to micro-insurances to offer them at low handling costs, if underwriting and claims handling can be automated based on defined rules and the availability of reliable data sources. Payouts to insured farmers, for example, might be triggered when drought conditions are reported by verified climate/weather databases. Internet of Things (IoT). Looking forward to the IoT, cars, electronic devices or home appliances can have their own insurance policies registered and administered by smart contracts in a blockchain network, automatically detecting damage first and then triggering the repair process, as well as claims and payments.” by Mckinsey

universal notary service for all the insurance industry, which is capable of eliminating huge losses caused by fraud and double claims,” Man said, “Transactions become instant and cheap due to the rejection of a large number of counterparties and the replacement of complex infrastructure. Previously, it could take several weeks from the insured event to make a payment, but now it’s done in minutes.” 保険取引における不正の検知や、事故や車に傷を つけた際に保険料の支払いを自動で行えるように なる。[1]

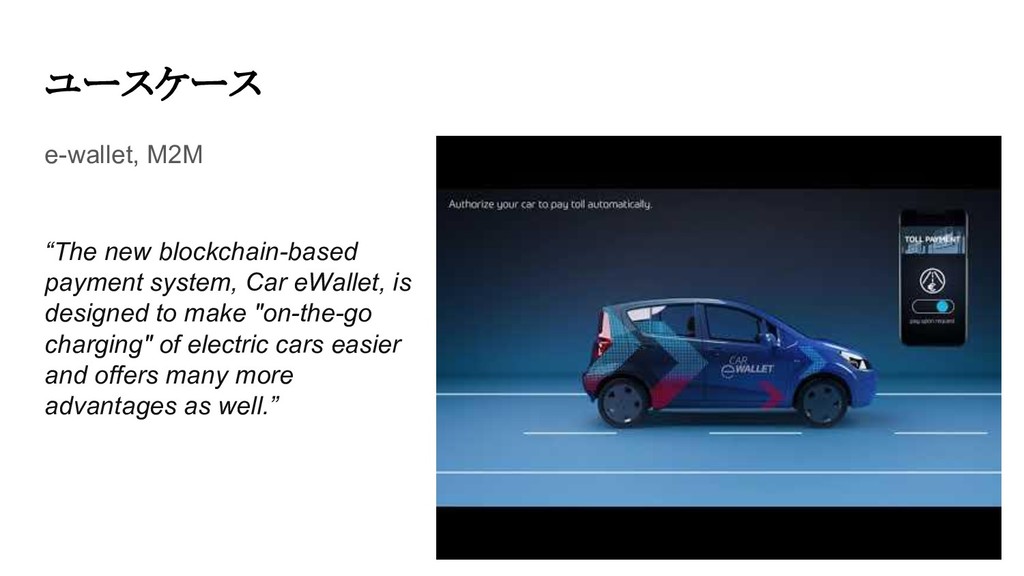

are fast and very secure. The car becomes part of the blockchain, making a direct offline connection possible – that is, without diversion through a server. Taking 1.6 seconds, the process of opening and closing the car via an app is up to six times faster than before. [1] “We want to develop a certificate based on blockchain that ensures a car’s mileage data is correct. Last year, we started with a proof of concept and connected a real car to the blockchain. We installed a connectivity device in the car to read its mileage data. Using the connectivity device we then transmitted the data to a backend which is connected to a blockchain.” [2] 12/05/2017

us the chance to reimagine how the unknown and risk factors could be taken out of the buying process, while giving more tools to financial services and insurance companies to offer new products and services.” [1] “Ethereum-powered platform aimed to reward users for sharing their transport data.the token could potentially be used for riding public transport, vehicle rentals, and enabling users to share their vehicle or travel data.”[2]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

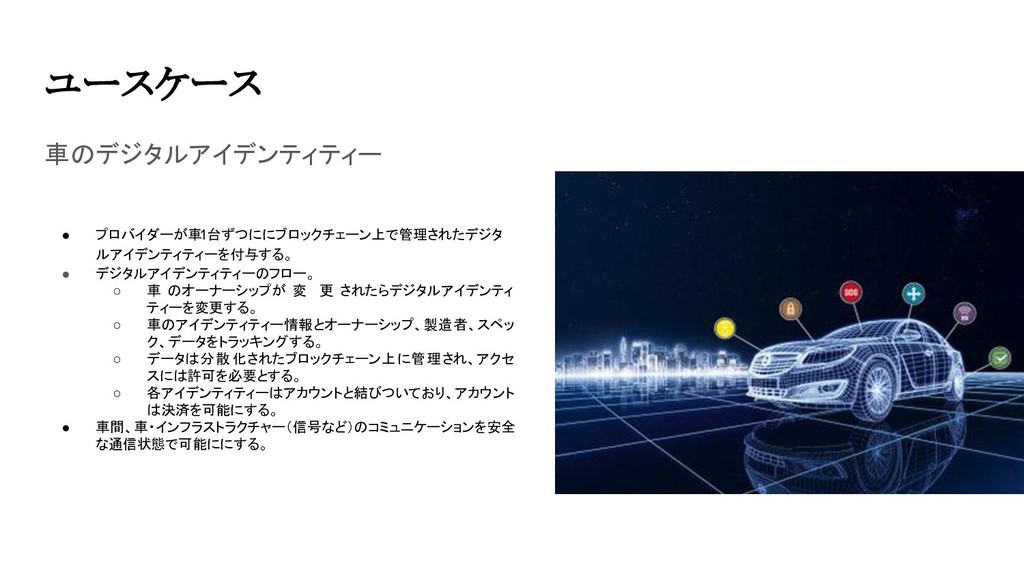

![ブロックチェーンはどう使えるのか? ③3rd partyを除いた価値のP2Pトランザクションによる移転 • M2Mの「スマート」コントラクト →機会同士のインタラクティブなトランザクションにブロックチェーンは使える。 例えば、車と車、車とインフラストラクチャーによる自律的な payment[1]。 • 中央管理者がいない状態でのデータの様々なプレーヤーによるより透明性の高いシェア。](https://files.speakerdeck.com/presentations/766f430e9bc24a0eb3489aaa842ef8b8/slide_10.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

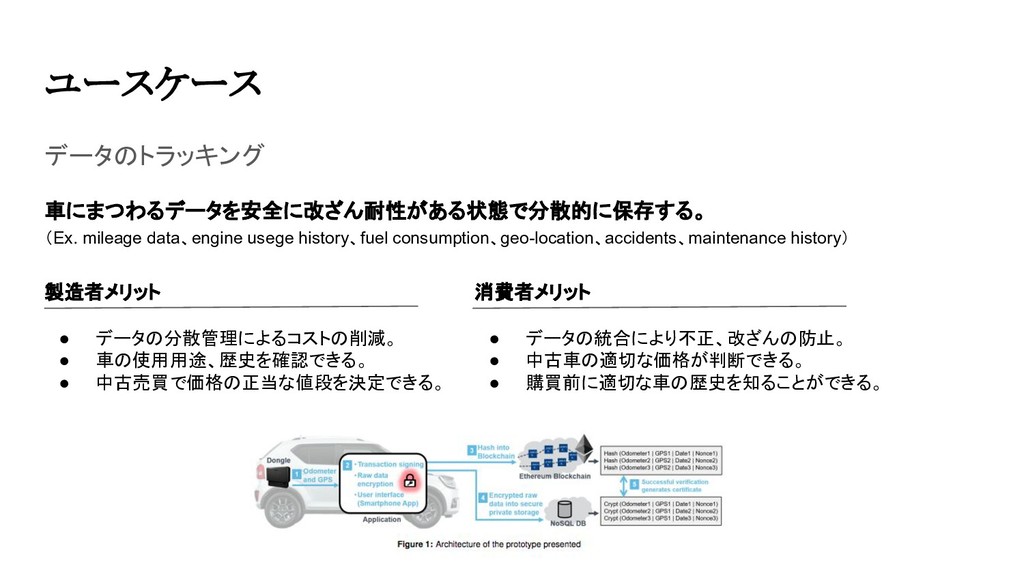

![ユースケース 保険とサプライチェーン・マネジメント(詳しくは下記のURLで)[1] “P2P blockchains with smart contracts could be applied](https://files.speakerdeck.com/presentations/766f430e9bc24a0eb3489aaa842ef8b8/slide_14.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}