• 2007 – built (in house) on line product e-APP • 2007 – On line Members website • 2011 – new on line product T20 – complete with online payment • 2012 – OTIP begins distribution of our T20 On line in Ontario • 2013 – TW (OTIP Brokerage in Alberta) begins distribution (T20, T100) • 2013 – we really begin to believe the internet is going to catch on…we begin the journey to a truly on line product with Acceptiv and TCP. Other pieces had to be in place: • Document Management System (ImageRight) • New Policy Admin System (FIMMAS) • New state of the art phone system • New Members On Line Website • New (PCI Compliant) on line payment system • New Branding – website • New Business Continuity Plan in place • Secure Environment

organization will be licensed in every province Robust marketing/digital/analytics strategy – constant refining of the customer journey Providing administration support for multiple organizations A strong partnership with OTIP to provide products and services to the education community (group and individual) Why change – positive reasons, change is not just driven from fear • Ability to essentially act as a ‘start up’ with a long valued history • Technology costs have gone down • We can appear to ‘punch above our weight’ What this will mean for TL • Build an innovative brand • Flexibility to work with others Things fraternals can do together • Demonstrated the ability to work with others (OTIP) in the new world • Leverage this technology to support distribution networks

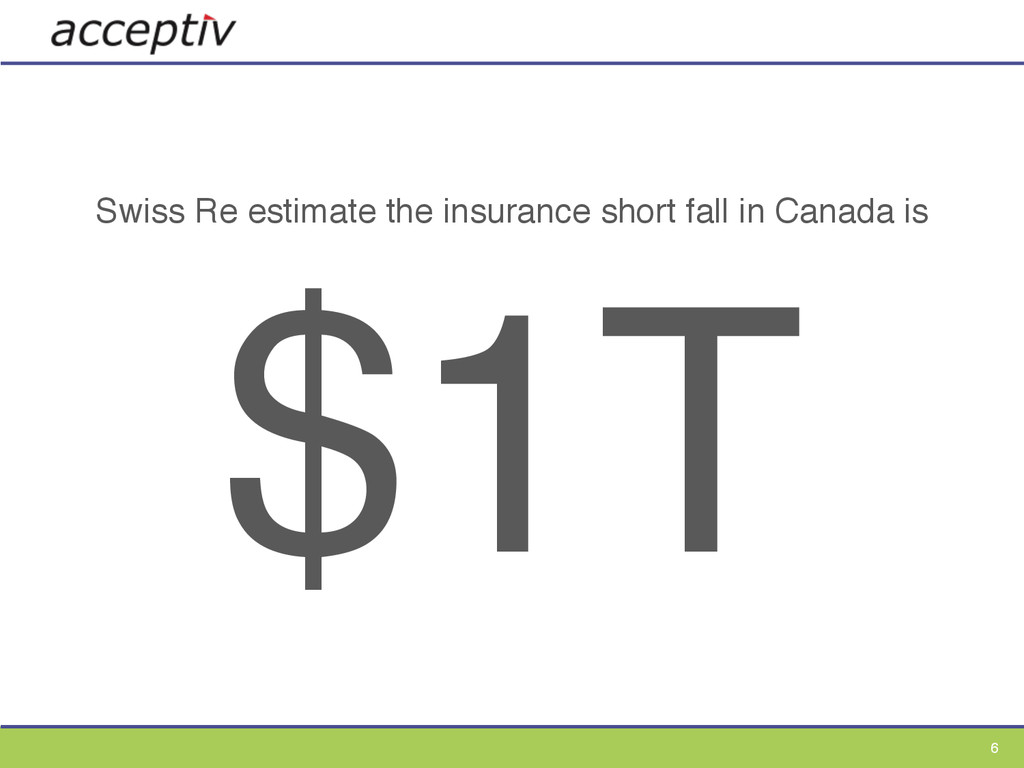

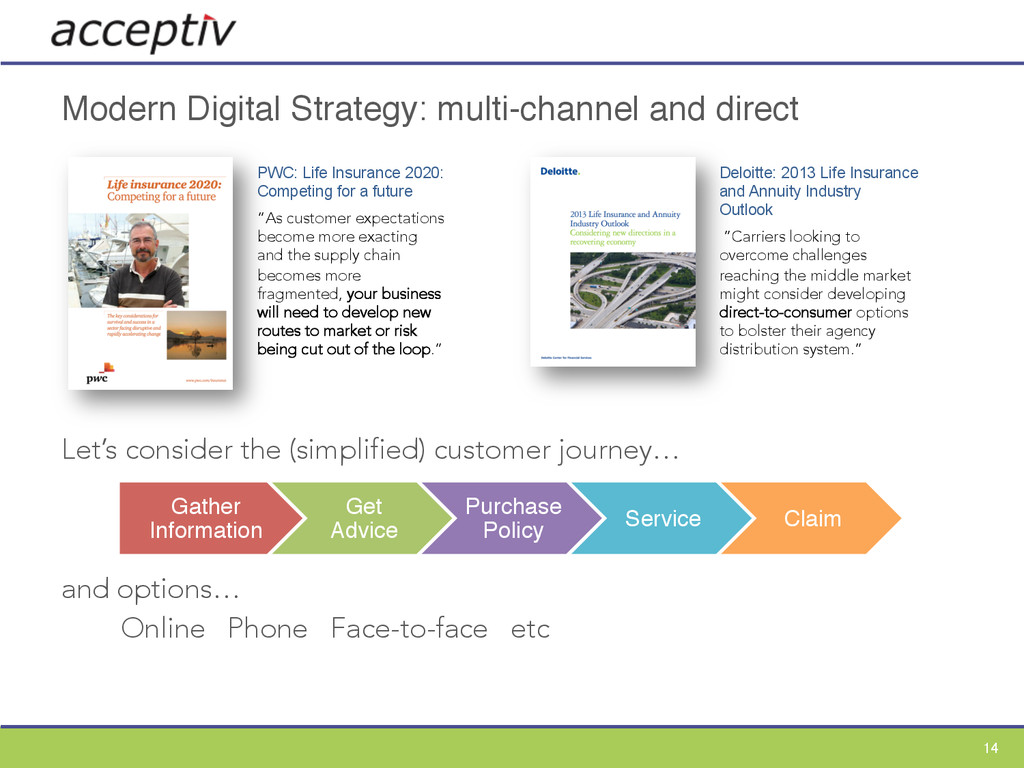

2020: Competing for a future “As customer expectations become more exacting and the supply chain becomes more fragmented, your business will need to develop new routes to market or risk being cut out of the loop.” Deloitte: 2013 Life Insurance and Annuity Industry Outlook ”Carriers looking to overcome challenges reaching the middle market might consider developing direct-to-consumer options to bolster their agency distribution system.” Accenture: The Digital Insurer “The difference between the front-runners and those who are struggling to keep up is, in many cases, the engine that drives them. Old, outdated legacy platforms are costly to maintain and prevent insurers from competing effectively against those with modern, flexible systems. “ Capgemini: Trends in Insurance Channels “To remain competitive in the marketplace, insurers need to redesign their business processes to speed up the automation process and also develop predictive analytics and automated underwriting solutions. “

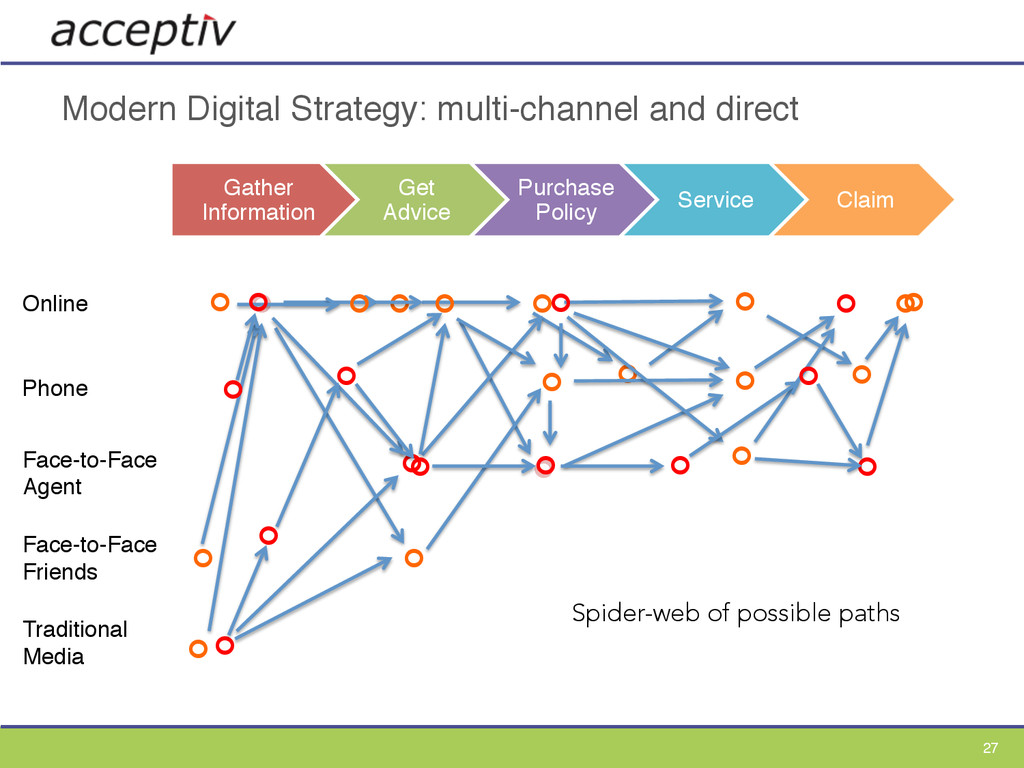

2020: Competing for a future “As customer expectations become more exacting and the supply chain becomes more fragmented, your business will need to develop new routes to market or risk being cut out of the loop.” Deloitte: 2013 Life Insurance and Annuity Industry Outlook ”Carriers looking to overcome challenges reaching the middle market might consider developing direct-to-consumer options to bolster their agency distribution system.” Let’s consider the (simplified) customer journey… and options… Online Phone Face-to-face etc Gather Information Get Advice Purchase Policy Service Claim

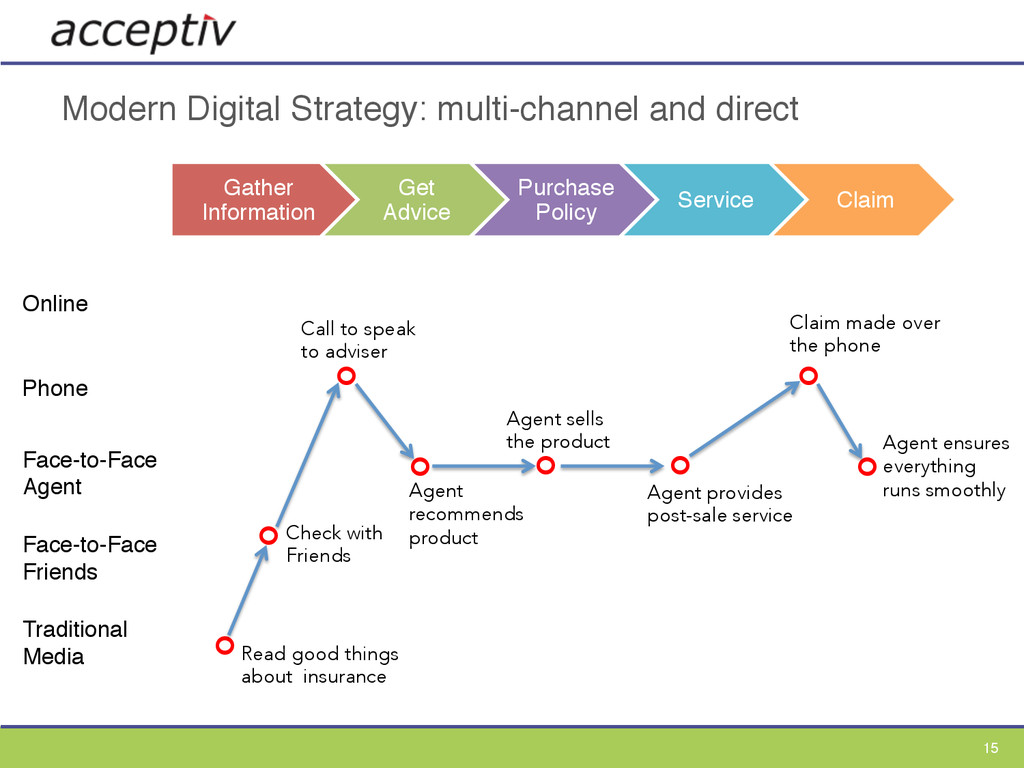

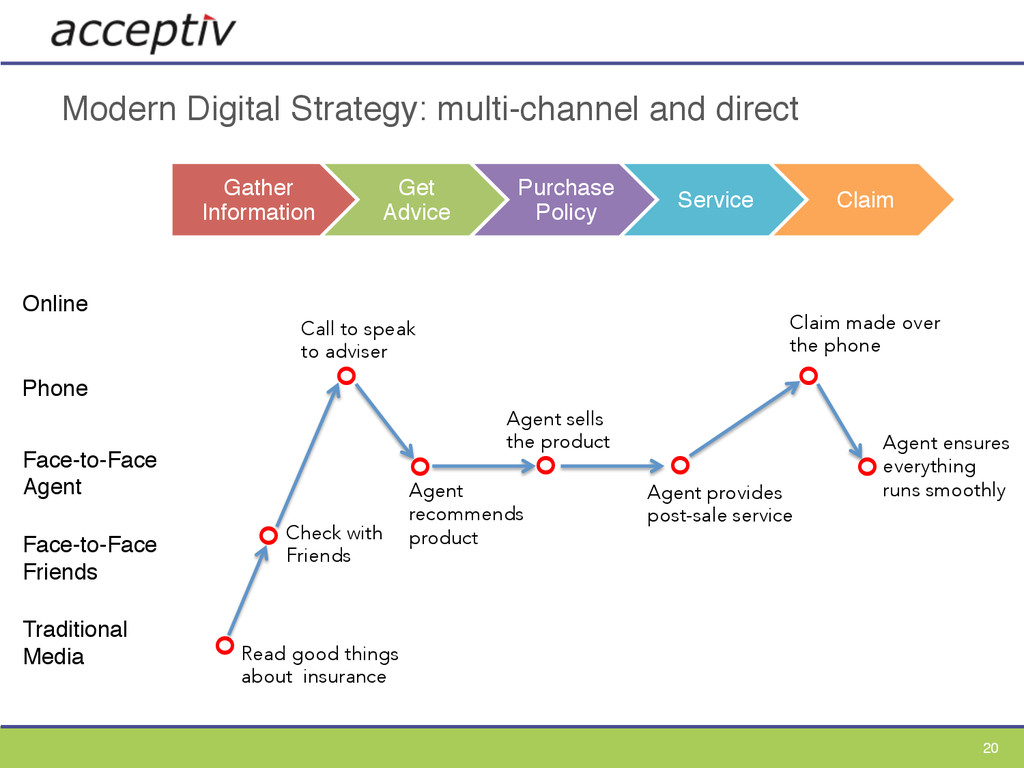

Phone Face-to-Face Agent Face-to-Face Friends Traditional Media ¢ ¢ ¢ ¢ ¢ Call to speak to adviser Agent recommends product Agent sells the product Claim made over the phone Agent provides post-sale service ¢ ¢ Agent ensures everything runs smoothly ¢ Read good things about insurance Check with Friends Modern Digital Strategy: multi-channel and direct

Phone Face-to-Face Agent Face-to-Face Friends Traditional Media ¢ ¢ ¢ ¢ ¢ Call to speak to adviser Agent recommends product Agent sells the product Claim made over the phone Agent provides post-sale service ¢ ¢ Agent ensures everything runs smoothly ¢ Read good things about insurance Check with Friends Modern Digital Strategy: multi-channel and direct

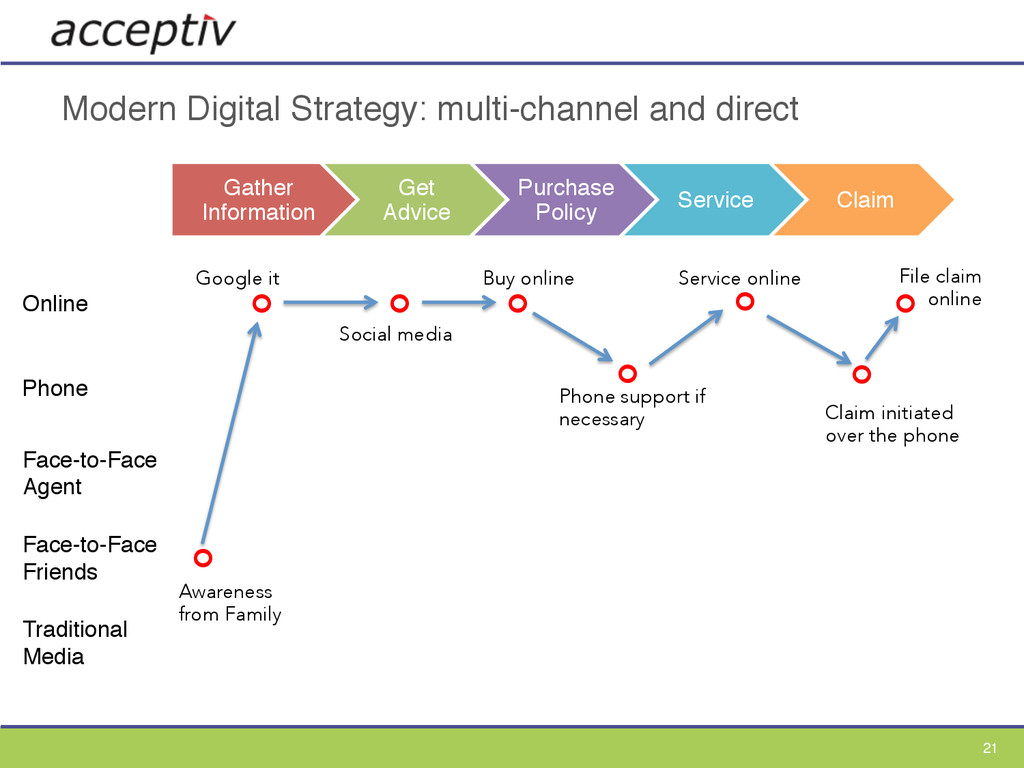

Phone Face-to-Face Agent Face-to-Face Friends Traditional Media ¢ ¢ ¢ ¢ ¢ Social media Buy online Claim initiated over the phone Service online ¢ ¢ Google it Awareness from Family ¢ Phone support if necessary File claim online Modern Digital Strategy: multi-channel and direct

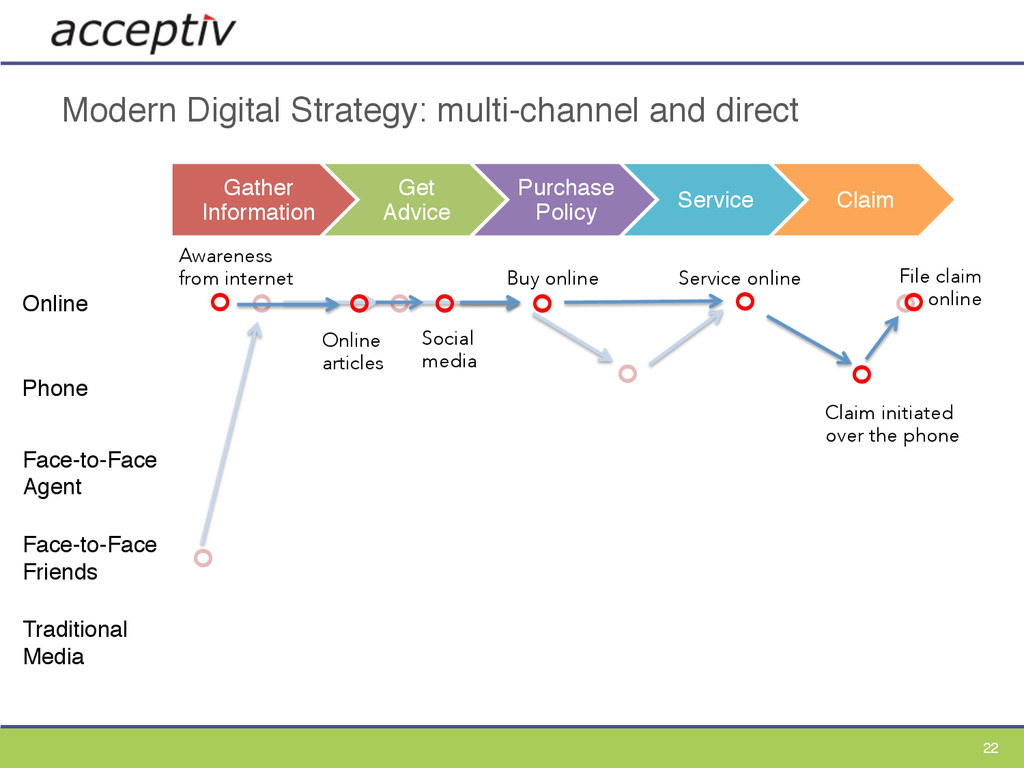

Phone Face-to-Face Agent Face-to-Face Friends Traditional Media ¢ ¢ ¢ ¢ ¢ Online articles Buy online Claim initiated over the phone Service online ¢ ¢ Awareness from internet Social media ¢ ¢ File claim online ¢ ¢ ¢ Modern Digital Strategy: multi-channel and direct

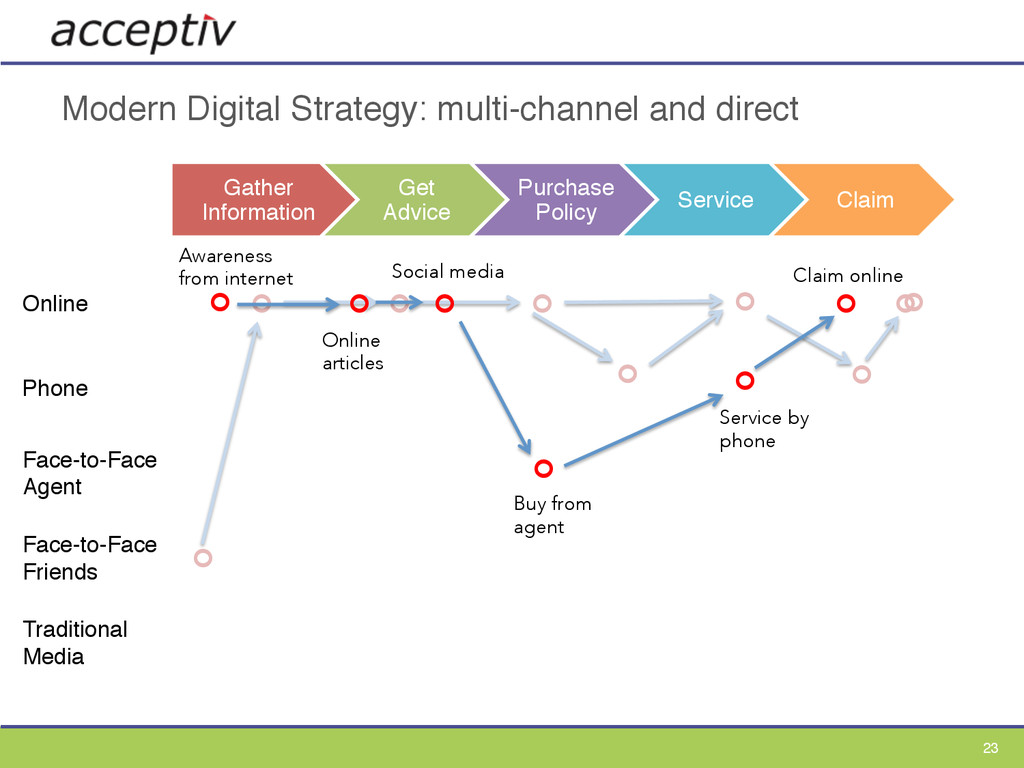

Phone Face-to-Face Agent Face-to-Face Friends Traditional Media ¢ ¢ ¢ ¢ ¢ Online articles Buy from agent Service by phone ¢ ¢ Awareness from internet Social media ¢ ¢ Claim online ¢ ¢ ¢ ¢ ¢ ¢ Modern Digital Strategy: multi-channel and direct

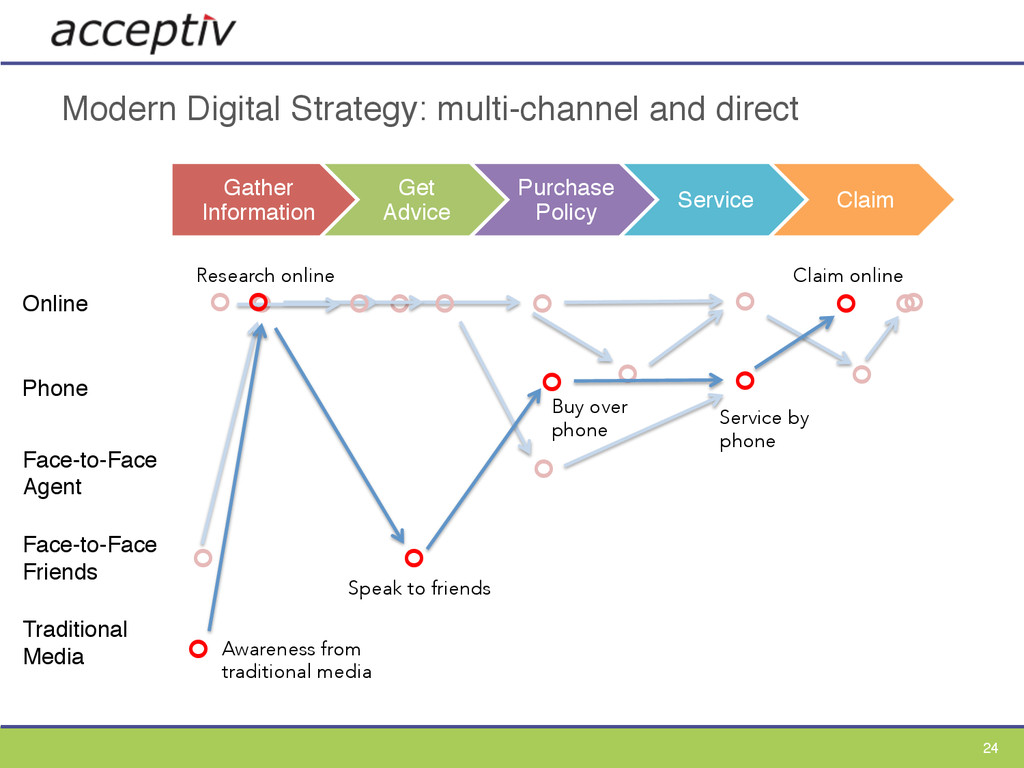

Phone Face-to-Face Agent Face-to-Face Friends Traditional Media ¢ ¢ ¢ ¢ ¢ Buy over phone Service by phone ¢ ¢ Research online ¢ Speak to friends ¢ Claim online ¢ ¢ ¢ ¢ ¢ ¢ ¢ ¢ ¢ Awareness from traditional media ¢ Modern Digital Strategy: multi-channel and direct

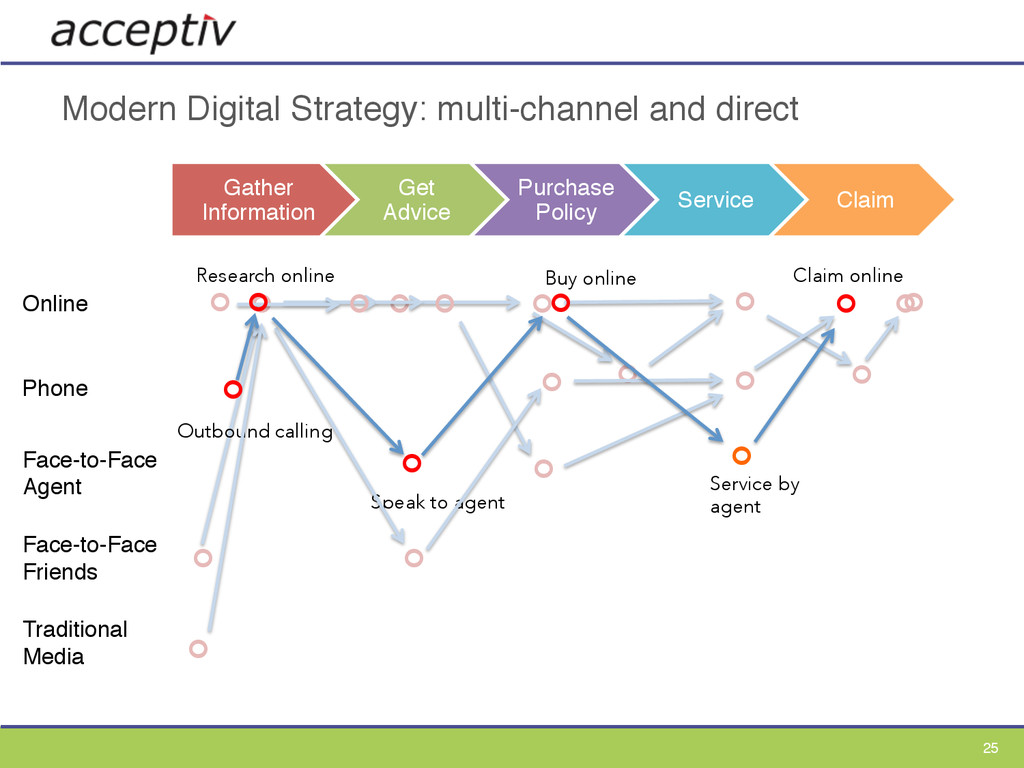

Phone Face-to-Face Agent Face-to-Face Friends Traditional Media ¢ ¢ ¢ ¢ ¢ Buy online Service by agent ¢ ¢ Research online ¢ Speak to agent ¢ Claim online ¢ ¢ ¢ ¢ ¢ ¢ ¢ ¢ ¢ Outbound calling ¢ ¢ ¢ ¢ ¢ Modern Digital Strategy: multi-channel and direct

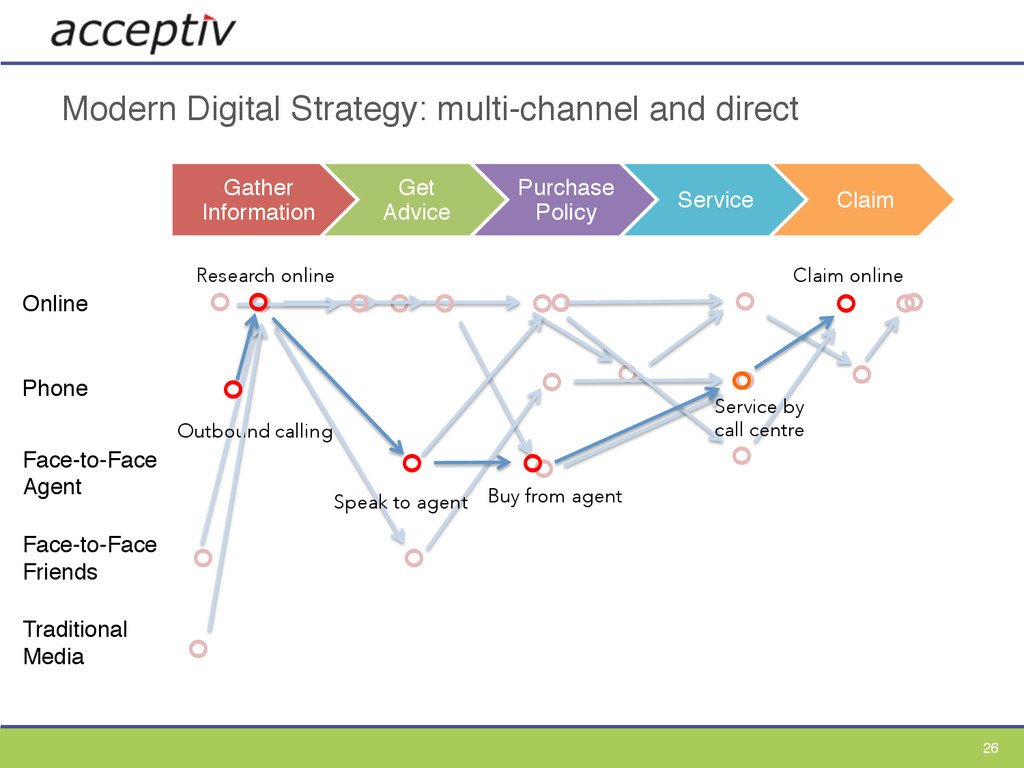

Phone Face-to-Face Agent Face-to-Face Friends Traditional Media ¢ ¢ ¢ ¢ ¢ Buy from agent ¢ ¢ Research online ¢ ¢ Claim online ¢ ¢ ¢ ¢ ¢ ¢ ¢ ¢ ¢ Outbound calling ¢ ¢ ¢ ¢ ¢ Modern Digital Strategy: multi-channel and direct ¢ Speak to agent Service by call centre ¢

bought” mindset Direct online only or multi-channel integrated with direct – not silos ‘Online products’, not ‘products online’ Fully underwritten – online consumers shop for price Brand promise Processes to support digital experience Be committed to continued improvement 28

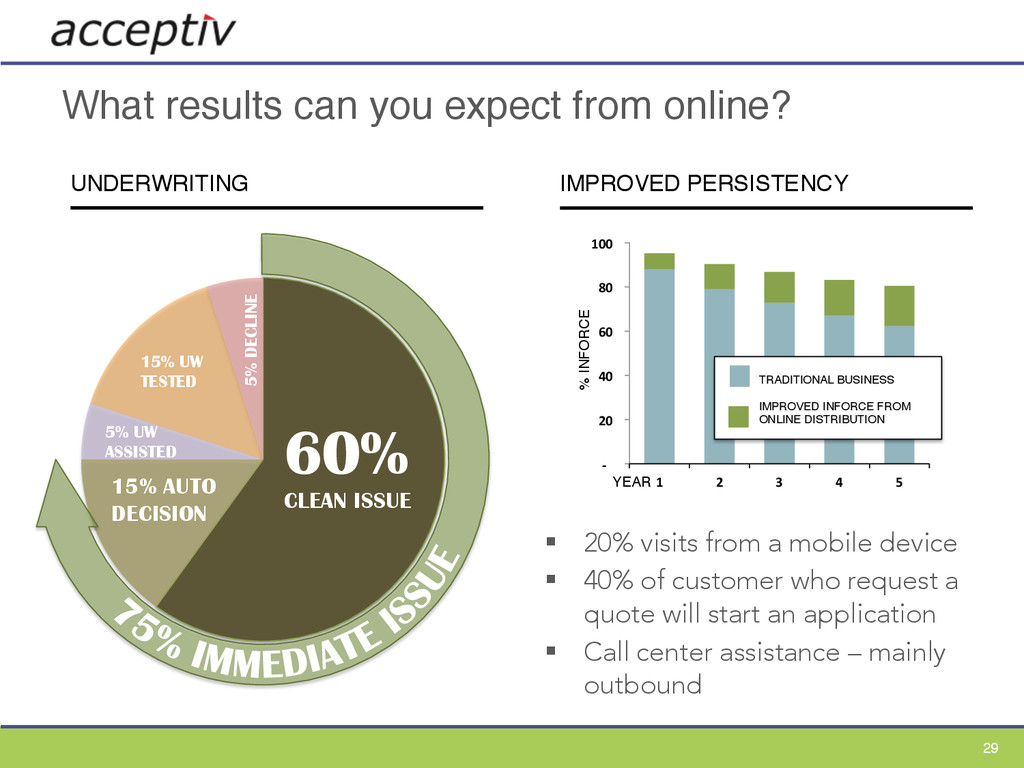

CLEAN ISSUE 15% AUTO DECISION 5% UW ASSISTED 5% DECLINE 15% UW TESTED IMPROVED PERSISTENCY -‐ 20 40 60 80 100 1 2 3 4 5 YEAR % INFORCE TRADITIONAL BUSINESS IMPROVED INFORCE FROM ONLINE DISTRIBUTION § 20% visits from a mobile device § 40% of customer who request a quote will start an application § Call center assistance – mainly outbound

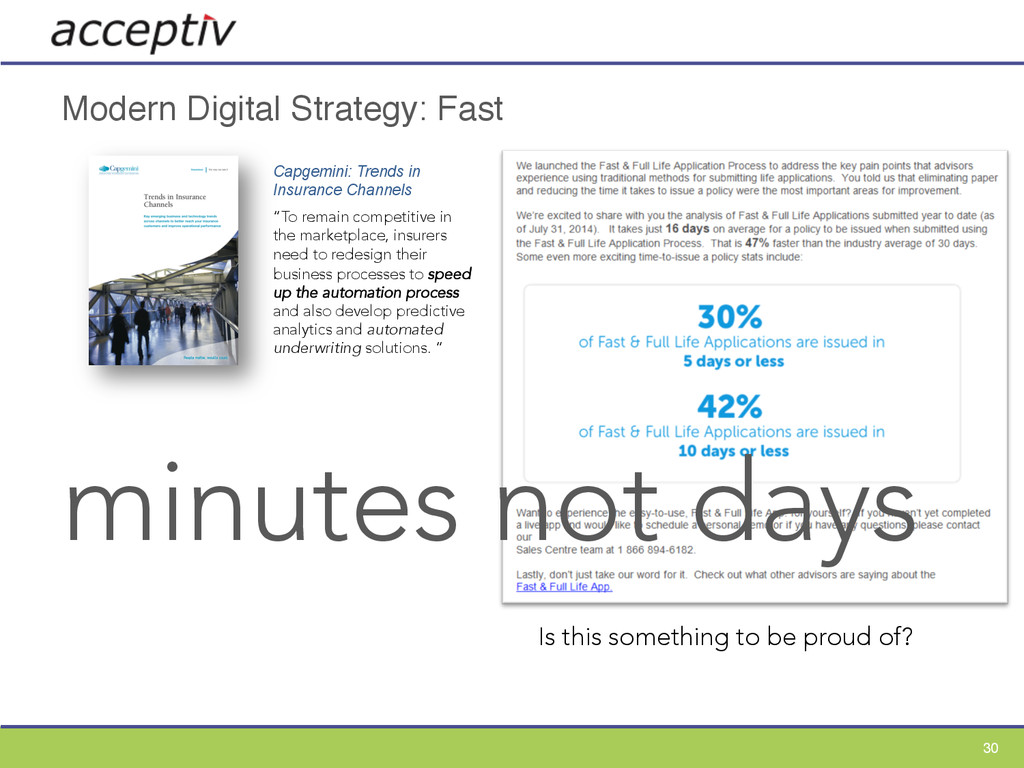

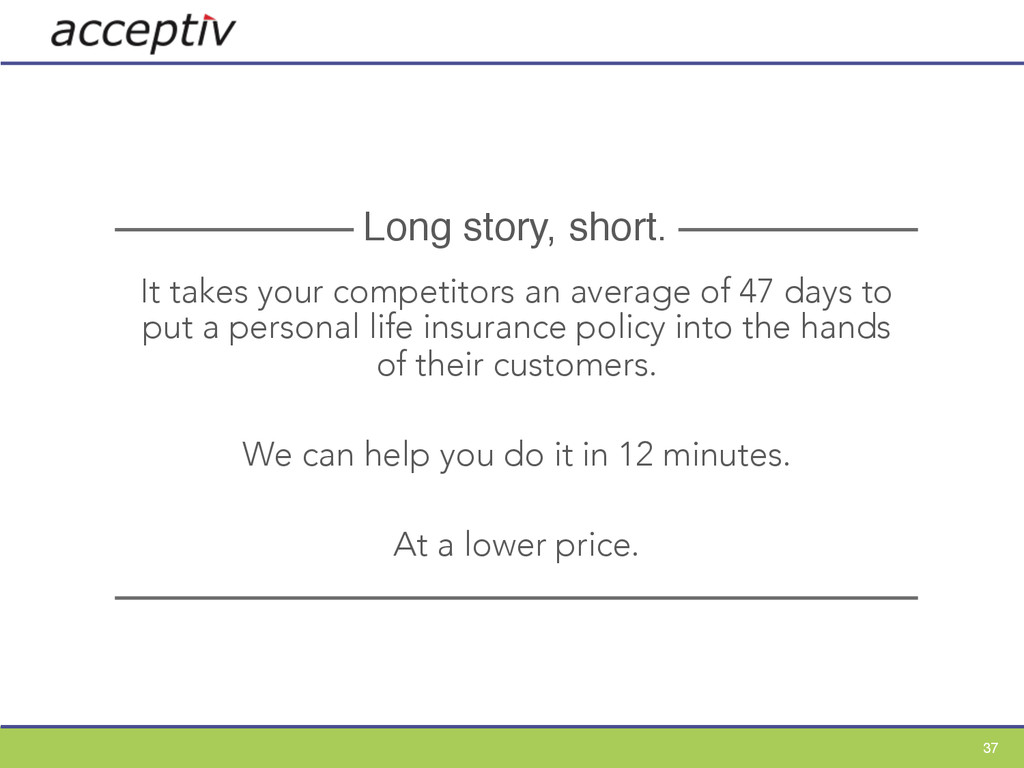

“To remain competitive in the marketplace, insurers need to redesign their business processes to speed up the automation process and also develop predictive analytics and automated underwriting solutions. “ minutes not days Is this something to be proud of?

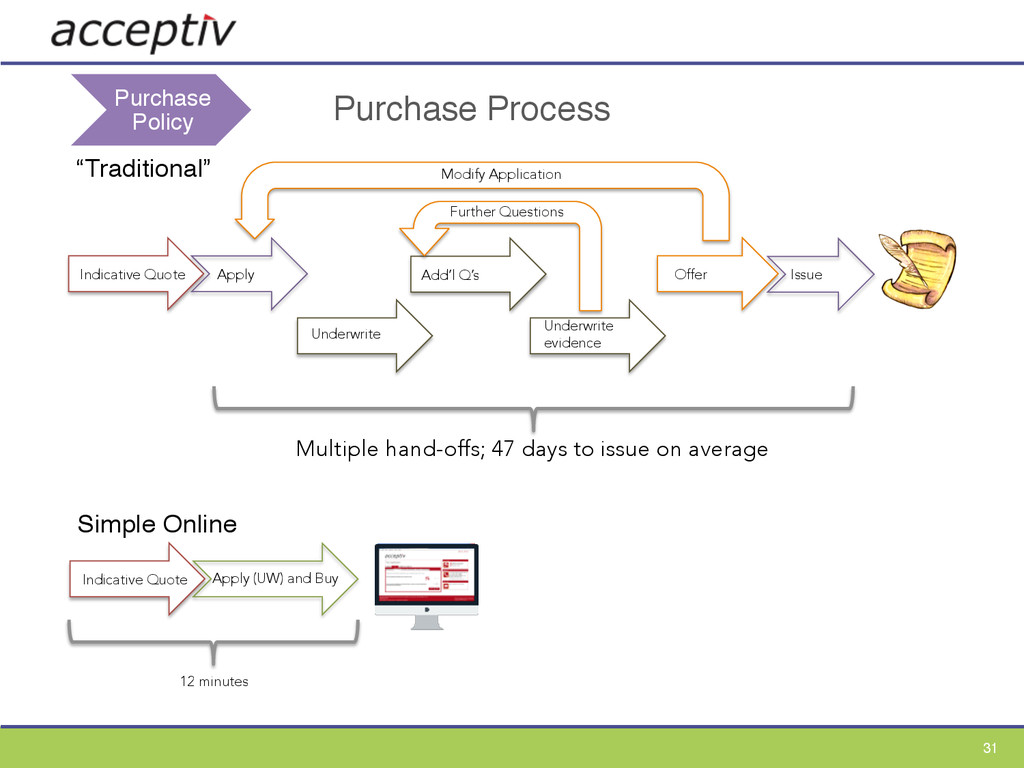

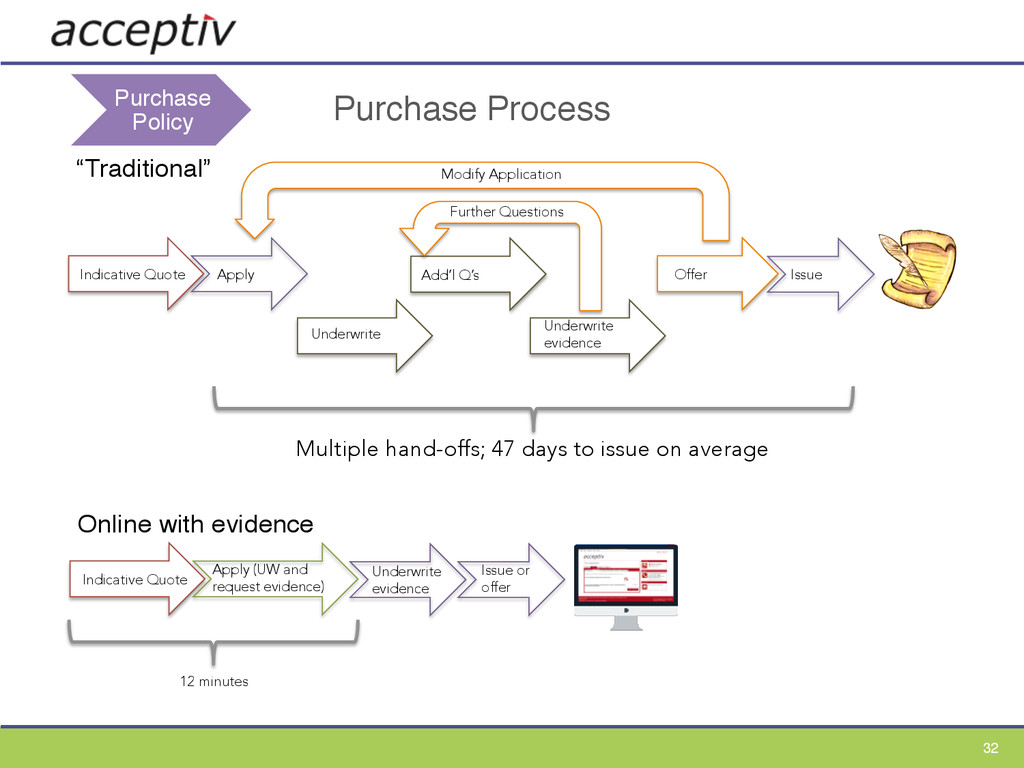

evidence) Online with evidence 12 minutes Purchase Policy Indicative Quote Underwrite Issue Offer Add’l Q’s Multiple hand-offs; 47 days to issue on average Modify Application Apply Underwrite evidence Further Questions Underwrite evidence Issue or offer

“The difference between the front-runners and those who are struggling to keep up is, in many cases, the engine that drives them. Old, outdated legacy platforms are costly to maintain and prevent insurers from competing effectively against those with modern, flexible systems. “ An opportunity for fraternals

Teachers Life to offer a full go to market solution for online fulfillment. At its core is a proven robust TCP system and Acceptiv’s product design. Acceptiv provide the TCP system, product and process design. Teachers Life host the system, provide call center and TPA support. Configured to your brand, customization possible. Faster, less costly, more agile: We offer a fast, economical way to provide online fulfillment. Plus…an entry point to the complete online/ mobile experience that will compete against the largest insurers. 34

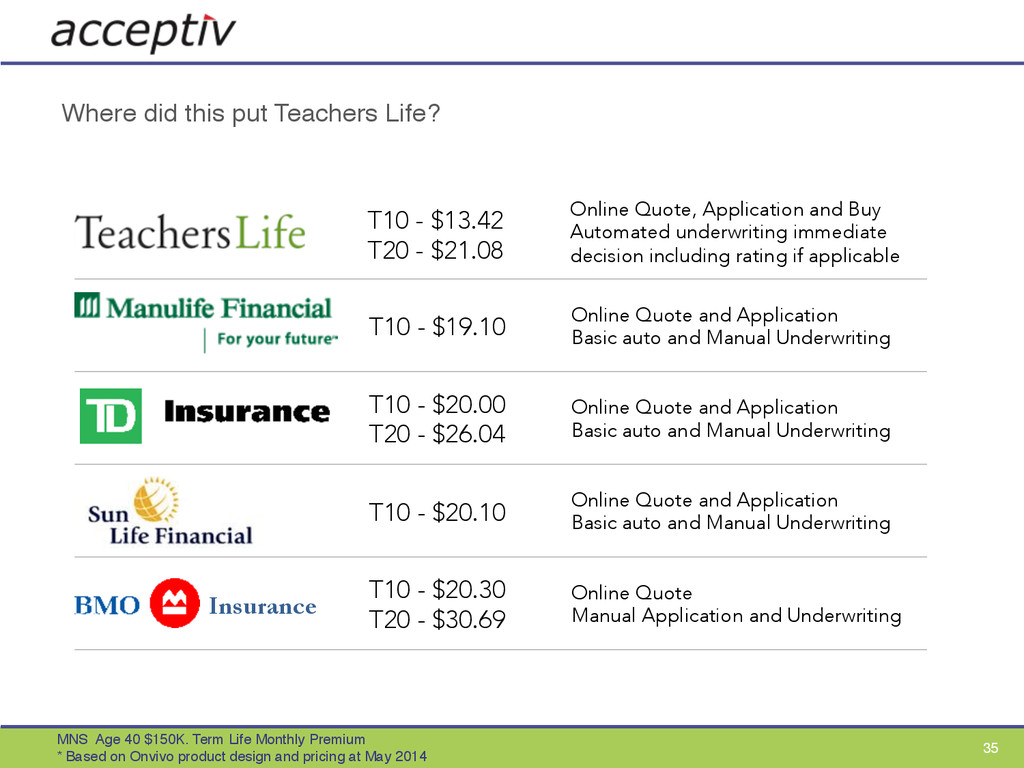

Manual Underwriting T10 - $20.00 T20 - $26.04 Online Quote and Application Basic auto and Manual Underwriting T10 - $20.10 Online Quote and Application Basic auto and Manual Underwriting T10 - $20.30 T20 - $30.69 Online Quote Manual Application and Underwriting Where did this put Teachers Life? MNS Age 40 $150K. Term Life Monthly Premium * Based on Onvivo product design and pricing at May 2014 35 Insurance T10 - $13.42 T20 - $21.08 Online Quote, Application and Buy Automated underwriting immediate decision including rating if applicable

experience • Dynamic, fact-based underwriting engine • Fully hosted turn-key solution • System kept up to date • Configured to your brand • Configured to your premium rates • Massive productivity gain 36

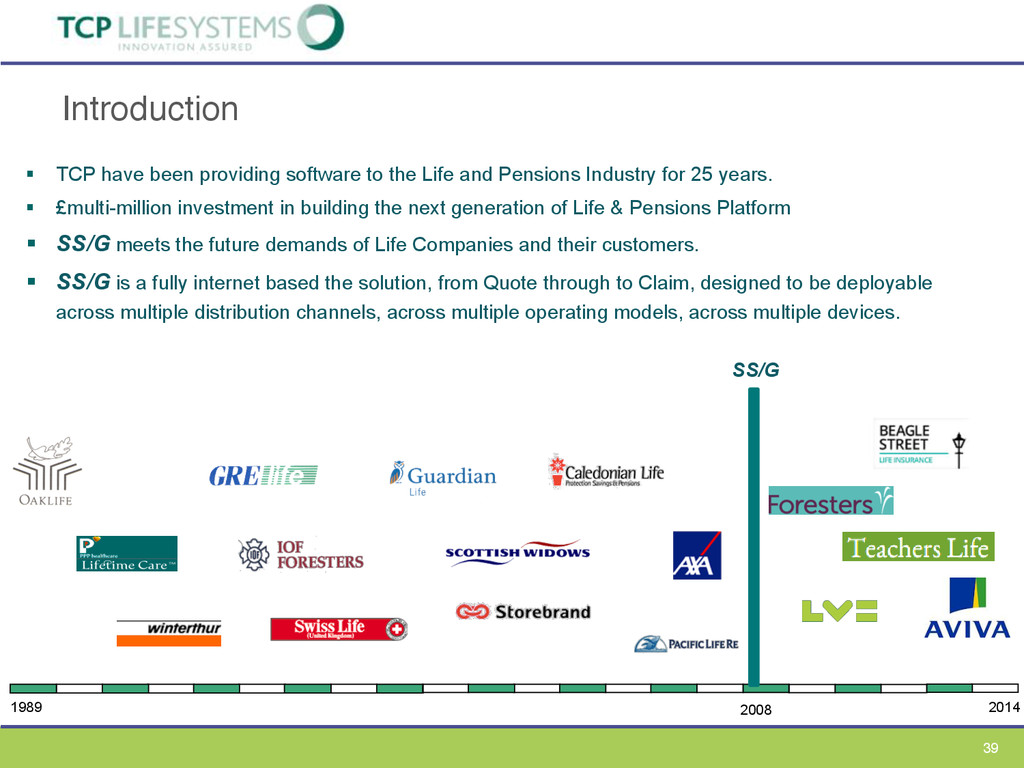

Life and Pensions Industry for 25 years. § £multi-million investment in building the next generation of Life & Pensions Platform § SS/G meets the future demands of Life Companies and their customers. § SS/G is a fully internet based the solution, from Quote through to Claim, designed to be deployable across multiple distribution channels, across multiple operating models, across multiple devices. 1989 2014 2008 SS/G

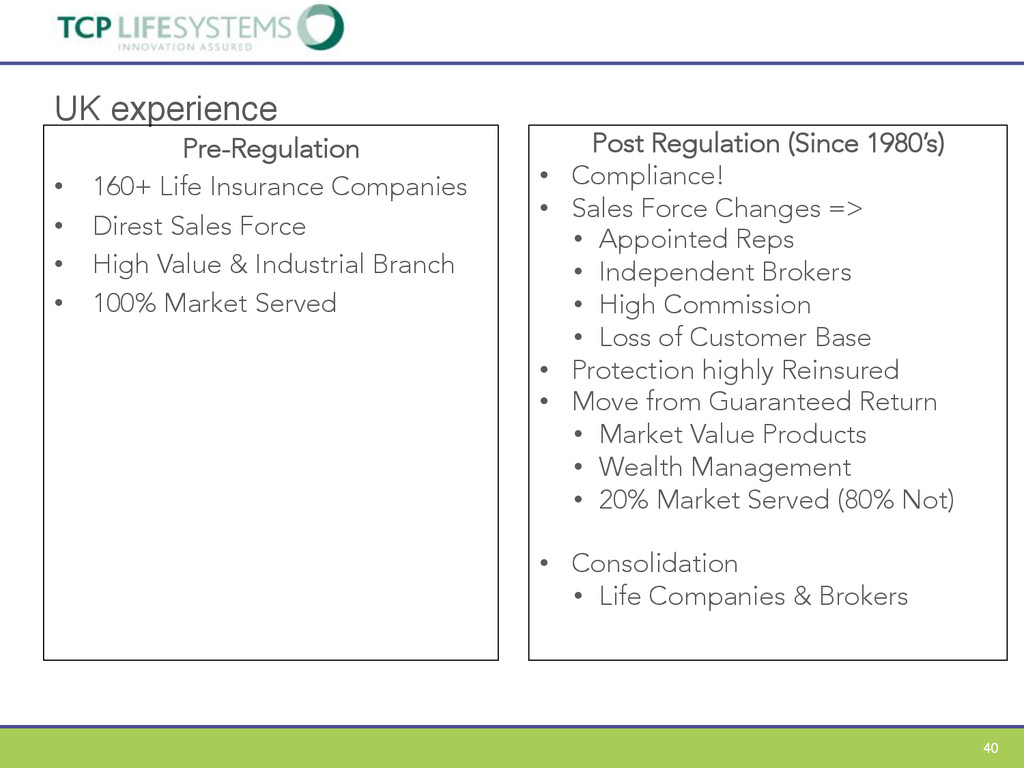

Direst Sales Force • High Value & Industrial Branch • 100% Market Served Post Regulation (Since 1980’s) • Compliance! • Sales Force Changes => • Appointed Reps • Independent Brokers • High Commission • Loss of Customer Base • Protection highly Reinsured • Move from Guaranteed Return • Market Value Products • Wealth Management • 20% Market Served (80% Not) • Consolidation • Life Companies & Brokers

• Life insurance comparison – High commission earnings • Huge Marketing Budget • The first now providing Life Insurance…More products to follow 44 www.youtube.com/watch?v=ON8825F_Be8

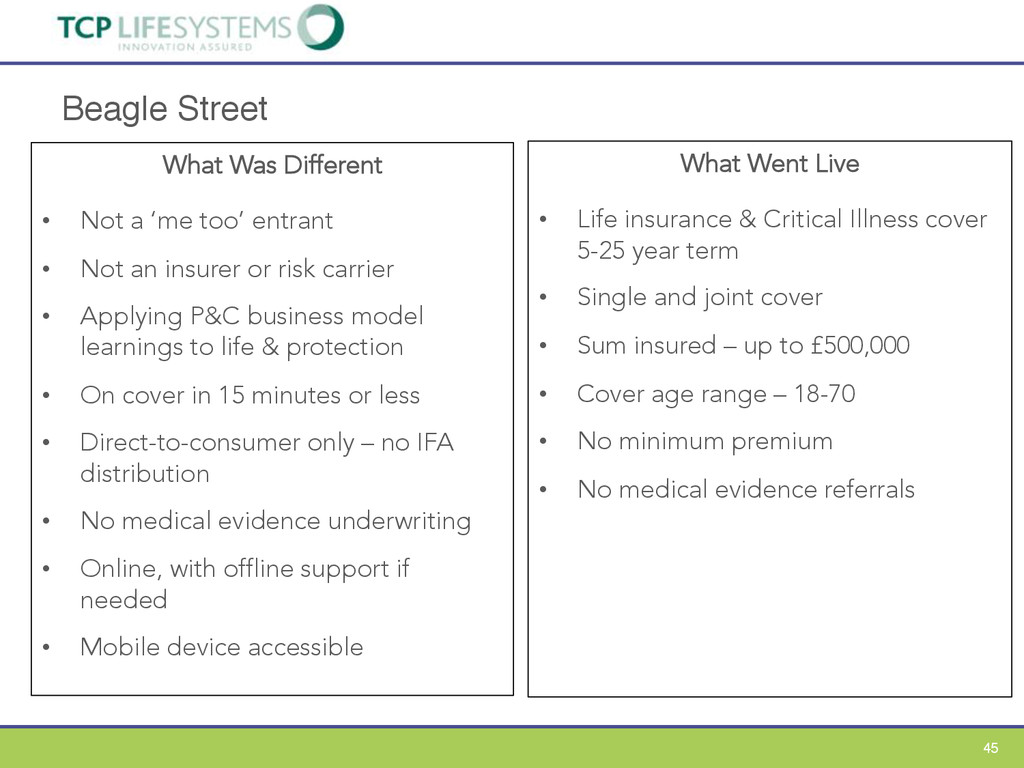

too’ entrant • Not an insurer or risk carrier • Applying P&C business model learnings to life & protection • On cover in 15 minutes or less • Direct-to-consumer only – no IFA distribution • No medical evidence underwriting • Online, with offline support if needed • Mobile device accessible What Went Live • Life insurance & Critical Illness cover 5-25 year term • Single and joint cover • Sum insured – up to £500,000 • Cover age range – 18-70 • No minimum premium • No medical evidence referrals

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}