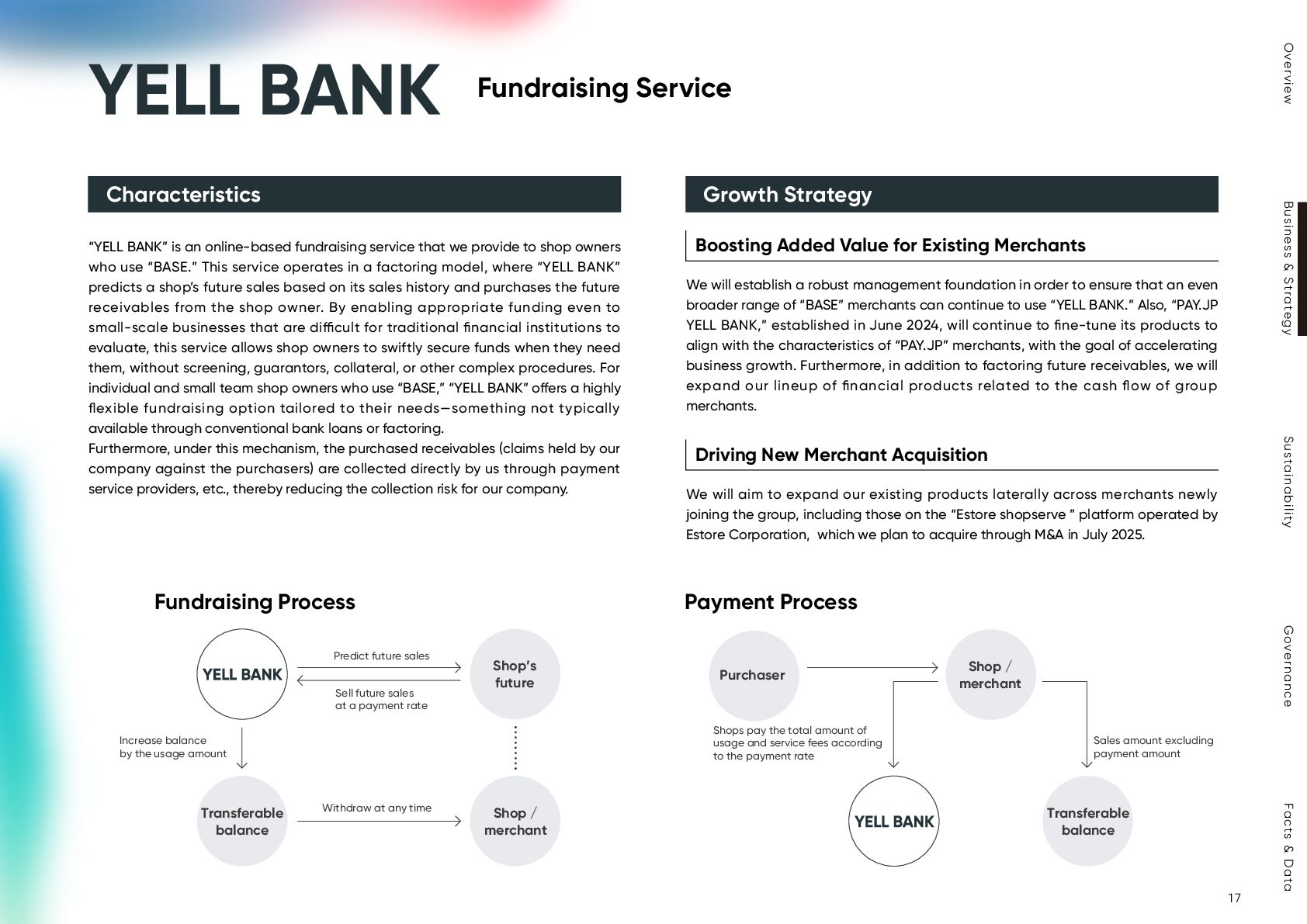

we provide to shop owners who use “BASE.” This service operates in a factoring model, where “YELL BANK” predicts a shop’s future sales based on its sales history and purchases the future receivables from the shop owner. By enabling appropriate funding even to small-scale businesses that are di cult for traditional financial institutions to evaluate, this service allows shop owners to swiftly secure funds when they need them, without screening, guarantors, collateral, or other complex procedures. For individual and small team shop owners who use “BASE,” “YELL BANK” o ers a highly flexible fundraising option tailored to their needs—something not typically available through conventional bank loans or factoring. Furthermore, under this mechanism, the purchased receivables (claims held by our company against the purchasers) are collected directly by us through payment service providers, etc., thereby reducing the collection risk for our company. Boosting Added Value for Existing Merchants We will establish a robust management foundation in order to ensure that an even broader range of “BASE” merchants can continue to use “YELL BANK.” Also, “PAY.JP YELL BANK,” established in June 2024, will continue to fine-tune its products to align with the characteristics of “PAY.JP” merchants, with the goal of accelerating business growth. Furthermore, in addition to factoring future receivables, we will expand our lineup of financial products related to the cash flow of group merchants. Driving New Merchant Acquisition We will aim to expand our existing products laterally across merchants newly joining the group, including those on the “Estore shopserve ” platform operated by Estore Corporation, which we plan to acquire through M&A in July 2025. Characteristics Growth Strategy Fundraising Process Payment Process Predict future sales Withdraw at any time Transferable balance Transferable balance Shop / merchant Shop’s future Purchaser Increase balance by the usage amount Sales amount excluding payment amount Shops pay the total amount of usage and service fees according to the payment rate Sell future sales at a payment rate Shop / merchant 17 Business & Strategy Governance Sustainability Facts & Data Overview

service provides users with a smartphone shopping app that allows them to browse and purchase products from shops on the “BASE” platform. Users can follow their favorite shops to receive push notifications with the latest updates on new product launches, coupons, and more. They can also view their order history, track shipments, and contact shops for a seamless shopping experience. ID Payment Using the ID payment feature, purchasers only need to register their address and credit card information with “Pay ID” once. After that, they can enjoy a seamless checkout experience at any shop on the “BASE” platform simply by logging in with their email address and password. BNPL “Post Pay (Pay ID)” “Post Pay (Pay ID)” is a payment method that allows purchasers to pay after receiving their order. Payment can be made in a single installment in the following month or in three interest-free installments. This service allows purchasers to enjoy shopping even without cash on hand, and shops can boost their sales opportunities without the risk of uncollected payments. We will implement initiatives to monetize purchaser assets held within “Pay ID” and enhance the e ciency of the cost structure, thereby contributing to improved profitability for the BASE business. Furthermore, by introducing the BNPL “Post Pay (Pay ID)” to platforms beyond “BASE,” such as for purchasers who checkout at PAY.JP merchants, we will strengthen the group’s two-sided network across both merchants and purchasers. want.jp is a cross-border e-commerce service that supports Japanese online businesses in selling their products on overseas marketplaces, primarily in Asia. It streamlines many of the complex tasks businesses often face in overseas sales, including pricing, logistics, and inventory management, by handling them on behalf of businesses, thereby supporting their e cient overseas expansion. Its most notable features include a pricing function that automatically optimizes cost calculation for each product by country and marketplace, and a logistics optimization function that automatically selects the most appropriate shipping carrier, depending on the destination. These features ensure both strong price competitiveness and high shipping e ciency in overseas sales. Furthermore, the service is automated to handle each country’s language, currency, and shipping conditions, making cross-border sales as easy and simple as domestic e-commerce. Existing Businesses We will focus e orts on securing stable sales on high-impact overseas marketplaces, aiming to swiftly rebuild and strengthen existing businesses by expanding sales channels, reviewing pricing strategies, and broadening the product lineup. Collaboration with “BASE” By creating an environment where shops on the “BASE” platform can easily venture into overseas sales, we will aim to o er new growth opportunities to individuals and small teams that have traditionally faced high barriers to entering the cross-border e-commerce field. Characteristics Growth Strategy Characteristics Growth Strategy 18 Business & Strategy Governance Sustainability Facts & Data Overview

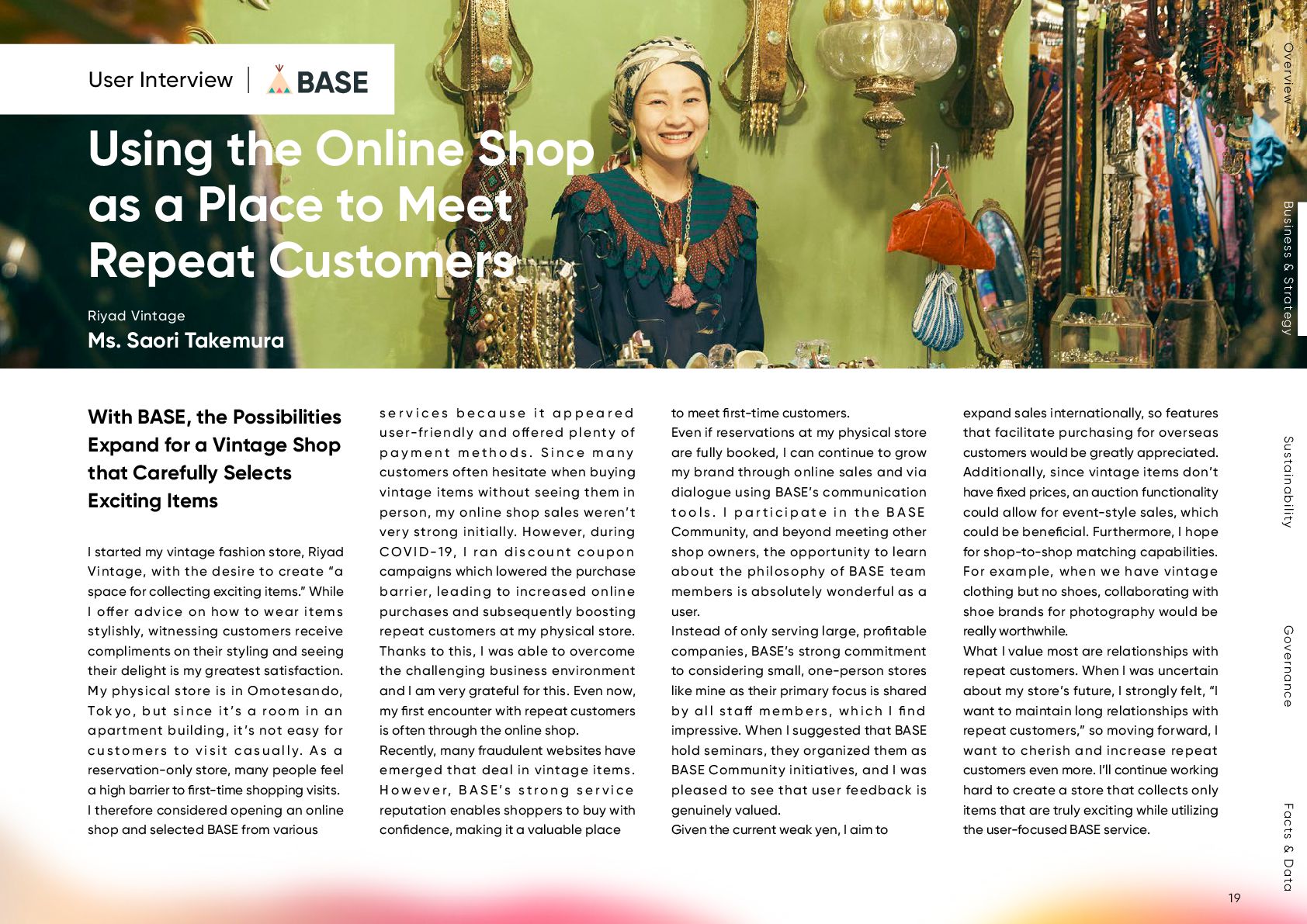

Customers I started my vintage fashion store, Riyad Vintage, with the desire to create “a space for collecting exciting items.” While I o er advice on how to wear items stylishly, witnessing customers receive compliments on their styling and seeing their delight is my greatest satisfaction. My physical store is in Omotesando, Tok yo, but since it ’s a room in an apartment building, it’s not easy for c u s to m e r s to v i s it c a s u a l l y. A s a reservation-only store, many people feel a high barrier to first-time shopping visits. I therefore considered opening an online shop and selected BASE from various User Interview s e r v i c e s b e c a u s e i t a p p e a r e d user-friendly and o ered plenty of p a y m e n t m e t h o d s . S i n c e m a n y customers often hesitate when buying vintage items without seeing them in person, my online shop sales weren’t very strong initially. However, during COVI D -19, I ra n d isco u nt co u p o n campaigns which lowered the purchase barrier, leading to increased online purchases and subsequently boosting repeat customers at my physical store. Thanks to this, I was able to overcome the challenging business environment and I am very grateful for this. Even now, my first encounter with repeat customers is often through the online shop. Recently, many fraudulent websites have emerged that deal in vintage items. H o w e v e r, B A S E ’s s t r o n g s e r v i c e reputation enables shoppers to buy with confidence, making it a valuable place to meet first-time customers. Even if reservations at my physical store are fully booked, I can continue to grow my brand through online sales and via dialogue using BASE’s communication t o o l s . I p a r t i c i p a t e i n t h e B A S E Community, and beyond meeting other shop owners, the opportunity to learn about the philosophy of BASE team members is absolutely wonderful as a user. Instead of only serving large, profitable companies, BASE’s strong commitment to considering small, one-person stores like mine as their primary focus is shared by all sta m em bers, which I find impressive. When I suggested that BASE hold seminars, they organized them as BASE Community initiatives, and I was pleased to see that user feedback is genuinely valued. Given the current weak yen, I aim to expand sales internationally, so features that facilitate purchasing for overseas customers would be greatly appreciated. Additionally, since vintage items don’t have fixed prices, an auction functionality could allow for event-style sales, which could be beneficial. Furthermore, I hope for shop-to-shop matching capabilities. For example, when we have vintage clothing but no shoes, collaborating with shoe brands for photography would be really worthwhile. What I value most are relationships with repeat customers. When I was uncertain about my store’s future, I strongly felt, “I want to maintain long relationships with repeat customers,” so moving forward, I want to cherish and increase repeat customers even more. I’ll continue working hard to create a store that collects only items that are truly exciting while utilizing the user-focused BASE service. With BASE, the Possibilities Expand for a Vintage Shop that Carefully Selects Exciting Items Riyad Vintage Ms. Saori Takemura 19 Business & Strategy Governance Sustainability Facts & Data Overview

matters most,” providing housekeeping and house cleaning services for households. When we founded the company in 2014, both our Representative Director and COO, Hiroki Ikeda, and I actually used housekeeping services and found that everyone in our households was smiling more, especially compared to when we were chore-sharing, which strained relationships. When we considered why such a good service wasn’t spreading, we realized that the issues were high prices and the hassle incurred before use. Under the mission of controlling both price and hassle through a Payment Services that Lead to Business Expansion housekeeping service × sharing economy mechanism, we decided to provide services for those wanting a little more time. However, when we received the same voice from many users, “When I was busy and about to give up, CaSy helped me think I could work a little harder”, we recognized CaSy could become lifestyle infrastructure beyond just housekeeping, which inspired our current mission. Going forward, by developing various services that provide “free time” through more than just h o u s e ke e p i n g , we a i m to c re a te emotional space and free time, allowing people worldwide to dedicate time to altruistic actions. Our target figure, based on the world population, is 9 billion hours by 2050. Thus, we aim to expand the platform not just in Japan, but also overseas. We chose PAY.JP as CaSy’s payment service for two reasons. The first is the cost advantage in payment fees. R e d u c i n g f e e c o s t s a l l o w e d f o r significant investment in end users and our cast (workers). The second reason involves administrative aspects. While we originally used another service, we struggled significantly with the migration process. PAY.JP is cooperative during data migration to other companies, giving us the impression that they have confidence in their product. And we continue to use PAY.JP because of the cost benefits and payment transfer timing it provides. Since we added instant payment functionality for cast compensation, PAY.JP’s transfers, which take place twice a month at 15-day intervals, help optimize working c a p i t a l a n d a s s i s t c o m p a n y management. Going forward, we plan to expand our services to include house cleaning, organization and storage, partnerships with government entities, support for housekeeping businesses, and services for the elderly. Our goal is to create a platform where people can request helper services similar to shopping on Amazon. We hope PAY.JP will introduce payment methods beyond credit cards a n d b ro a d e n its i m p l e m e ntati o n conditions. Since “providing a sense of security for workers” is also part of our foc us, we a im to eve ntually o e r financial guarantees, including lending options, to our cast, and this includes corporations too. BASE was founded around the same time as us, and many of its employees use CaSy; therefore, we want to encourage each other to create services that can firmly establish a presence in the world. Delivering Diverse Businesses Worldwide that Create Free Time User Interview CaSy Co., Ltd. Representative Director, CEO & CFO Mr. Yuichi Kamo 20 Business & Strategy Governance Sustainability Facts & Data Overview

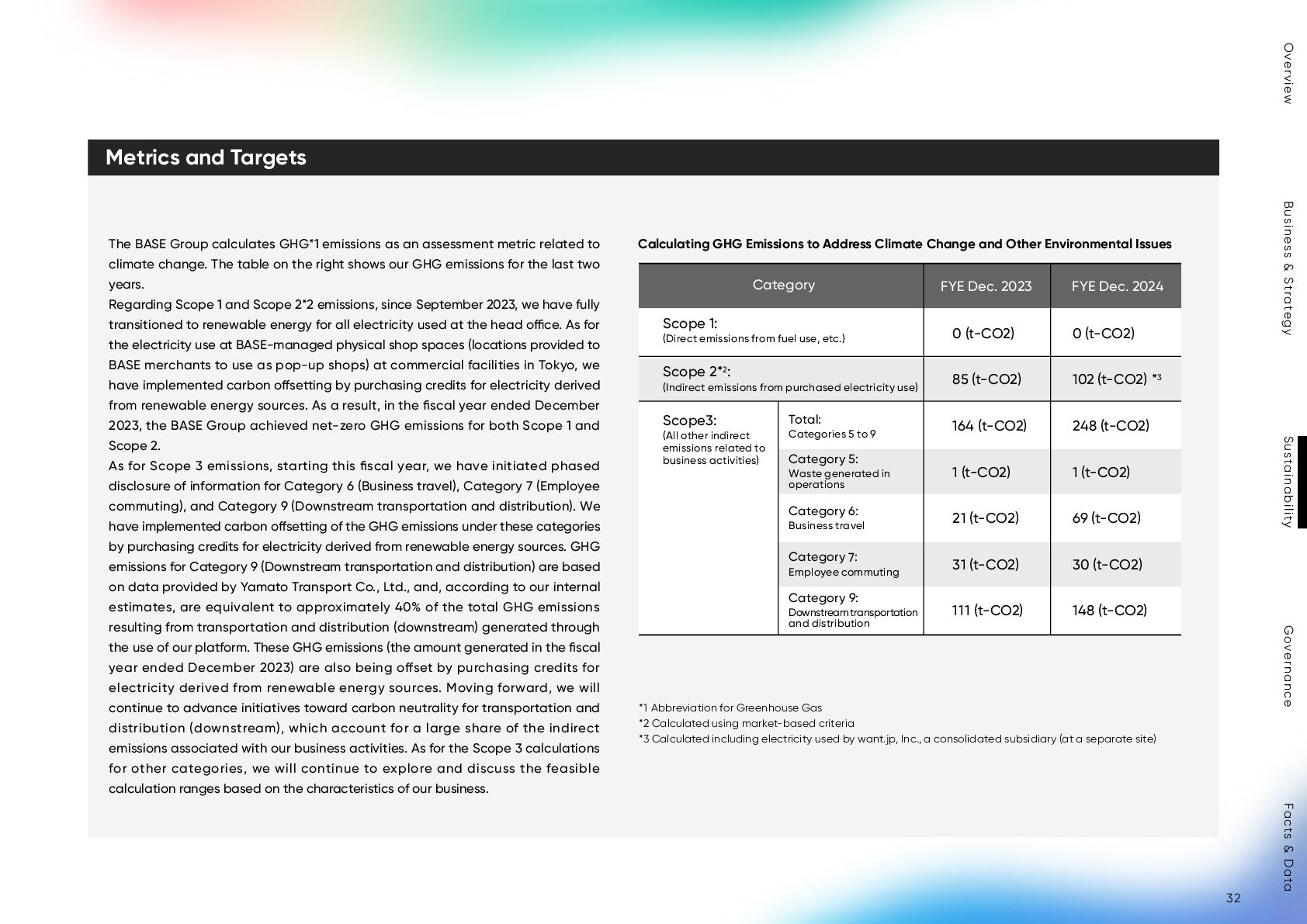

the People, Power to the People.” Our goal is to leverage internet technology to enhance accessibility to payment and financial services, which many people need but have not yet been able to benefit from, thereby empowering individuals and small teams, and realizing a society where everyone can thrive. Since our inception, we have believed more than anyone else that “when the internet empowers individuals and small teams, the world becomes a much better place.” This belief has guided our product planning and development and will continue to do so. We aim to realize this mission as soon as possible, acting as a responsible platform provider of open payment and financial services and promoting ESG initiatives throughout the group to achieve a sustainable society. As a platform provider of payment and financial services, our company views the occurrence of large-scale disasters as a grave risk to business continuity. To ensure prompt recovery while securing the safety of our employees and their families and minimizing the impact on business activities as our top priority tasks, we identify potential risks in advance and take various measures to prevent and mitigate them. In June 2023, the BASE Group formulated Business Continuity Plan (BCP) regulations, established a crisis management structure led by the CEO, introduced a safety confirmation system, and created various manuals (including a Disaster Prevention and Preparedness Manual and a Critical Business Recovery Plan). Through these e orts, we now have the capability to implement swift initial response in emergency situations and secure the continuity, early recovery, and normalization of business operations. Also, we formulate an annual BCP activity plan through the department overseeing BCP, and conduct regular safety confirmation and firefighting drills during normal operations in anticipation of potential emergencies. Through such drills, we confirm that departmental role assignments and communication systems function correctly and smoothly in emergency situations, and implement revisions as necessary. The results of these initiatives are reported at the quarterly meeting of the Risk Management and Compliance Committee, which establishes mechanisms to discuss necessary response policies and to monitor the status of those responses. Going forward, we will continue to implement a PDCA cycle based on the BCP regulations and will reinforce risk management. Moving forward, a department responsible for sustainability will identify and evaluate climate change-related risks and opportunities with the cooperation of relevant departments and report them to the Sustainability Committee along with recommendations, promoting a company-wide response to climate change. Critical environment risks and social challenges related to climate change issues raised in the Sustainability Committee will be integrated into company-wide risk management in collaboration with the Risk Management and Compliance Committee. Basic Sustainability Policy Business Continuity Plan (BCP) Initiatives Risks Associated with Sustainability In March 2022, the BASE Group established a Sustainability Committee to discuss, coordinate, and monitor significant sustainability-related matters, including our basic policy, materiality, and related initiatives. The committee also reviews and considers important issues to be presented to management meetings. Matters that have passed through the Sustainability Committee and have been deliberated and decided upon by management meetings are regularly reported to the Board of Directors along with progress status updates. The response policies and measures agreed upon at management meetings are spearheaded by the CEO, who chairs the Sustainability Committee, and implemented by each department within the company. 22 Business & Strategy Governance Sustainability Facts & Data Overview

we aim to create systems and workplace environments that allow each individual’s personality and abilities to be fully realized. This involves promoting work-life balance and cultivating a DE&I environment to enhance employee engagement. The BASE Group sees human resources as the most crucial management resource for achieving sustainable growth and enhancing business value. Therefore, supporting employees in taking ownership of their work and careers and continuously challenging themselves is essential for their development. The BASE Group defines nine areas of skills common to all job types, and promotes educational and training measures tailored to each grade, position, and career path in accordance with a set priority order. Through these measures, we will foster employees’ professional growth and thereby aim to enhance the overall competitiveness of the organization. Human Resource Development In order to provide a hybrid working model for our employees, we continue to operate a flex-time system and a work-from-home scheme. Also, we have achieved a 100% usage rate of five or more days of paid leave and an average monthly overtime of less than 10 hours. We have also introduced and regularly test-run support systems tailored to each employee’s life stage. In FY2024, we achieved 100% usage of parental leave among women and over 80% among men, and a 100% return to work rate for both men and women. Going forward, we will provide a framework that enables our diverse employees to work productively, and will ensure an environment where all talent can thrive. Work-Life Balance DE&I As a company striving to create a society where all individuals can succeed, we have established a human rights policy of zero tolerance for discrimination or harassment based on gender, gender identity or sexual orientation, disability, nationality, or any other personal di erences. In line with this policy, we conduct DE&I training, update internal systems, support the Ally Community activities of volunteer employees, and promote a workplace environment where members with diverse backgrounds can work comfortably. We implement measures tailored to the needs of women in the workplace to create an environment where they can thrive. By broadening the diversity of our talent in terms of gender, nationality, disability, etc., and leveraging the various perspectives this diversity brings, we aim to drive business growth. We have set the following goals to be achieved by 2030: 30% or more Ratio of female o cers: 30% or more Ratio of female managers: Internal Environment Development Policy Human Resource Development Policy Individual Themes 23 Business & Strategy Governance Sustainability Facts & Data Overview

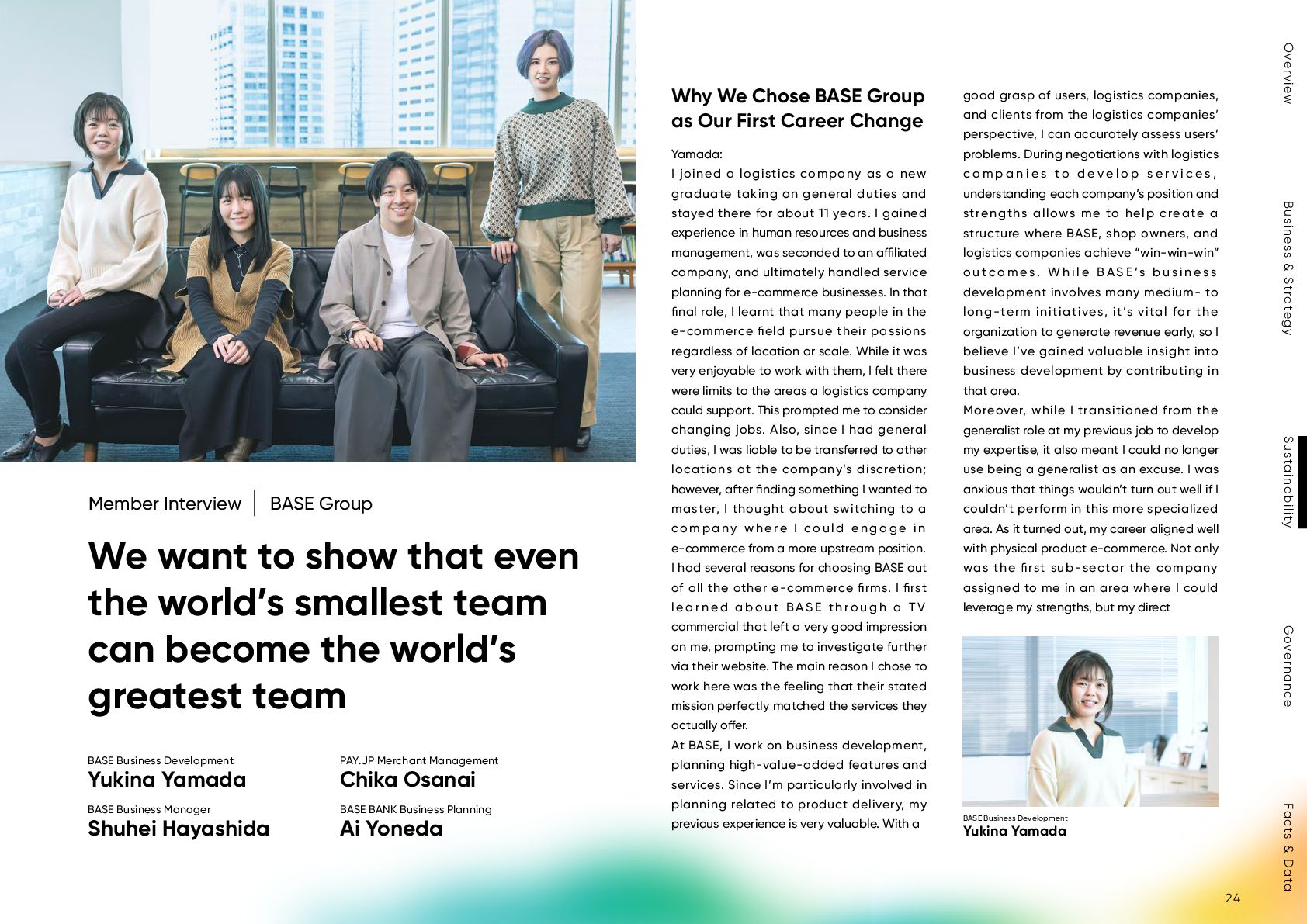

taking on general duties and stayed there for about 11 years. I gained experience in human resources and business management, was seconded to an a liated company, and ultimately handled service planning for e-commerce businesses. In that final role, I learnt that many people in the e-commerce field pursue their passions regardless of location or scale. While it was very enjoyable to work with them, I felt there were limits to the areas a logistics company could support. This prompted me to consider changing jobs. Also, since I had general duties, I was liable to be transferred to other locations at the company’s discretion; however, after finding something I wanted to master, I thought about switching to a c o m p a n y w h e re I c o u l d e n g a g e i n e-commerce from a more upstream position. I had several reasons for choosing BASE out of all the other e-commerce firms. I first l e a r n e d a b o u t B A S E t h ro u g h a T V commercial that left a very good impression on me, prompting me to investigate further via their website. The main reason I chose to work here was the feeling that their stated mission perfectly matched the services they actually o er. At BASE, I work on business development, planning high-value-added features and services. Since I’m particularly involved in planning related to product delivery, my previous experience is very valuable. With a good grasp of users, logistics companies, and clients from the logistics companies’ perspective, I can accurately assess users’ problems. During negotiations with logistics c o m p a n i e s t o d e v e l o p s e r v i c e s , understanding each company’s position and strengths allows me to help create a structure where BASE, shop owners, and logistics companies achieve “win-win-win” o u t c o m e s . W h i l e B A S E ’s b u s i n e s s development involves many medium- to long-term initiatives, it’s vital for the organization to generate revenue early, so I believe I’ve gained valuable insight into business development by contributing in that area. Moreover, while I transitioned from the generalist role at my previous job to develop my expertise, it also meant I could no longer use being a generalist as an excuse. I was anxious that things wouldn’t turn out well if I couldn’t perform in this more specialized area. As it turned out, my career aligned well with physical product e-commerce. Not only was the first sub-sector the company assigned to me in an area where I could leverage my strengths, but my direct Why We Chose BASE Group as Our First Career Change BASE Business Manager Shuhei Hayashida BASE BANK Business Planning Ai Yoneda BASE Business Development Yukina Yamada PAY.JP Merchant Management Chika Osanai Member Interview BASE Group We want to show that even the world’s smallest team can become the world’s greatest team BASE Business Development Yukina Yamada 24 Business & Strategy Governance Sustainability Facts & Data Overview

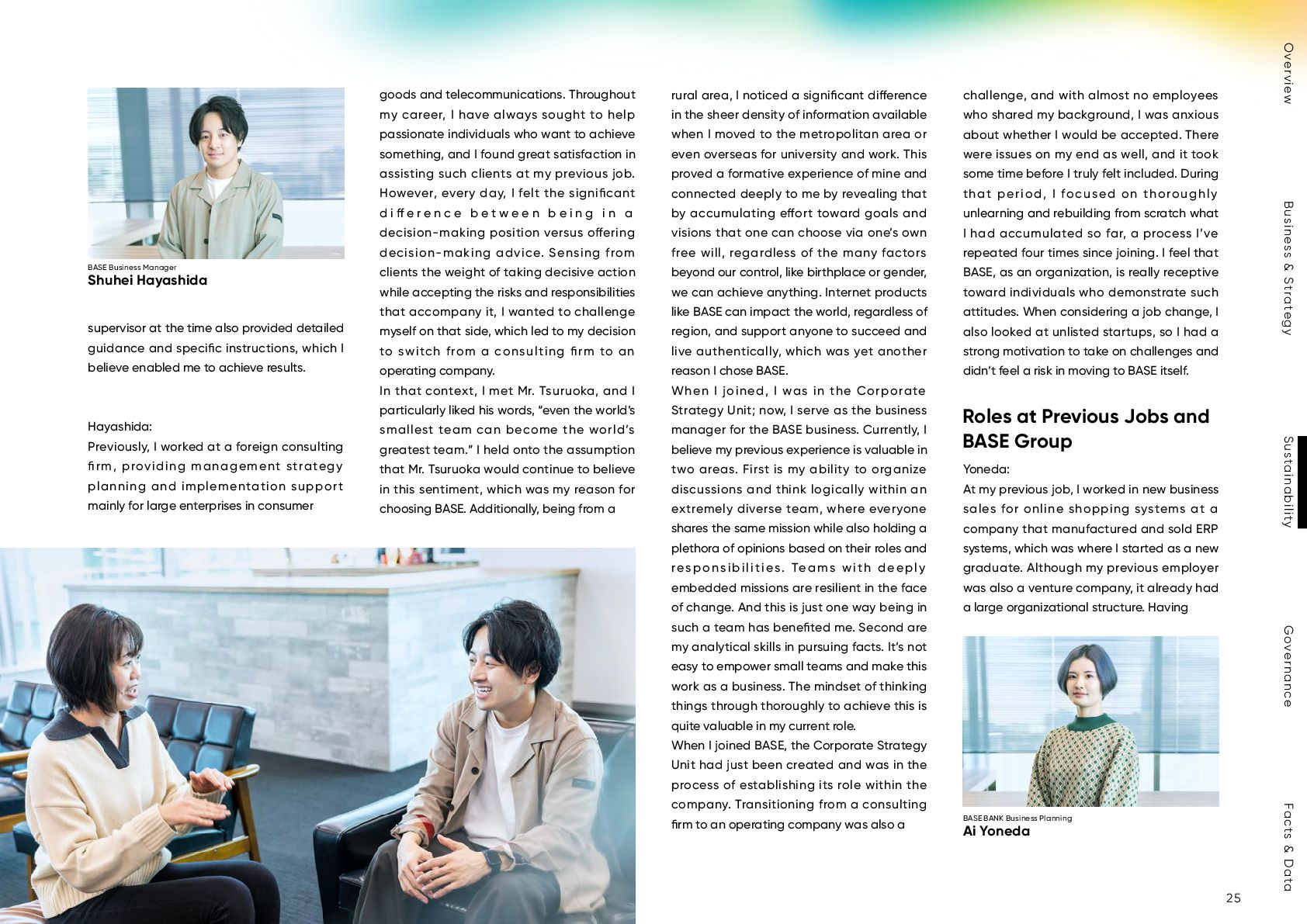

instructions, which I believe enabled me to achieve results. Hayashida: Previously, I worked at a foreign consulting firm, providing management strategy planning and implementation support mainly for large enterprises in consumer goods and telecommunications. Throughout my career, I have always sought to help passionate individuals who want to achieve something, and I found great satisfaction in assisting such clients at my previous job. However, every day, I felt the significant d i e r e n c e b e t w e e n b e i n g i n a decision-making position versus o ering decision-making advice. Sensing from clients the weight of taking decisive action while accepting the risks and responsibilities that accompany it, I wanted to challenge myself on that side, which led to my decision to switch from a consulting firm to an operating company. In that context, I met Mr. Tsuruoka, and I particularly liked his words, “even the world’s smallest team can become the world’s greatest team.” I held onto the assumption that Mr. Tsuruoka would continue to believe in this sentiment, which was my reason for choosing BASE. Additionally, being from a rural area, I noticed a significant di erence in the sheer density of information available when I moved to the metropolitan area or even overseas for university and work. This proved a formative experience of mine and connected deeply to me by revealing that by accumulating e ort toward goals and visions that one can choose via one’s own free will, regardless of the many factors beyond our control, like birthplace or gender, we can achieve anything. Internet products like BASE can impact the world, regardless of region, and support anyone to succeed and live authentically, which was yet another reason I chose BASE. When I joined, I was in the Corporate Strategy Unit; now, I serve as the business manager for the BASE business. Currently, I believe my previous experience is valuable in two areas. First is my ability to organize discussions and think logically within an extremely diverse team, where everyone shares the same mission while also holding a plethora of opinions based on their roles and responsibilities. Teams with deeply embedded missions are resilient in the face of change. And this is just one way being in such a team has benefited me. Second are my analytical skills in pursuing facts. It’s not easy to empower small teams and make this work as a business. The mindset of thinking things through thoroughly to achieve this is quite valuable in my current role. When I joined BASE, the Corporate Strategy Unit had just been created and was in the process of establishing its role within the company. Transitioning from a consulting firm to an operating company was also a challenge, and with almost no employees who shared my background, I was anxious about whether I would be accepted. There were issues on my end as well, and it took some time before I truly felt included. During that period, I focused on thoroughly unlearning and rebuilding from scratch what I had accumulated so far, a process I’ve repeated four times since joining. I feel that BASE, as an organization, is really receptive toward individuals who demonstrate such attitudes. When considering a job change, I also looked at unlisted startups, so I had a strong motivation to take on challenges and didn’t feel a risk in moving to BASE itself. Yoneda: At my previous job, I worked in new business sales for online shopping systems at a company that manufactured and sold ERP systems, which was where I started as a new graduate. Although my previous employer was also a venture company, it already had a large organizational structure. Having Roles at Previous Jobs and BASE Group BASE Business Manager Shuhei Hayashida BASE BANK Business Planning Ai Yoneda 25 Business & Strategy Governance Sustainability Facts & Data Overview

work in a smaller company again, which is why I changed the job. I initially applied for a customer success position at BASE where I could leverage my sales experience, but Mr. Yamamura (current executive o cer), who interviewed me, proposed a human resources position. Although I had no HR or recruiting experience, I believed I could leverage my communication skills developed t h r o u g h s a l e s a n d m y w e b m e d i a management experience from my internship days to recruitment PR, so I decided to join BASE. I also felt that startup recruitment had a significant impact on company growth. I think it’s relatively unusual for young startups seeking industry-ready talent to hire someone with little experience, but with my startup experience, I think they weren’t worried about cultural fit. After joining and engaging in recruitment work, I developed a desire to master this field and aim to become the CHRO. When I joined BASE, there were no experienced recruitment PR sta in the company, and we didn’t yet have the solid recruitment organization of large companies, so I was initially overwhelmed just handling immediate tasks. However, when I said, “I want to try this,” I was never flatly refused; they supported me in figuring out how to make it happen. Osanai: I previously worked at a funeral company, h a n d l i n g e v e r y t h i n g f r o m f u n e r a l arrangements to follow-ups for memorial services. That role involved flexibly responding to sudden events while honoring the family’s wishes. Before that, I had done back-o ce work, such as HR, at a venture company. However, when I had learned about the funeral industry, I had been drawn to the opportunity to support bereaved families immediately after their loss and to help conduct ceremonies smoothly. Seeing peers active in the field had motivated me to transfer to the funeral company, despite it being a completely di erent industry. While I had found fulfillment, I began to feel a disconnect with my career goals in an industry steeped in old traditions. I wanted to be in an environment where both the company and I could grow together, which led me to decide to transfer to PAY. In addition to customer-focused, flexible responses, I focused on smooth internal communication in an environment where mistakes weren’t tolerated, which I believe was appreciated when I transferred to PAY. At PAY, I handle merchant management, supporting merchants so they can continue using our services with confidence. I also handle behind-the-scenes design and troubleshooting when we launch new services or make system modifications. As it was a job change during the COVID-19 pandemic and I started to work remotely, I initially struggled to adjust to text-based communication. However, since this was a common team challenge, we all worked together on “paying it forward”—giving back what we had received to benefit others, to create a positive atmosphere. And as a result, my communication anxieties disappeared. Yoneda: I’ve made two job changes within the company. I started in recruitment, then moved to the Corporate Strategy Unit, and now I handle business planning for YELL BANK. I was inexperienced when I joined BASE, and I didn’t yet have experience in any of the roles I’ve since been allowed to take on. If I had been transferring to another company, it would have been di cult to secure an o er without experience, but I think BASE recognized my attitude and track record so far. As the company grows and business diversifies, everyone faces new challenges, but I believe I was given these opportunities because I’ve been able to do my best in each situation and produce tangible results. Among these, establishing the field-driven recruitment style that is now our company’s approach was a key area where I could contribute significantly. I rethought BASE’s recruitment systems from scratch and was able to create and promote a culture where immediate managers and team members take the initiative in recruiting. I’m proud that this practice continues even though I’m no longer in charge of recruitment. For me, career advancement means aiming for What We Gained Through Job Changes, Transfers, and Leave PAY.JP Merchant Management Chika Osanai 26 Business & Strategy Governance Sustainability Facts & Data Overview

I’m gaining the necessary experience for my target career through various roles. Not only essential for career progression—being able to think “this looks fun” is very important to me in choosing roles, and I was fortunate to have such opportunities within the company. However, not everything has been smooth sa i l i n g . T h e re we re t i m es w h e n my performance reviews seemed wanting, and I painfully realized I lacked a management perspective. Especially after I moved to the Corporate Strategy Unit, I struggled to meet the high level of output that management required. Additionally, with my goal of becoming CHRO in the future, I thought I wouldn’t be able to make HR work properly without a solid understanding and knowledge of our business. As I remained concerned with my lack of business experience, I once considered changing a company. At that time, YELL BANK business manager Mr. Yanagawa gave me the opportunity to handle business planning while the business was experiencing tremendous growth. Although I faced challenges that I couldn’t o v e r c o m e, c o n f r o n t i n g t h e m w i t h determination and focusing on how to improve and take action has shaped who I am today. Osanai: At PAY, I have a flexible environment and growth opportunities. I once fell ill and took leave, but work became truly enjoyable after I returned. Previously, we were a very small team handling various duties, but around the time I returned, as the business expanded, the organization grew slightly, and responsibilities became more divided among the teams. At that time, I also clarified what I wanted to do; when I communicated this to my supervisor, I was grateful to be assigned to the perfect department. My previous duties were focused on “continuing immediate tasks without incident.” However, in my current role, I can e ectively engage in activities beyond those immediate tasks. I have more chances to say, “I want to do this and try that,” and with help from other departments, I can connect these to business improvements. While the PAY.JP business is growing significantly, I can contribute to establishing operational systems while being encouraged to actively try things I couldn’t do before, and I really feel a sense of personal growth as a result. In addition to my daily duties, I am responsible for a large annual survey. I’m gradually improving it each year while ensuring it’s e ectively completed without causing any issues for merchants. To be honest, I really believe I’m supporting the foundation of our business operations. Back-o ce work revolves around avoiding mistakes, but it’s challenging to actually gain recognition for the act of not making an error. Although it is clear that mistakes can lead to significant trouble for both customers and the company; maintaining motivation in this context can be somewhat di cult. However, at PAY, they appropriately recognize accident-free task execution, and I am also grateful that I can feel a strong sense of place here as management policies are e ectively shared to all levels amidst incredibly rapid growth. Osanai: PAY.JP currently has fewer features than its competitors if we take a simple comparison, so I feel there’s still much room for growth. Since new feature development and initiatives are proceeding at an incredible speed, I want to create strong back-o ce operations that can keep up with this business growth. It should become a service chosen by companies and payment sta across a broader, more diverse range of industries, so the thought of being able to see that process up close really gets me excited. Additionally, I love the atmosphere within the PAY team, especially our culture of praising one another, and I don’t want that to change. Yoneda: The YELL BANK business encompasses multiple products, and I’m eager to enhance the value of this business division by continuously introducing new o erings. Generally, launching financial services from the ground up involves significant challenges, but BASE Group has already established foundations in the BASE and PAY.JP businesses, enabling the financial business to create various new value propositions for them. I believe we’re fortunate to focus on diverse challenges and enhance Group-wide profitability. By leveraging this position, we’re diligently working to surpass existing businesses in terms of growth while maintaining a healthy rivalry. Hayashida: BASE will continue to be a team that contributes to society by believing that “when individuals and small teams are empowered, the world becomes a better place” and by evolving as a platform that maximizes the potential of individuals and small teams. In an era of uncertain changes like technological trends and social conditions, I believe that having an established presence—one where all sorts of people know that “apparently there’s a service called ‘BASE’ that’s creating a big impact through its individual and small team empowerment”—is what will lead to value contribution to society. To achieve this, while we continue to pursue our mission, we’ll also fo c u s o n b u s i n ess g row t h to m e e t expectations. We’ll keep creating solid user value. With support from users, we’ll see profits rise. People who share our mission will join the team, enabling us to create greater value. This cycle is simple yet extremely challenging, and I want to tackle it head-on. By doing so, I want us to prove to ourselves that “even the world’s smallest team can become the world’s greatest team.” BASE Group from the Perspective of PAY.JP and YELL BANK Career Plans and Aspirational Goals 27 Business & Strategy Governance Sustainability Facts & Data Overview

sustain team output, under the shared understanding that working hours are equal for everyone, and this policy ultimately allows members to have flexible working styles. Hayakawa: Children’s sudden circumstances of ten necessitate changes to schedules, and I’m truly grateful they accommodate this so readily. The flexibility in work hours and location allows me to maintain a work-family balance. Samata: While our lifestyles vary, I believe the team has built trusting relationships that enable exchanges of opinion frankly. Being able to support one another with necessary skills while respecting each other’s circumstances is reassuring. Tanaka: I’m looking forward to our members on childcare leave returning to work. Going forward, I want the whole team to continue supporting each other’s circumstances while aiming for maximum results. Tanaka: The PR Division handles both corporate and business PR, sharing responsibilities. Currently, we have a team of five: four regular employees and one contractor. Ms. Samata and I work full-time, while Ms. Misawa and Ms. Kimura are on childcare leave, and Ms. Hayakawa works half the week (2.5 days). Samata: I joined BASE in November last year, and including members who are raising children, I feel it’s great that we can work in a flexible and reasonable way. The manager flexibly adjusts work allocation. Hayakawa: When I started working at BASE, my husband was on a solo assignment, which left me in a situation of working while single-handedly raising two children. Because of this, I chose contract work to better balance my family responsibilities. At BASE, even as a contractor, I don’t feel any barriers with full-time members and I felt that I was working in trusting relationships. Information is thoroughly shared in manager 1 on 1s and regular team meetings, allowing me to focus on work without anxiety. Tanaka: Regardless of each person’s employment type, s i n c e o u r m e m b e rs c a n t h i n k a n d a c t autonomously to produce results, I can trust them and delegate tasks, fostering an environment where we can work flexibly with a focus on output. Also, when it comes to our working styles, we are not overly considerate of each individual’s personal circumstances, as everyone has di erent lives and lifestyles. What is common between us all, however, is our working hours. Since each person knows best how to use their own time e ciently to be as productive as they can be during their working hours, we should avoid delays as a team or backing down from challenges simply in favor of pandering to each person’s individual circumstances. I have informed PR team culture of autonomy and trust supporting diverse working styles Member Interview PR Division This was my first time taking childcare leave, and I could prepare and give birth with peace of mind thanks to the company’s systems and attentive labor relations support. Despite being a small team, they gave me a warm send o , and when I return, I want to continue my career while utilizing company systems. Supported by flexible work arrangements, a remote environment, and thoughtful responses from my team and the business divisions I handle PR for, I’m really excited to come back. On childcare leave: Ayano Kimura Wanting to stay involved in work even during childcare leave, I’m utilizing the semi-childcare leave system to work reduced hours. Supported by the company’s flexible systems, remote environment, and team cooperation, I can work with peace of mind. The PR team regularly shares information and communicates actively on Slack, making communication straightforward and enabling working styles tailored to individual circumstances, which is what I prefer. On childcare leave: Mari Misawa Yuko Hayakawa Manager Yoko Tanaka Harumi Samata 28 Business & Strategy Governance Sustainability Facts & Data Overview

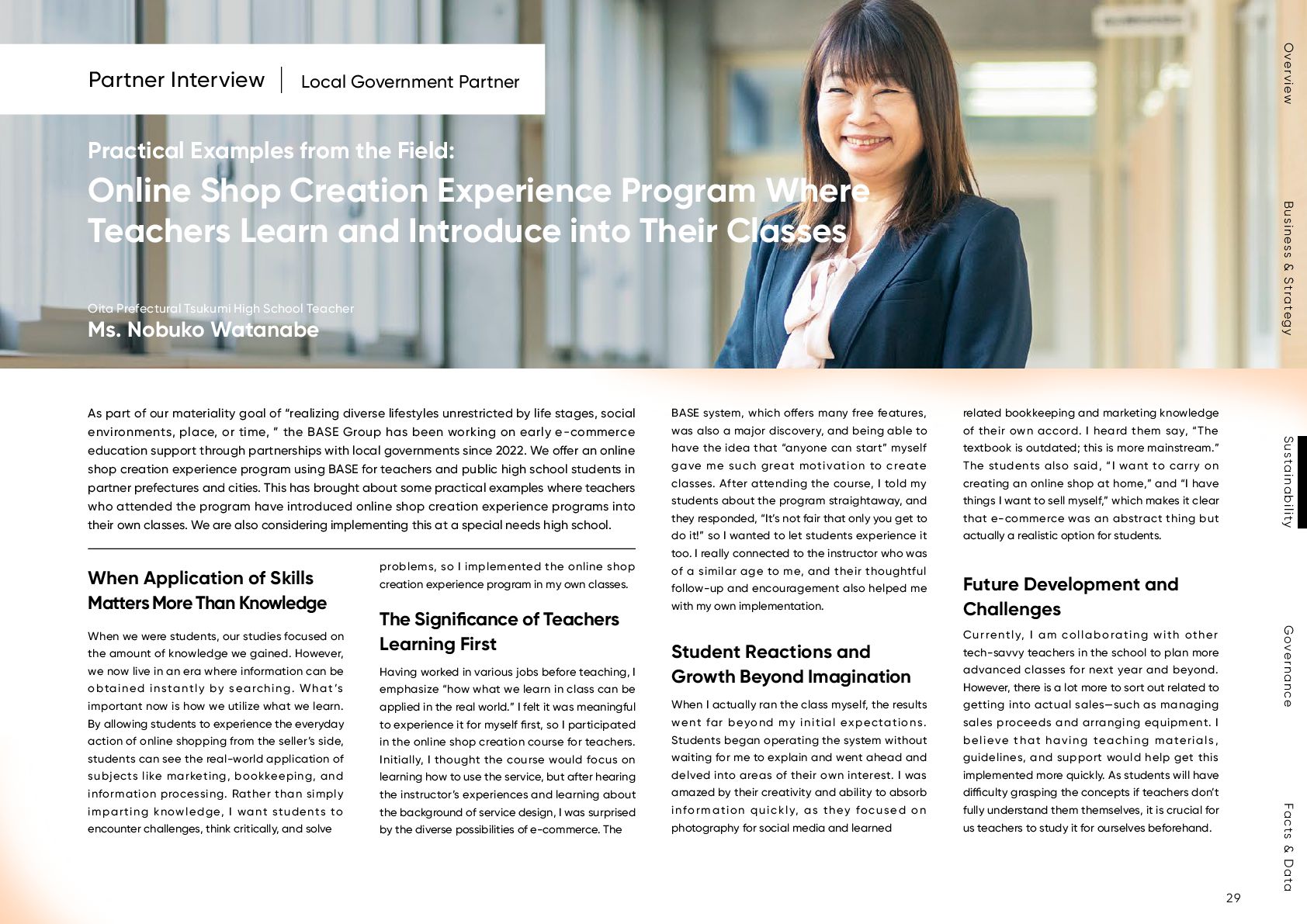

Examples from the Field: Online Shop Creation Experience Program Where Teachers Learn and Introduce into Their Classes When we were students, our studies focused on the amount of knowledge we gained. However, we now live in an era where information can be obtained instantly by searching. What’s important now is how we utilize what we learn. By allowing students to experience the everyday action of online shopping from the seller’s side, students can see the real-world application of subjects like marketing, bookkeeping, and information processing. Rather than simply imparting knowledge, I want students to encounter challenges, think critically, and solve problems, so I implemented the online shop creation experience program in my own classes. Having worked in various jobs before teaching, I emphasize “how what we learn in class can be applied in the real world.” I felt it was meaningful to experience it for myself first, so I participated in the online shop creation course for teachers. Initially, I thought the course would focus on learning how to use the service, but after hearing the instructor’s experiences and learning about the background of service design, I was surprised by the diverse possibilities of e-commerce. The BASE system, which o ers many free features, was also a major discovery, and being able to have the idea that “anyone can start” myself gave me such great motivation to create classes. After attending the course, I told my students about the program straightaway, and they responded, “It’s not fair that only you get to do it!” so I wanted to let students experience it too. I really connected to the instructor who was of a similar age to me, and their thoughtful follow-up and encouragement also helped me with my own implementation. When I actually ran the class myself, the results went far beyond my initial expectations. Students began operating the system without waiting for me to explain and went ahead and delved into areas of their own interest. I was amazed by their creativity and ability to absorb information quickly, as they focused on photography for social media and learned As part of our materiality goal of “realizing diverse lifestyles unrestricted by life stages, social environments, place, or time, ” the BASE Group has been working on early e-commerce education support through partnerships with local governments since 2022. We o er an online shop creation experience program using BASE for teachers and public high school students in partner prefectures and cities. This has brought about some practical examples where teachers who attended the program have introduced online shop creation experience programs into their own classes. We are also considering implementing this at a special needs high school. related bookkeeping and marketing knowledge of their own accord. I heard them say, “The textbook is outdated; this is more mainstream.” The students also said, “I want to carry on creating an online shop at home,” and “I have things I want to sell myself,” which makes it clear that e-commerce was an abstract thing but actually a realistic option for students. Currently, I am collaborating with other tech-savvy teachers in the school to plan more advanced classes for next year and beyond. However, there is a lot more to sort out related to getting into actual sales—such as managing sales proceeds and arranging equipment. I believe that having teaching materials, guidelines, and support would help get this implemented more quickly. As students will have di culty grasping the concepts if teachers don’t fully understand them themselves, it is crucial for us teachers to study it for ourselves beforehand. Partner Interview Local Government Partner When Application of Skills Matters More Than Knowledge Student Reactions and Growth Beyond Imagination Future Development and Challenges The Significance of Teachers Learning First 29 Business & Strategy Governance Sustainability Facts & Data Overview

Sapporo Minami-no-Mori Special Needs High School fosters the ability of students with disabilities to work independently in society. The school emphasizes practical education and features an on-campus café that is open to the public, providing students with experience in customer service and shop operations. In order to explore the possibilities of online shops and see if it is a good fit, I participated in the course alongside the principal at that time. Our school has six specialized courses, including customer service, design, and product management. And there are opportunities to apply the skills from each course in online shop management. For instance, design course students create layouts and product pages, while those in the customer service course write descriptions and social media posts. Studying e-commerce lets the students completely experience the whole business process. The school’s participation in the course was decided after consulting with the principal, influenced by the partnership agreement between the Sapporo City Board of Education and BASE. The BASE system o ers a wide variety of layouts and is user-friendly, and I felt that students would enjoy working on it with teacher support. Our school already uses AI for research and marketing to attract customers to our café. And through engaging in activities such as these in IT and DX, our students can identify their own strengths, weaknesses, and preferences. Here, online shops too can act as a platform for such self-discovery. Our school curriculum lets students line up jobs, with four internships in their second year. The school works with companies to ensure students are able to do the job they wish to try. In the p a s t , i n t e r n s h i p s t y p i c a l l y i n v o l v e d behind-the-scenes tasks; however, students now req uest vari ous j ob p l a ce me n ts. A lso, post-graduation employment has diversified and now includes the aviation industry and gaming centers, and I anticipate that e-commerce knowledge will open up new career choices. Recently, there was a student who dreamed of working at a general goods store, but when we had trouble finding an internship location and consulted with a local business owner, who told us, “If there isn’t one, start your own business!” I also believe we’re entering an era where students will start their own businesses to pursue their dreams. I think now is the time when anyone, regardless of disability, can pursue what they enjoy wherever they like. And I hope it stays this way. As the students are able to engage in online shop management that is connected to career support, they can further expand their own possibilities. Our role is to support the initial step so students can turn what excites them into their work. This is a time when anyone can work in their preferred environment, and e-commerce o ers students great possibilities as an entry point. Our school is continually seeking internship opportunities, and it would be fantastic if, in the future, we could help address the talent shortage at companies that promote IT and DX. To that end, we would appreciate the chance to apply the materials used in the teacher online shop creation course to our classes as well. Should we implement an online shop creation experience program for students, we, as teachers, could rest assured with BASE’s support. We look forward to your future assistance. Partner Interview Local Government Partner Taking the First Steps in e-commerce Practical Education at a Special Needs High School: Students’ Futures Expand Through Online Shop Management Students’ Futures Expand Through Online Shop Management How Practical Education at Special Needs High School and e-commerce Can Work Together A Future Where Students Create Their Own Ways of Working Online Shops Where Students’ “Strengths” Can Be Utilized 30 Business & Strategy Governance Sustainability Facts & Data Overview