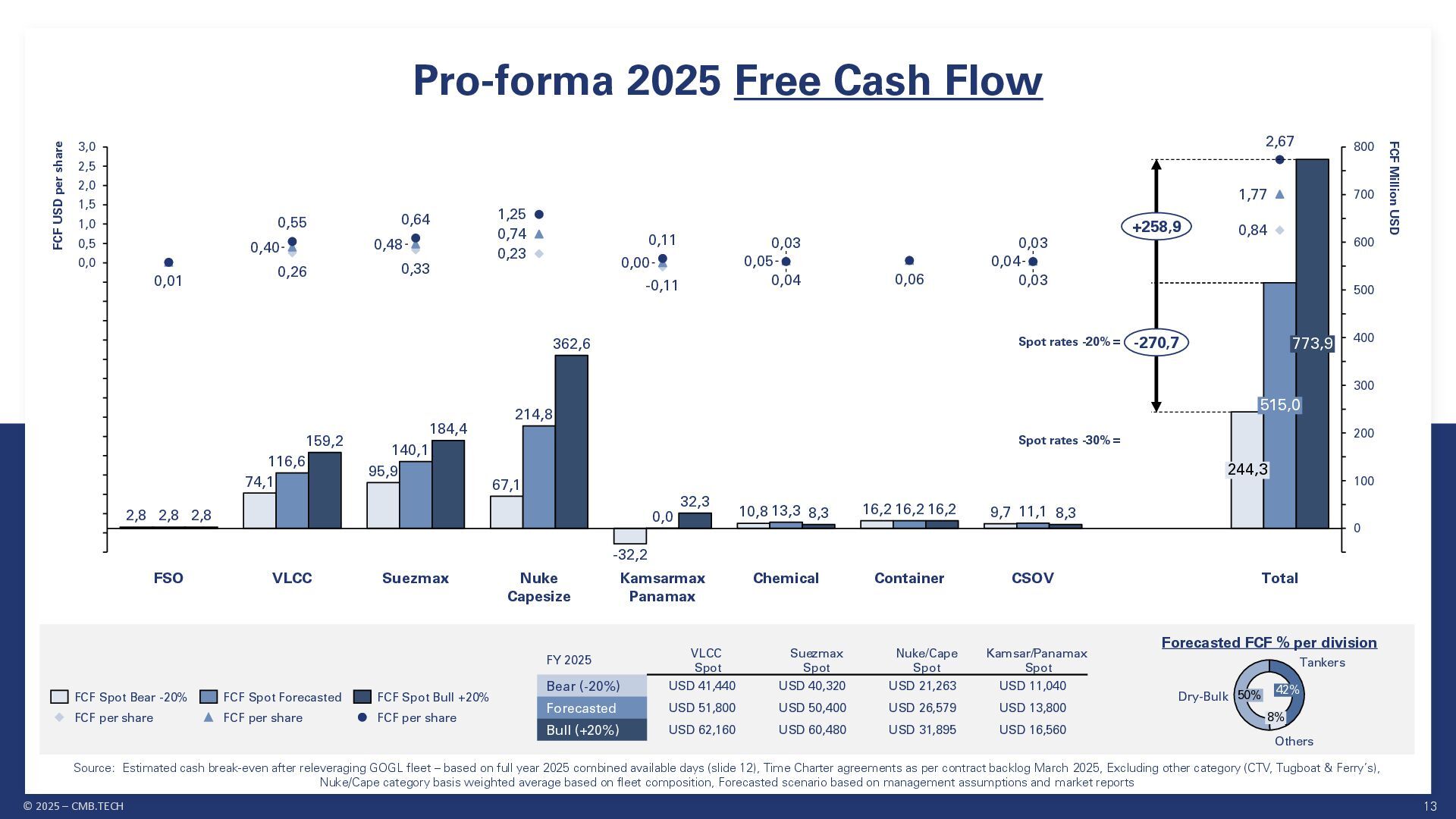

0,06 0,03 0,84 0,40 0,48 0,74 0,00 0,05 0,04 1,77 0,01 0,55 0,64 1,25 0,11 0,03 0,03 2,67 0 100 200 300 400 500 600 700 800 0,0 0,5 1,0 1,5 2,0 2,5 3,0 Chemical Container CSOV Total 2,8 FCF Million USD FCF USD per share FSO VLCC Suezmax Nuke Capesize 2,8 2,8 74,1 116,6 159,2 95,9 140,1 184,4 Kamsarmax Panamax 214,8 362,6 -32,2 0,0 32,3 10,8 13,3 8,3 67,1 16,2 16,2 9,7 11,1 8,3 773,9 515,0 244,3 16,2 +258,9 -270,7 FCF Spot Bear -20% FCF per share FCF Spot Forecasted FCF per share FCF Spot Bull +20% FCF per share Pro-forma 2025 Free Cash Flow FY 2025 VLCC Spot Suezmax Spot Nuke/Cape Spot Kamsar/Panamax Spot Bear (-20%) USD 41,440 USD 40,320 USD 21,263 USD 11,040 Forecasted USD 51,800 USD 50,400 USD 26,579 USD 13,800 Bull (+20%) USD 62,160 USD 60,480 USD 31,895 USD 16,560 Source: Estimated cash break-even after releveraging GOGL fleet – based on full year 2025 combined available days (slide 12), Time Charter agreements as per contract backlog March 2025, Excluding other category (CTV, Tugboat & Ferry’s), Nuke/Cape category basis weighted average based on fleet composition, Forecasted scenario based on management assumptions and market reports 50% Dry-Bulk 42% Tankers 8% Others Forecasted FCF % per division Spot rates -20% = Spot rates -30% =

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![[email protected] +32 498 61 71 11 JORIS DAMAN HEAD OF](https://files.speakerdeck.com/presentations/c7e0f1f3dda54b649dcaefbc609be9ea/slide_41.jpg){kind=link}