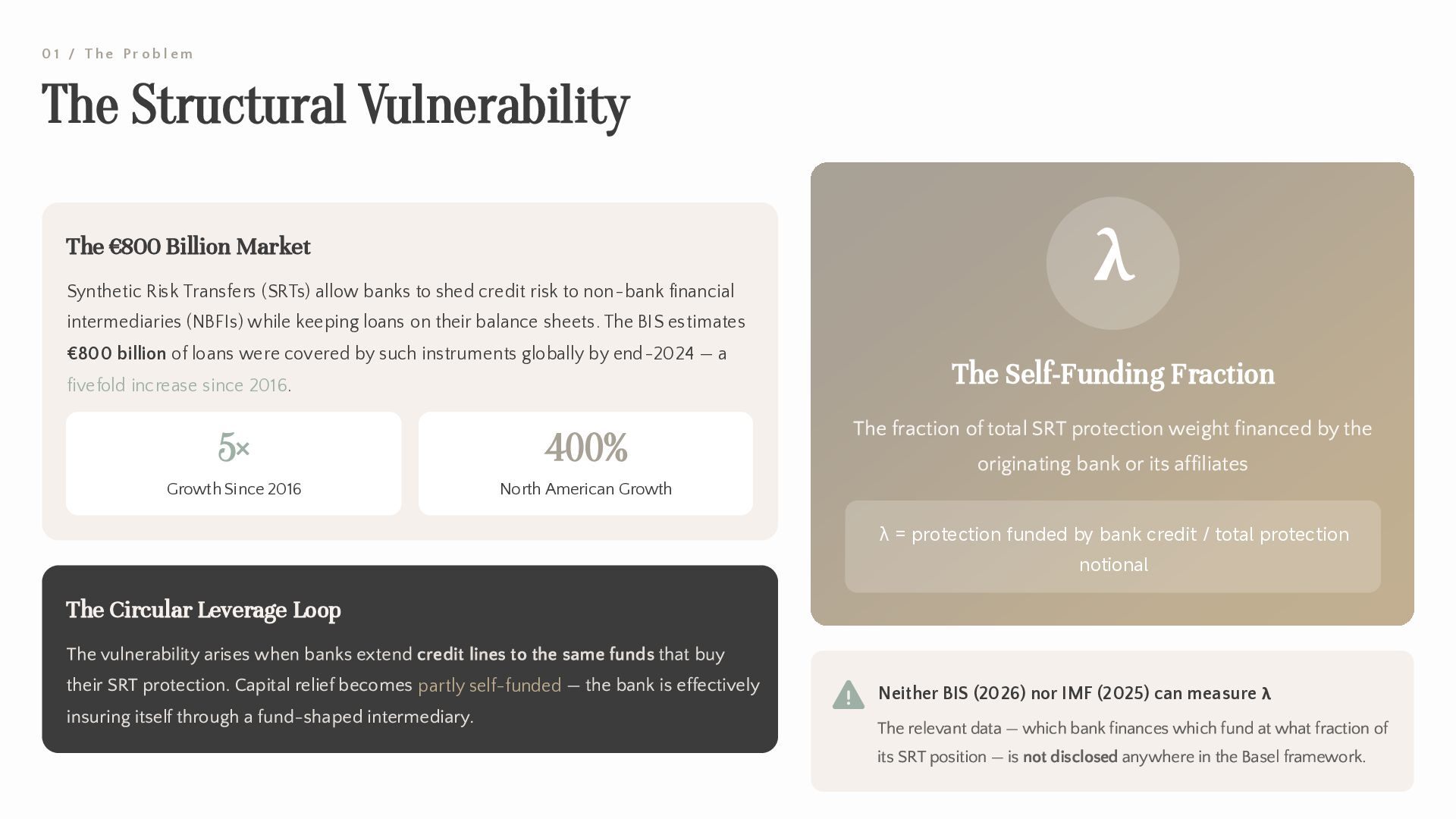

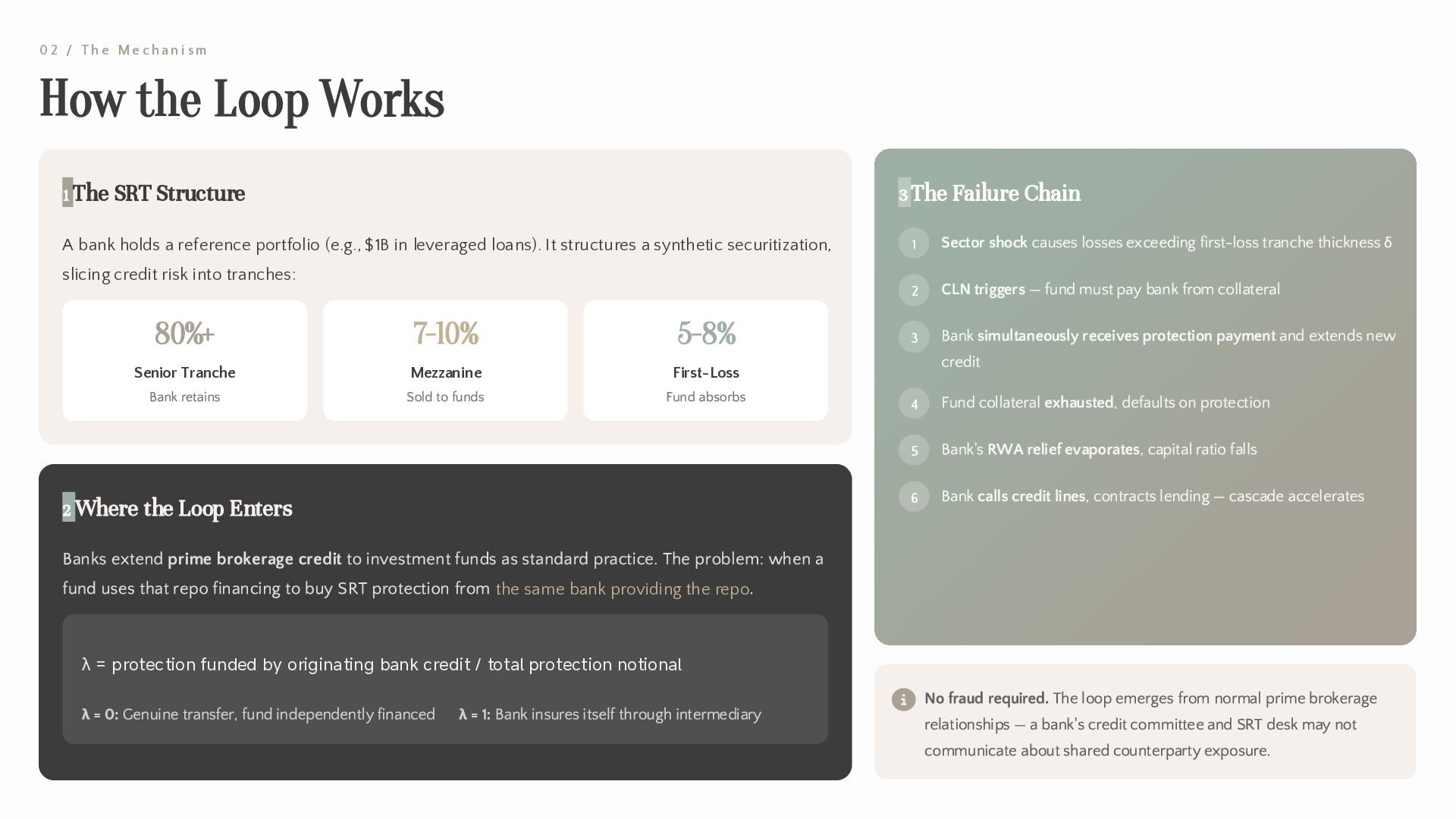

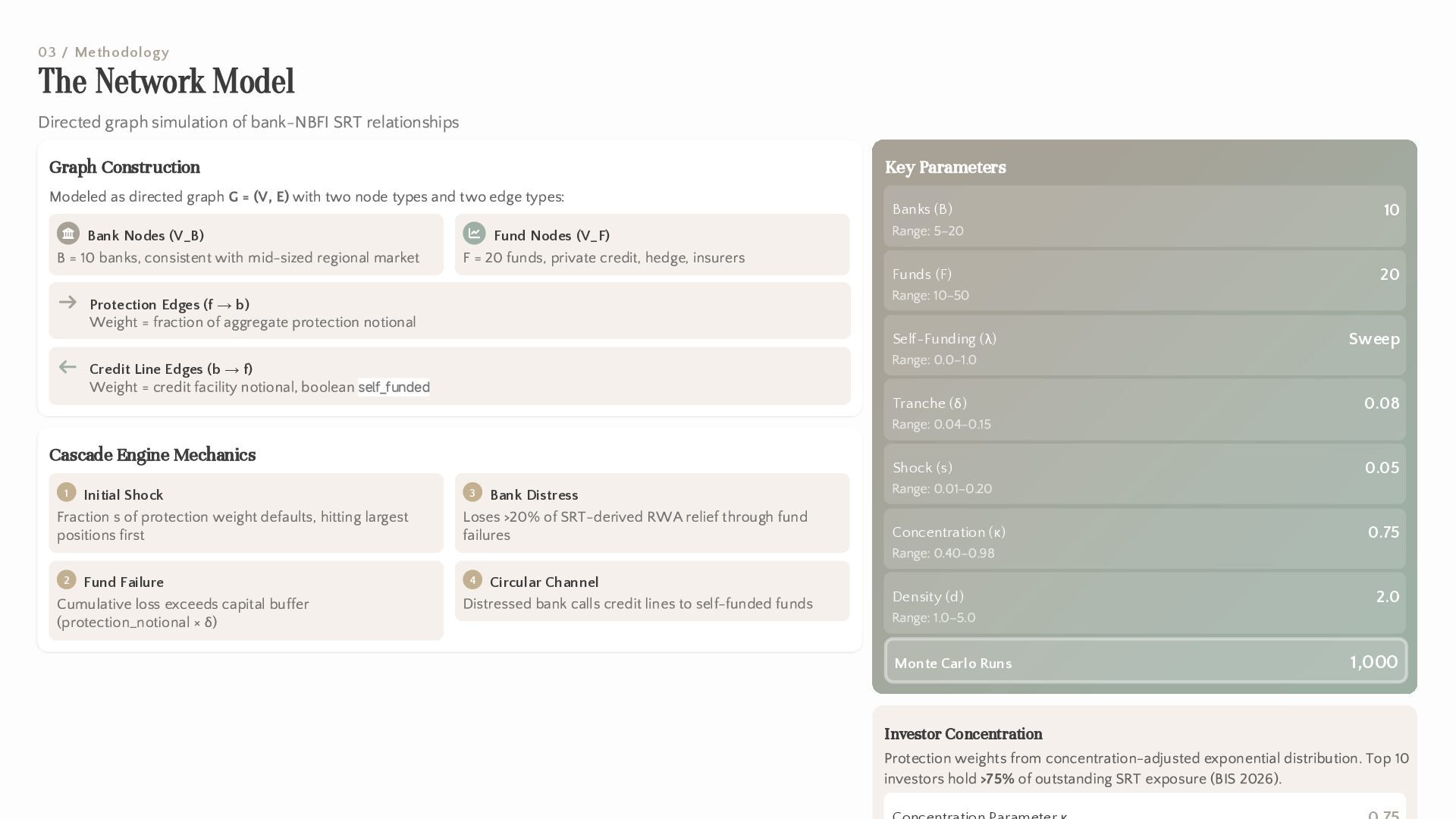

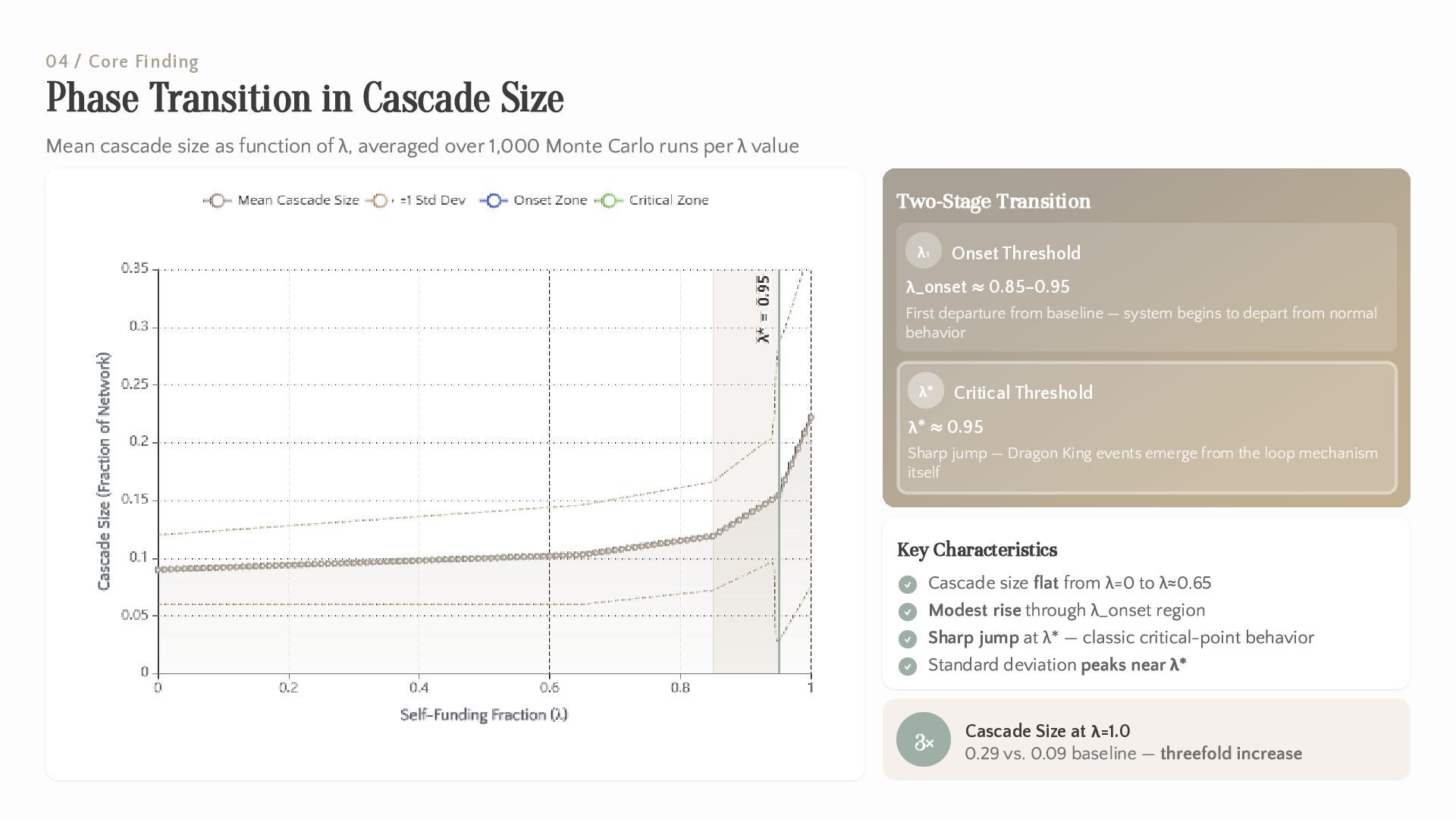

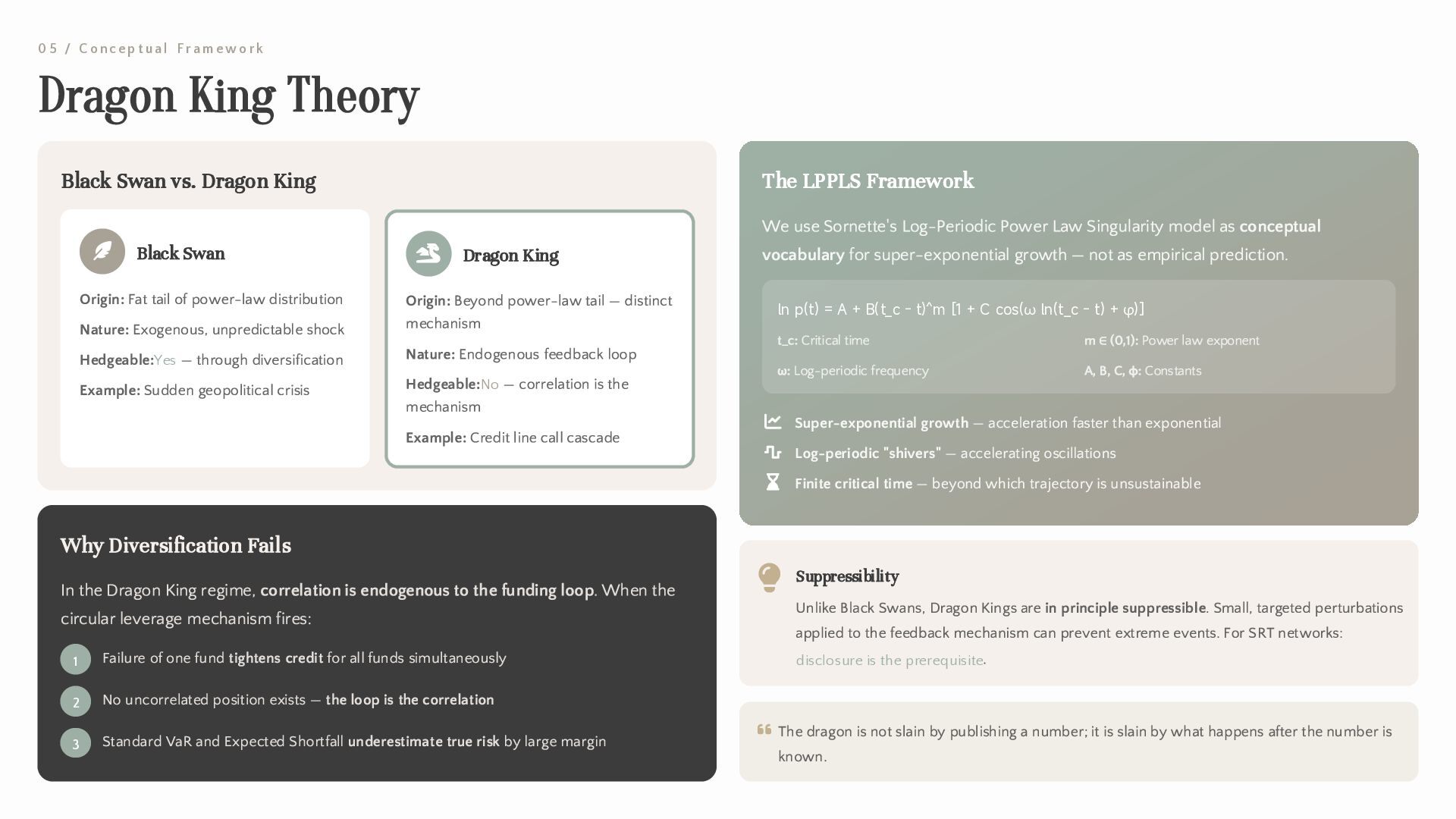

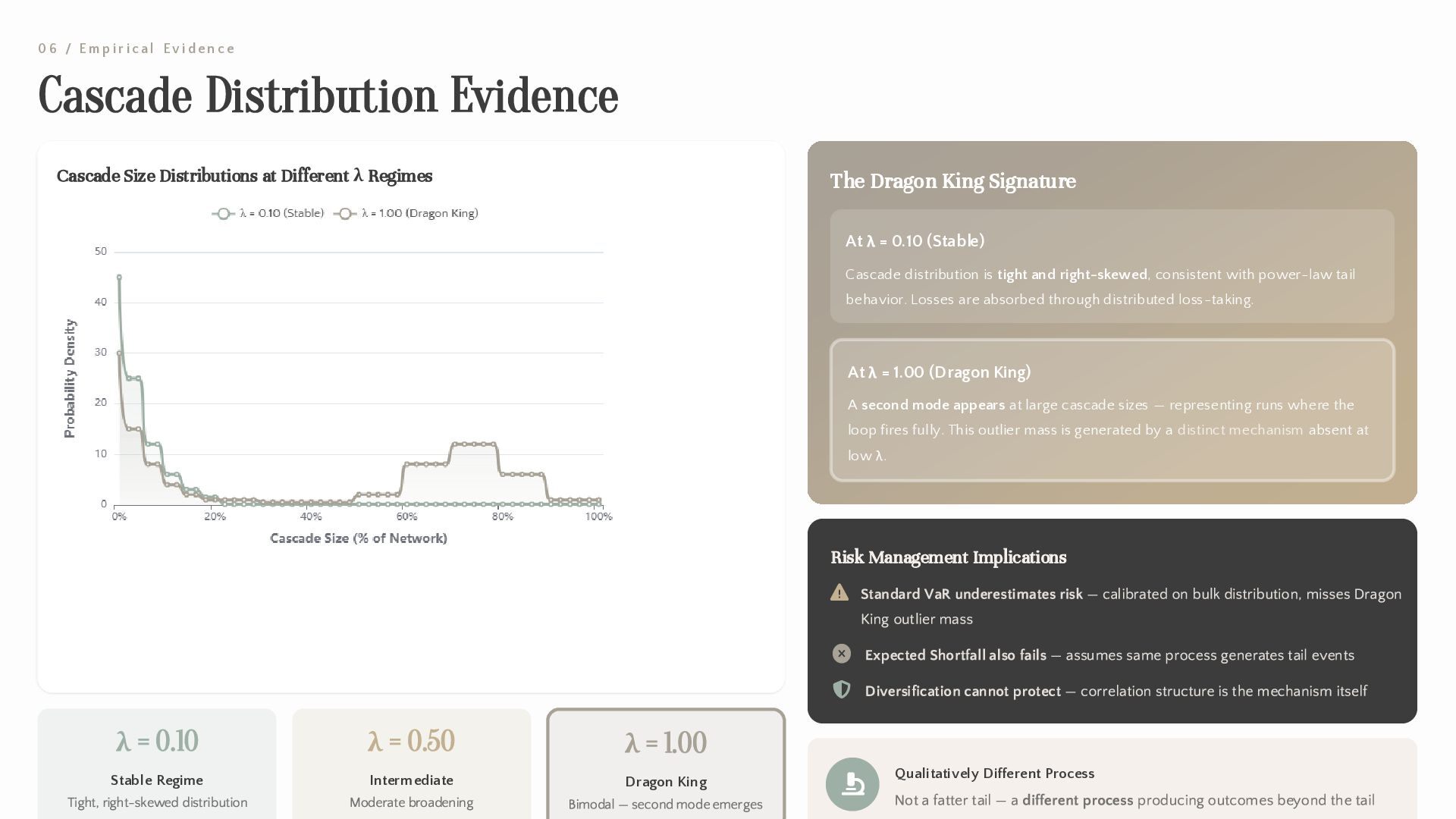

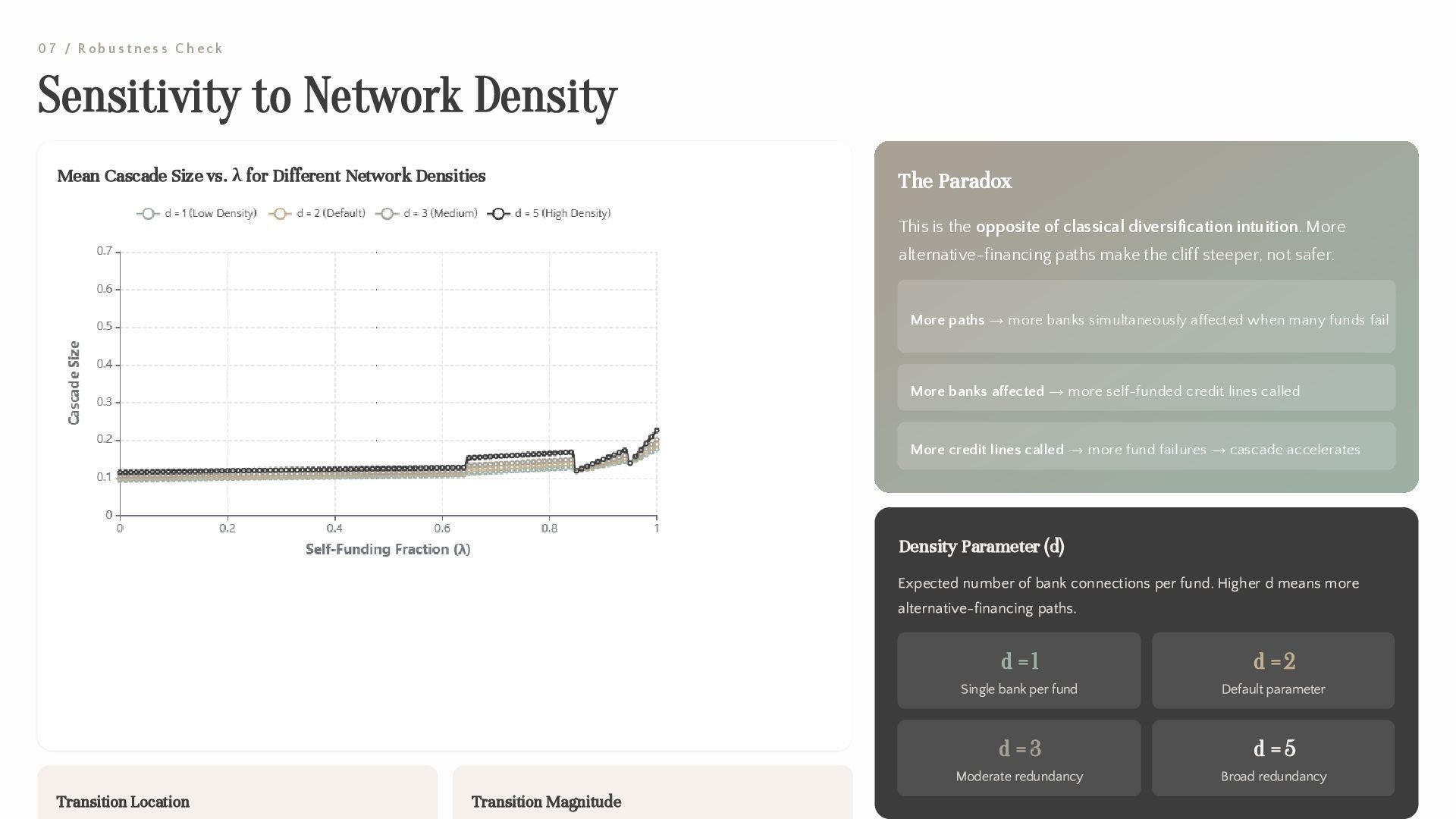

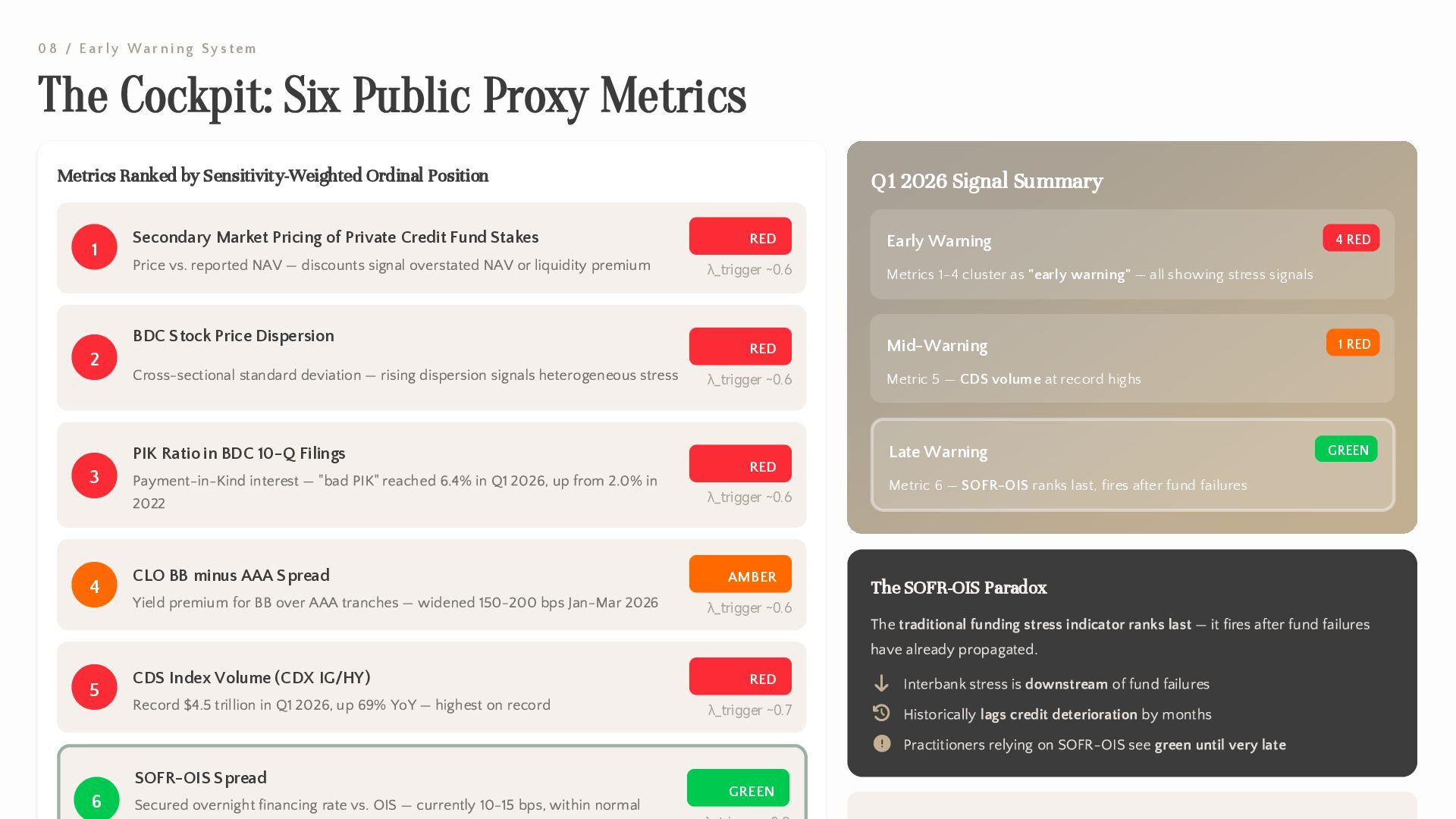

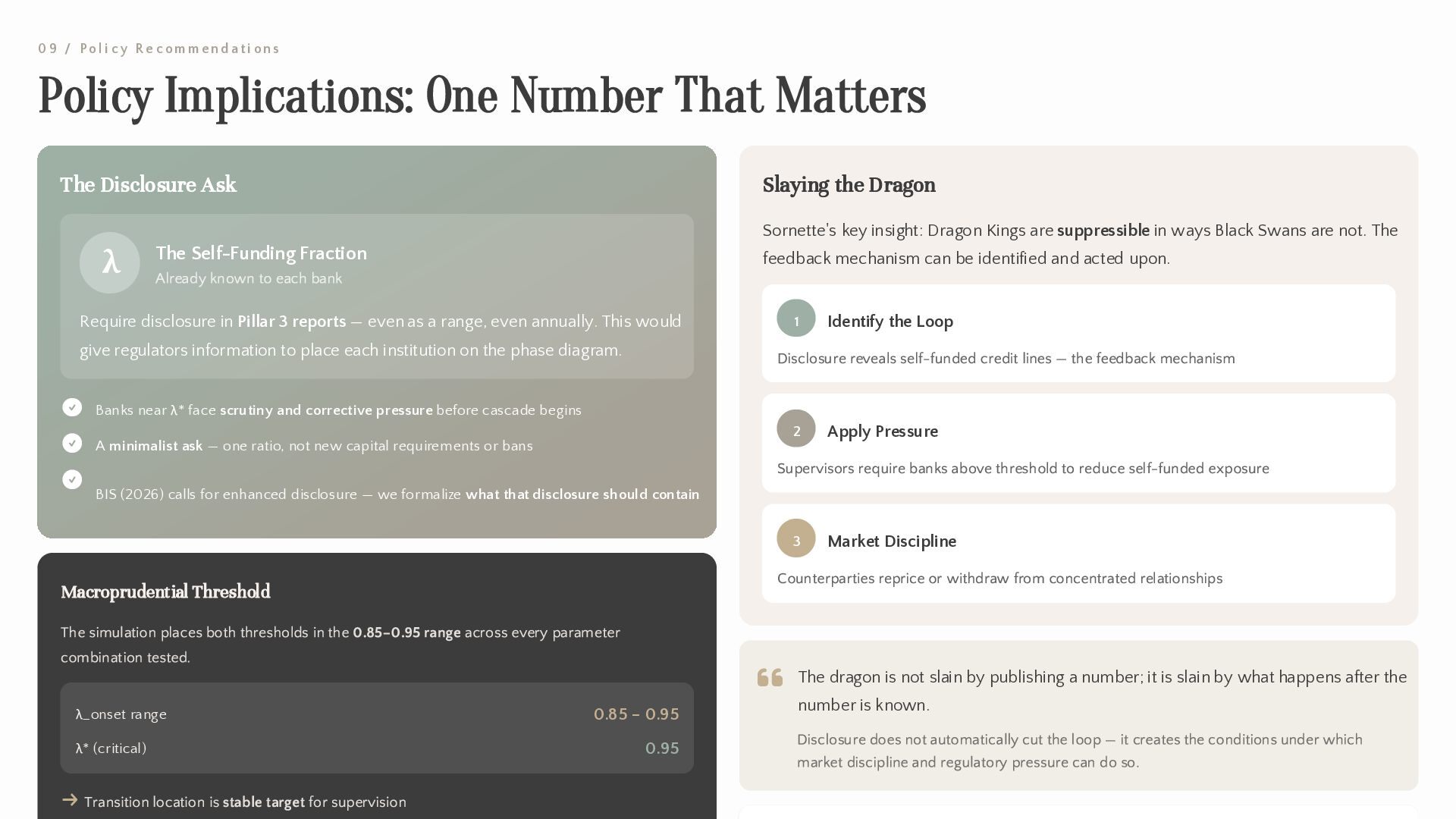

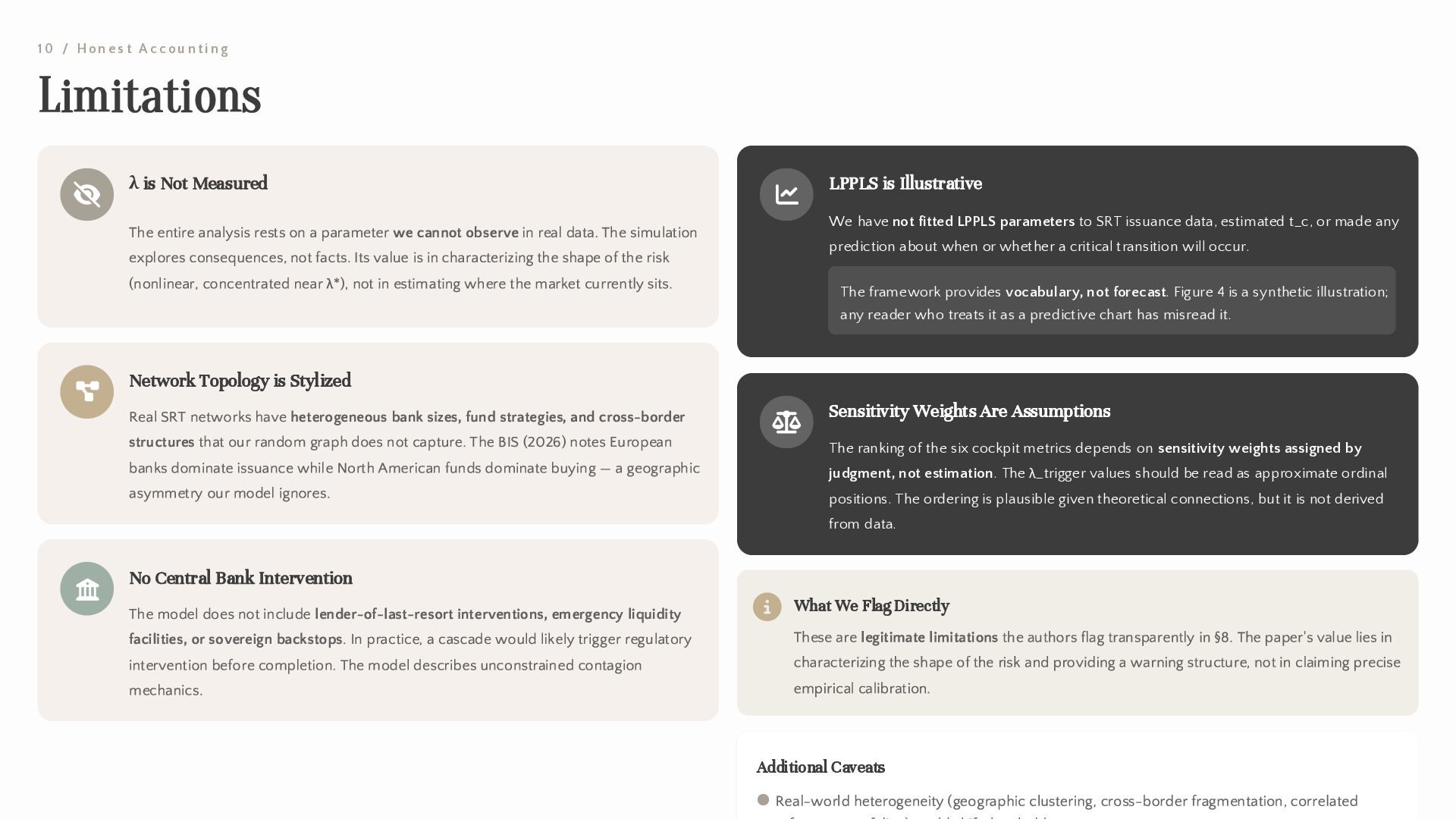

Synthetic Risk Transfers (SRTs) let banks shed credit risk to non-bank financial intermediaries (NBFIs) while keeping the underlying loans on their balance sheets. A structural vulnerability arises when the same banks extend credit lines to the funds that buy their SRT protection, creating a circular leverage loop in which the capital relief is partly self-funded. We formalize this loop as a single parameter, λ, the fraction of total SRT protection weight financed by the originating bank or its affiliates. Using a directed network model of bank-NBFI SRT relationships, we simulate contagion cascades across 1,000 random network realizations for each λ value. The simulation shows a two-stage phase transition: cascade size first departs meaningfully from its baseline at $λ_{onset}$ ≈ 0.85–0.95 (the exact position depends on network density), then jumps sharply at λ* ≈ 0.95 where Dragon King events emerge from the loop mechanism itself. The transition *location* is invariant across network density, investor concentration, shock size, and tranche thickness; what density controls is cascade *magnitude* at high λ, which scales from 0.18 to 0.61 across the tested range. Because λ is not disclosed, we cannot place the real market on this phase diagram. Instead, we propose six publicly observable proxy metrics, computable without proprietary data, ranked by sensitivity-weighted ordinal position relative to λ*. The ranking uses judgment-assigned sensitivity weights and should be read as ordinal. We use the Log-Periodic Power Law Singularity (LPPLS) framework as conceptual vocabulary for the super-exponential growth of SRT issuance observed since 2016, without fitting LPPLS parameters to data or predicting a critical time. As of Q1 2026, four of six proxy metrics show stress signals; the one metric most practitioners watch, SOFR-OIS, does not. One number, λ, would let supervisors place banks on the phase diagram. It is already known to each originating bank and is not reported. Simulation code is released under MIT license.

**Keywords:** synthetic risk transfer, circular leverage, network contagion, phase transition, Dragon King, LPPLS, private credit, systemic risk

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}