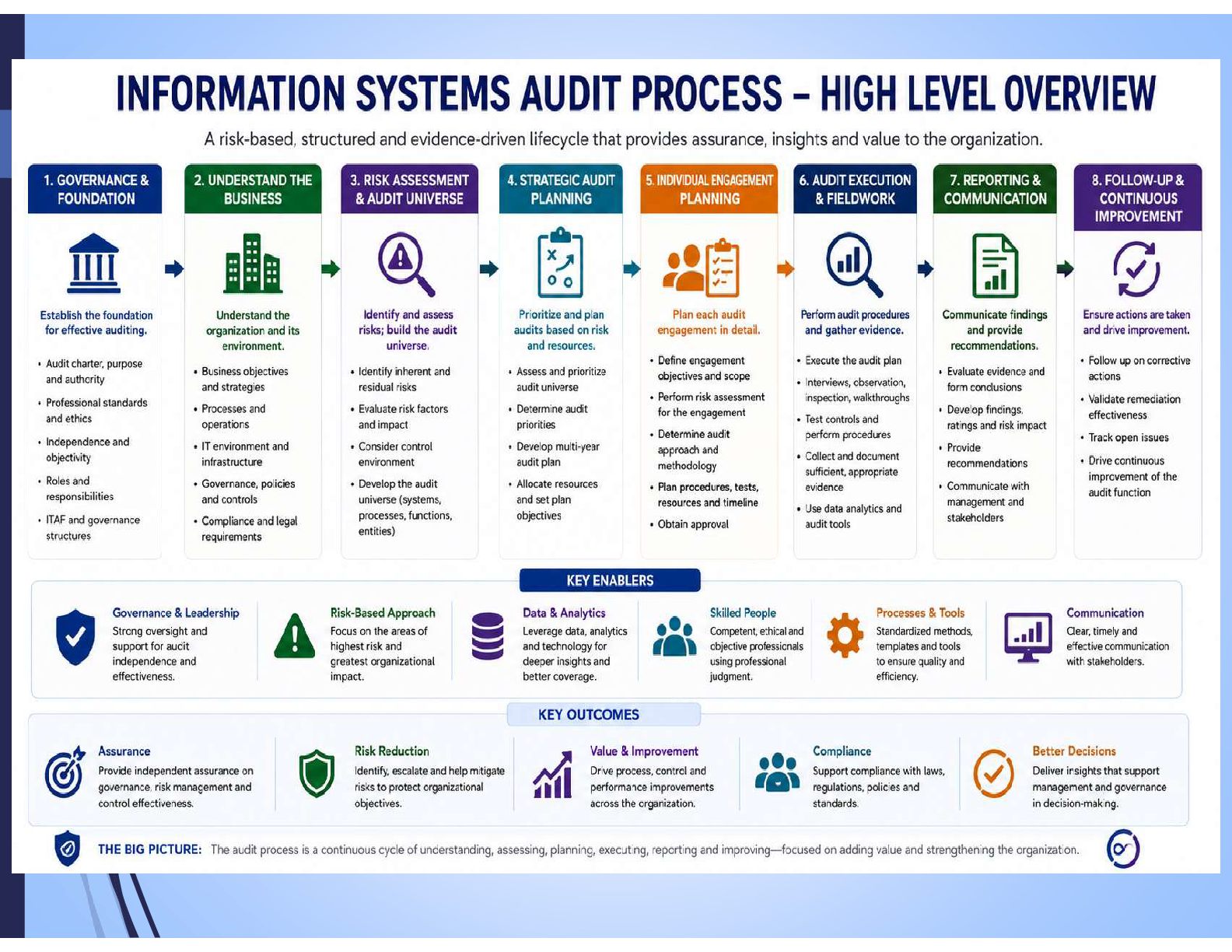

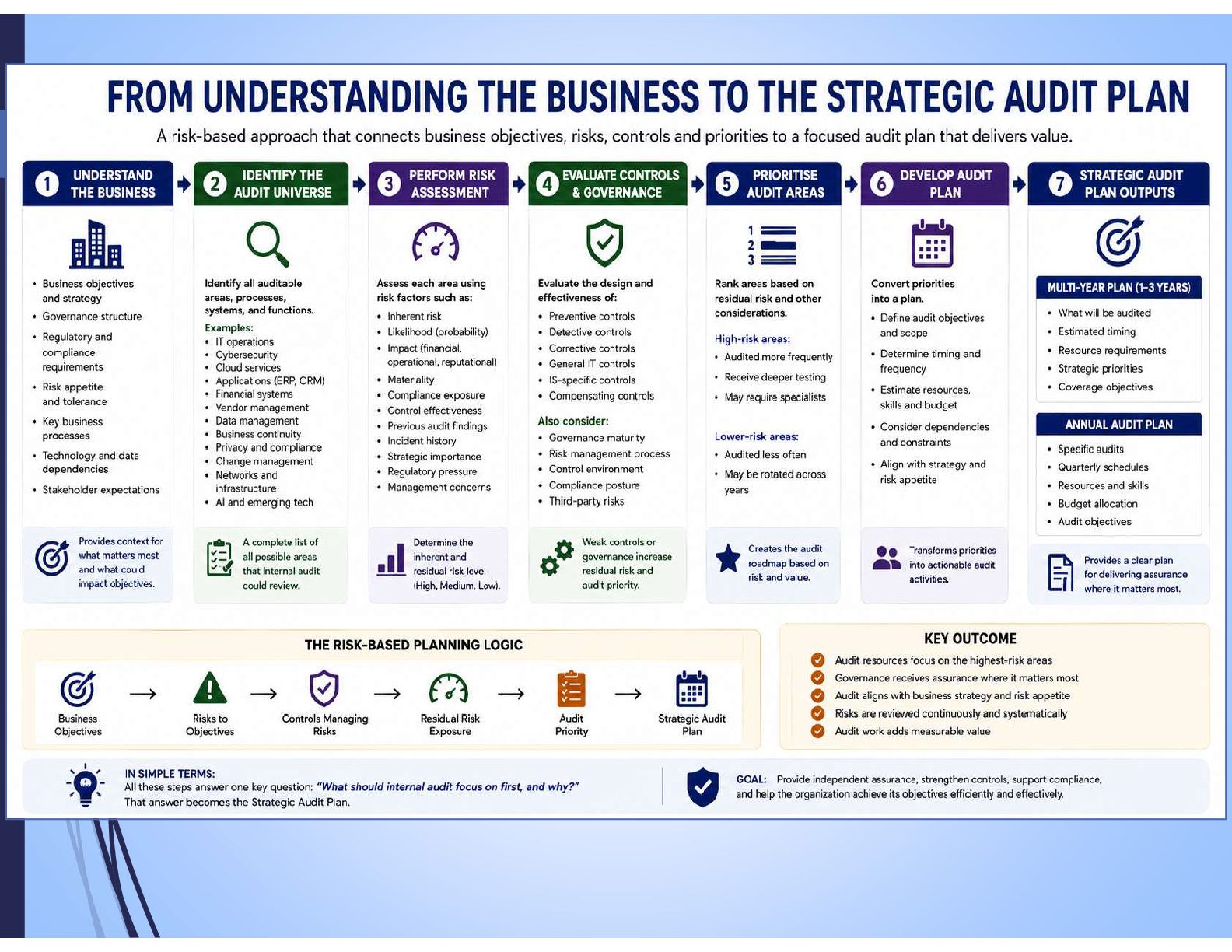

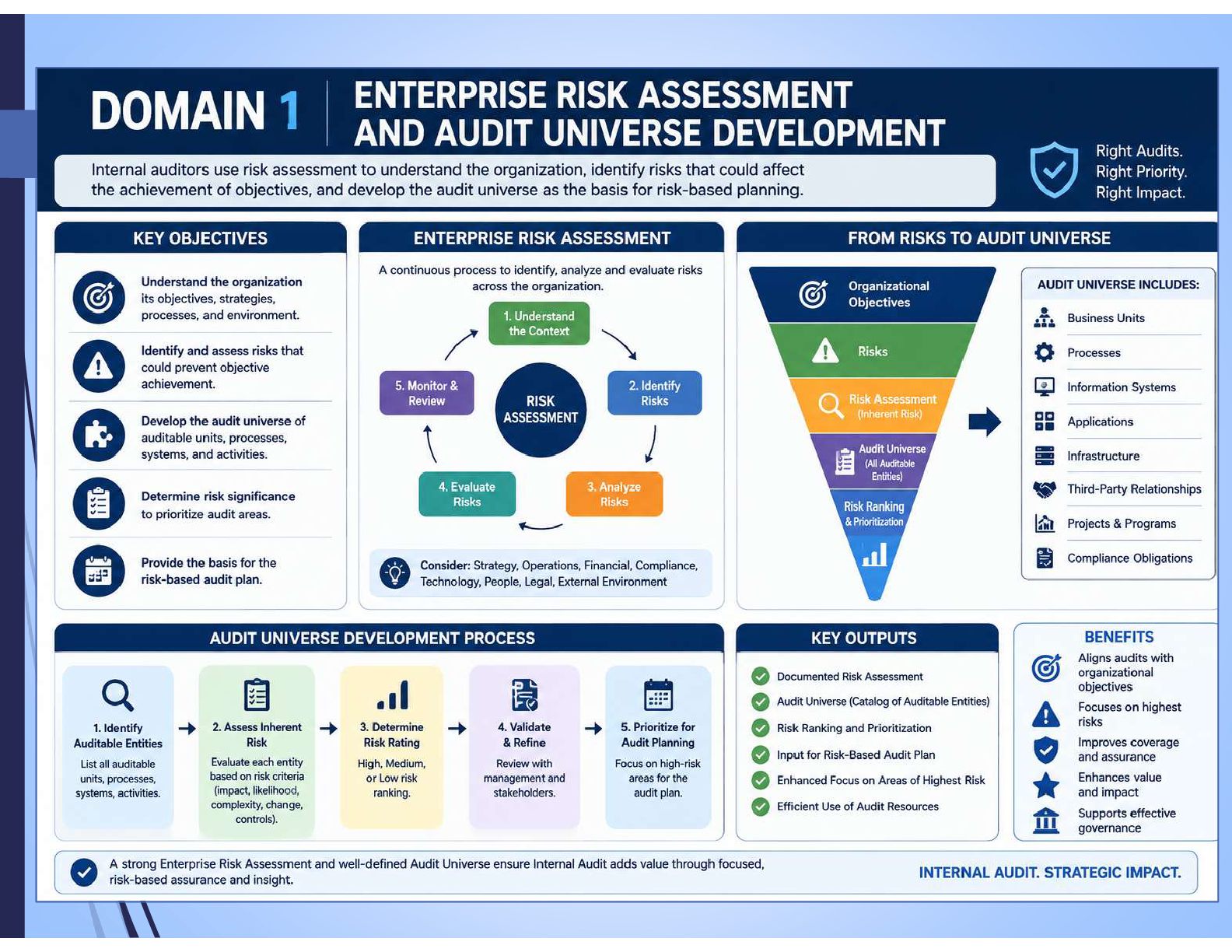

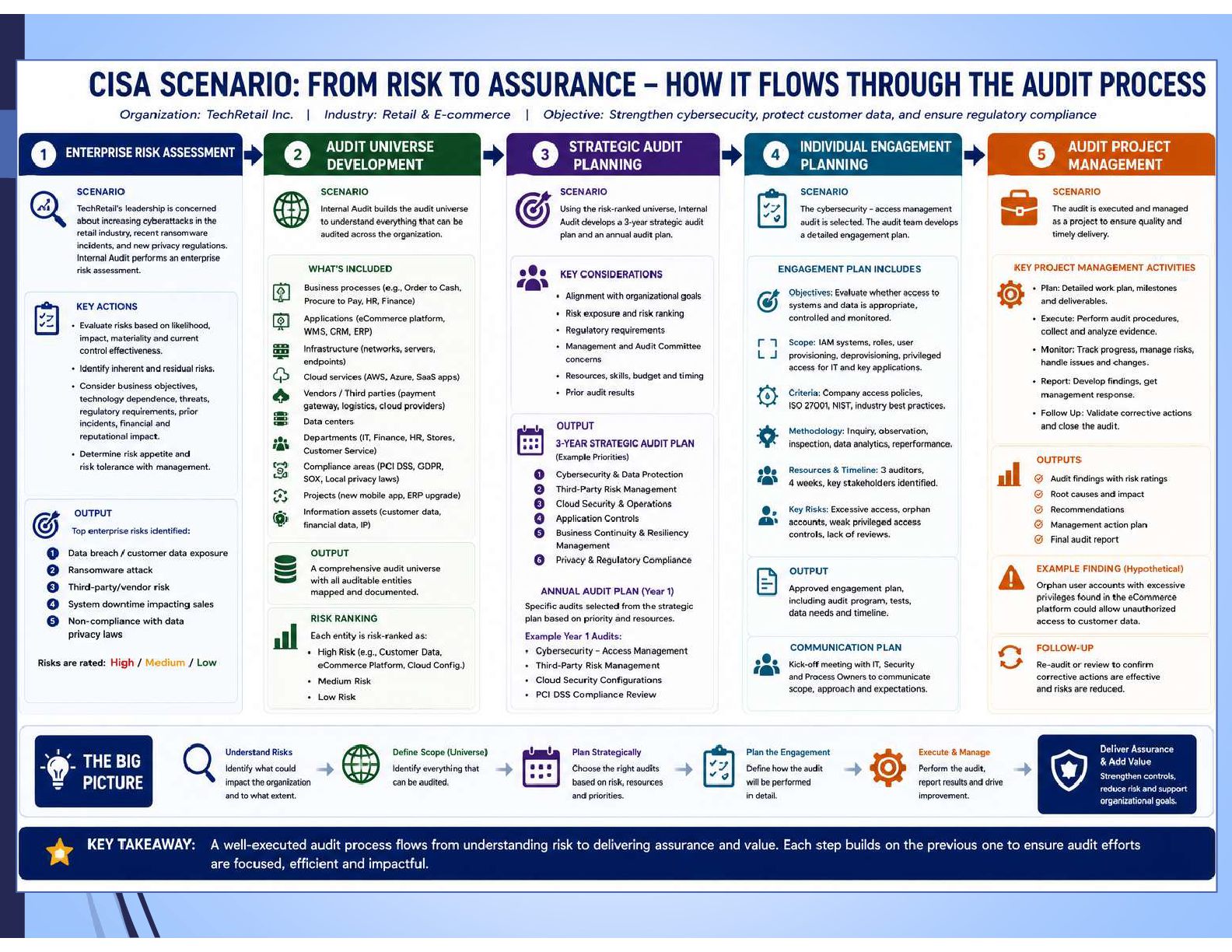

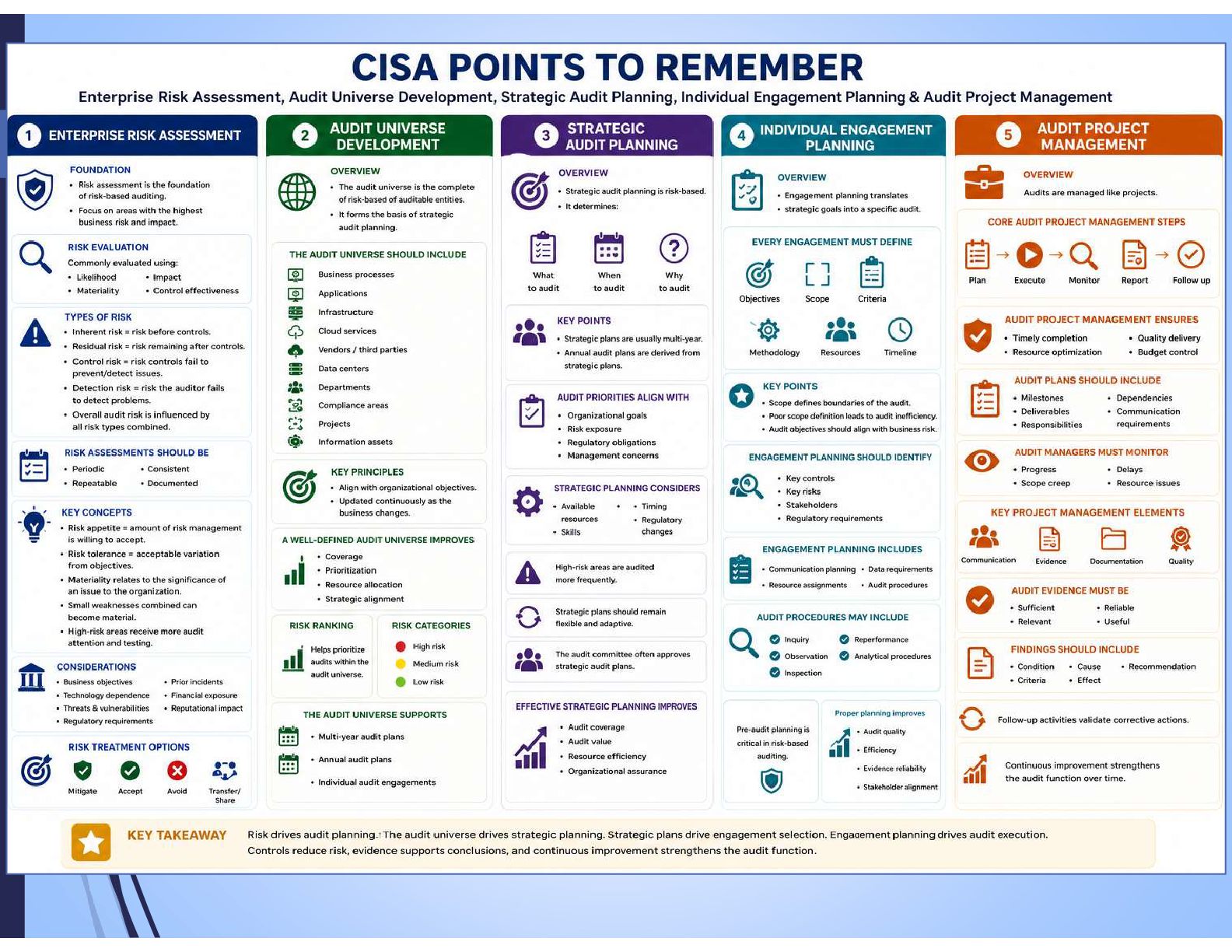

Enterprise Risk Assessment, Audit Universe Development, and Strategic Audit Planning, Individual Engagement Planning and Audit Project Management

We explore how Internal Audit moves from understanding organizational risk to developing a focused, risk-based audit strategy that delivers assurance and business value.

Topics covered in this session include:

• Enterprise Risk Assessment

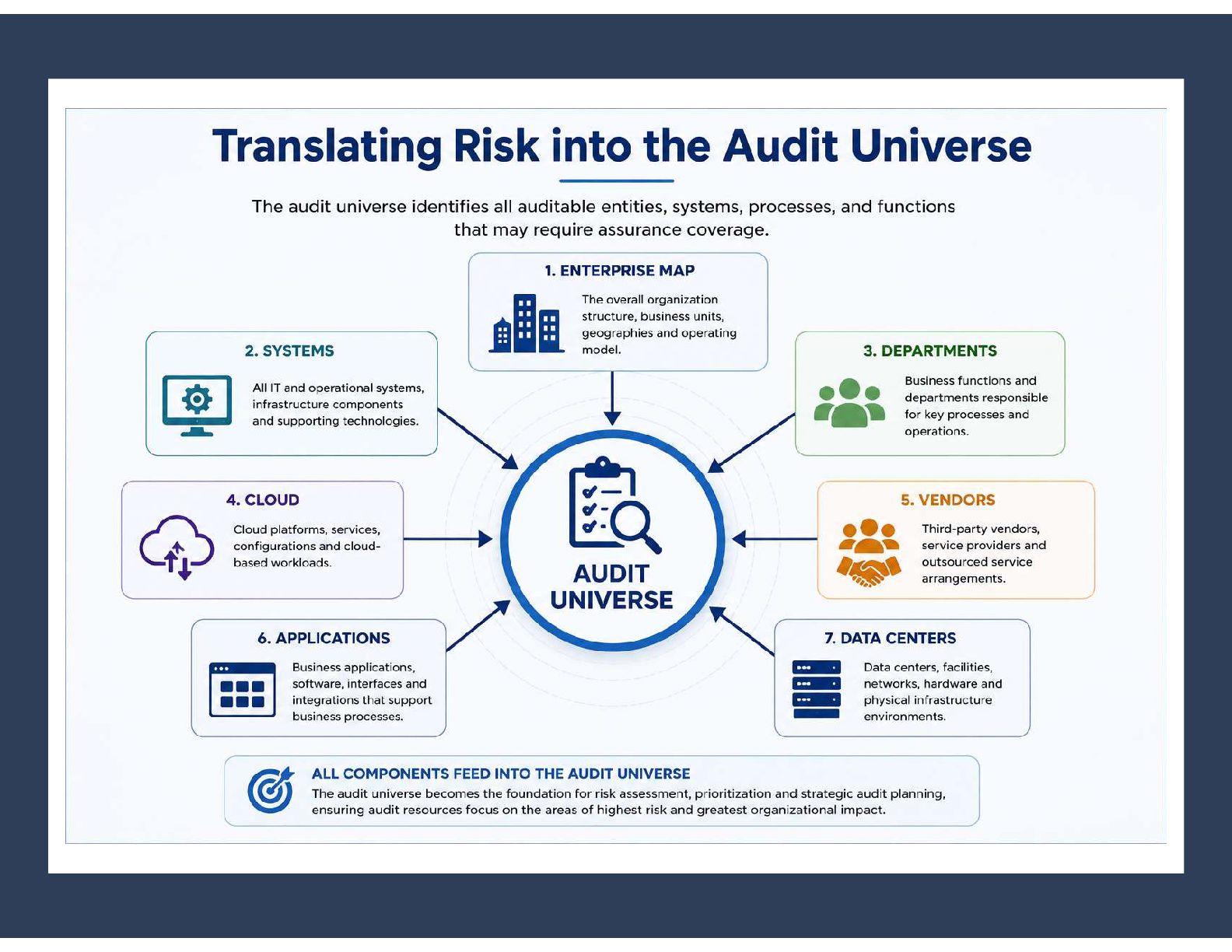

• Audit Universe Development

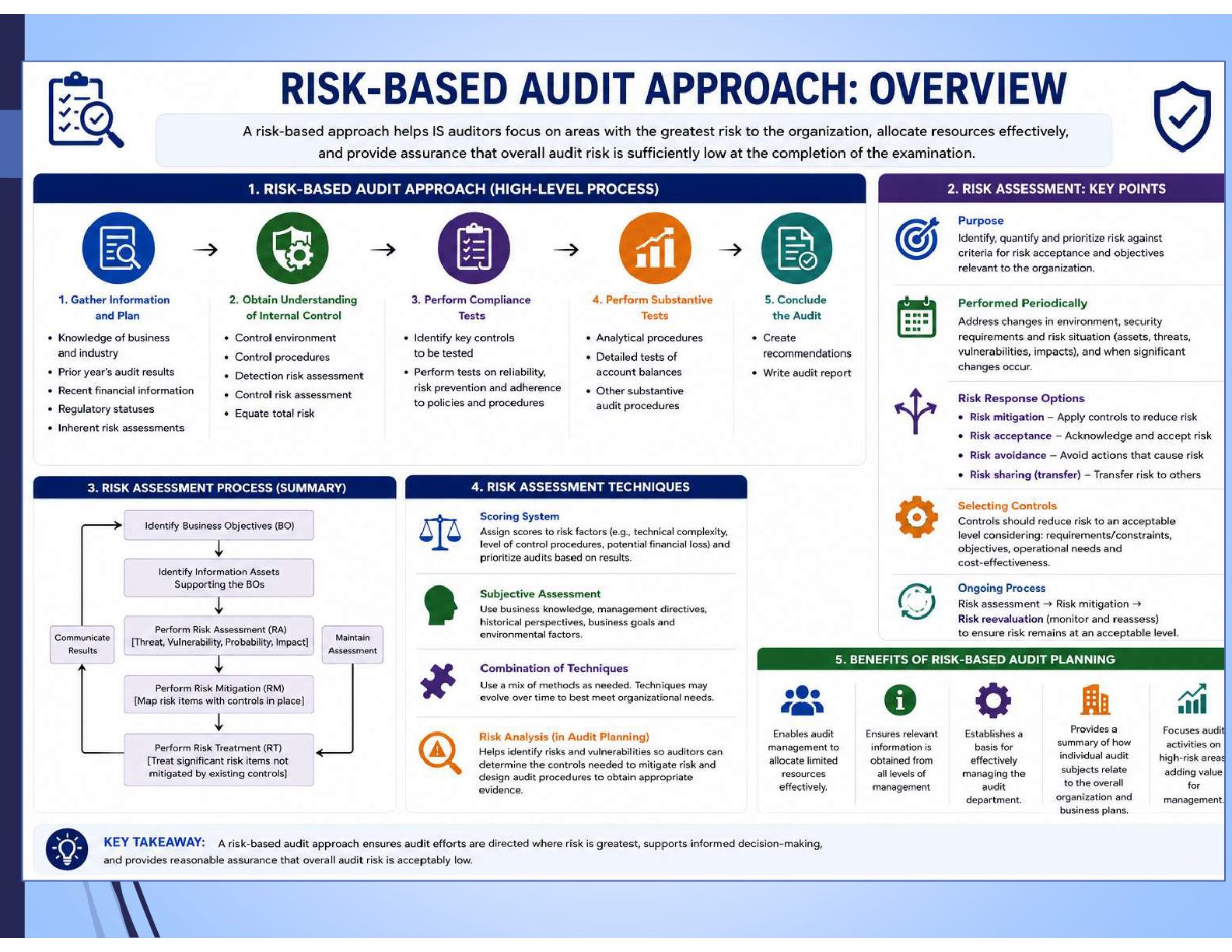

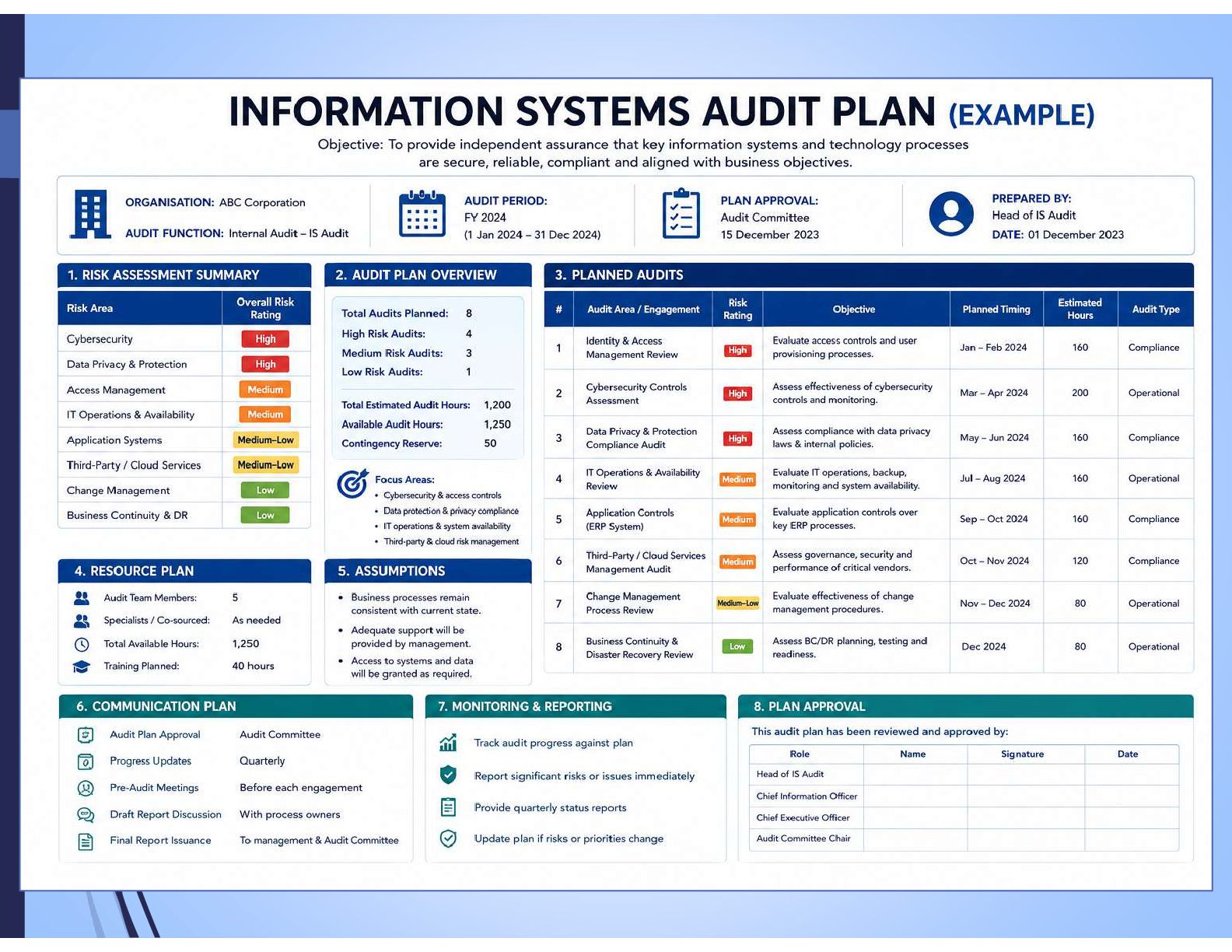

• Risk-Based Audit Planning

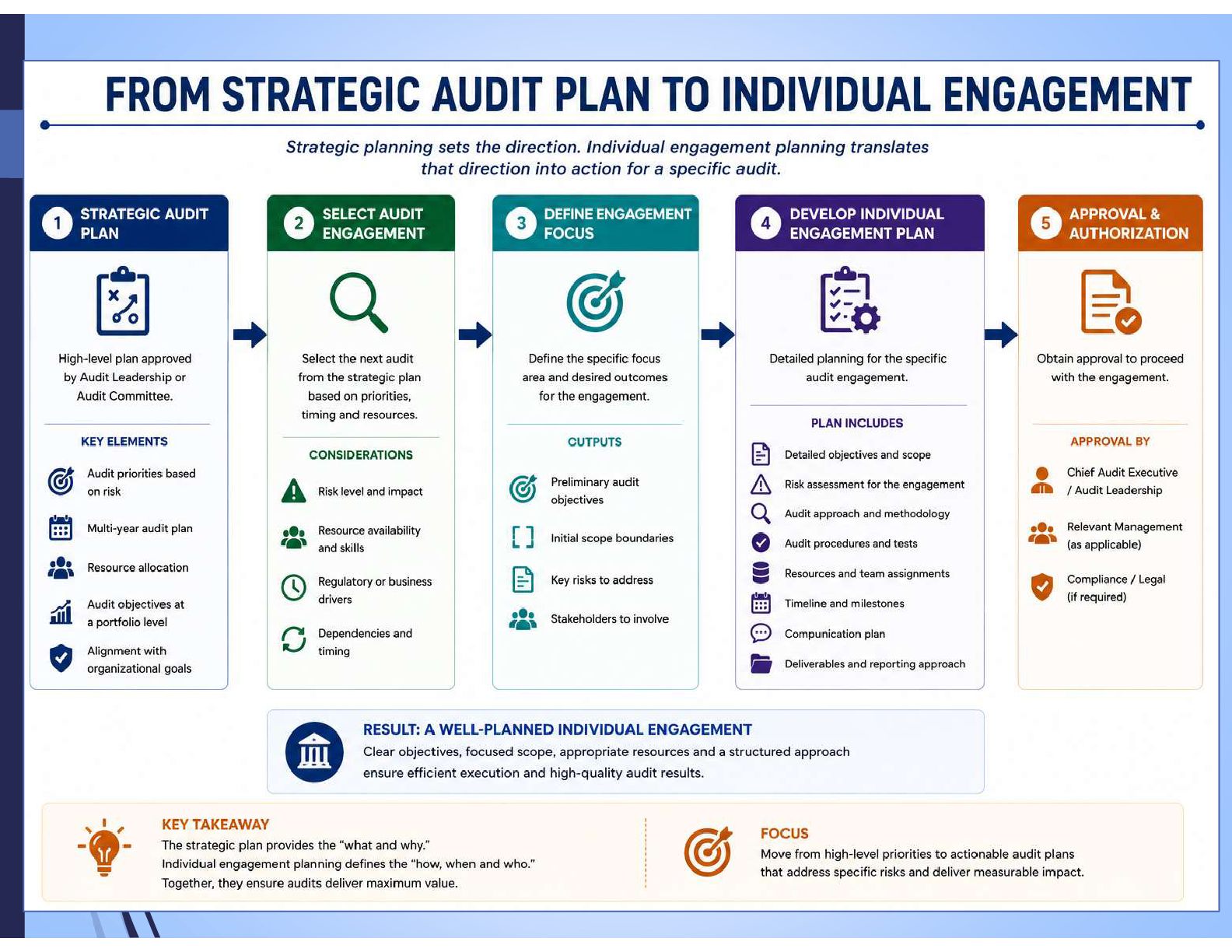

• Strategic Audit Planning

• Individual Engagement Planning

• Audit Project Management

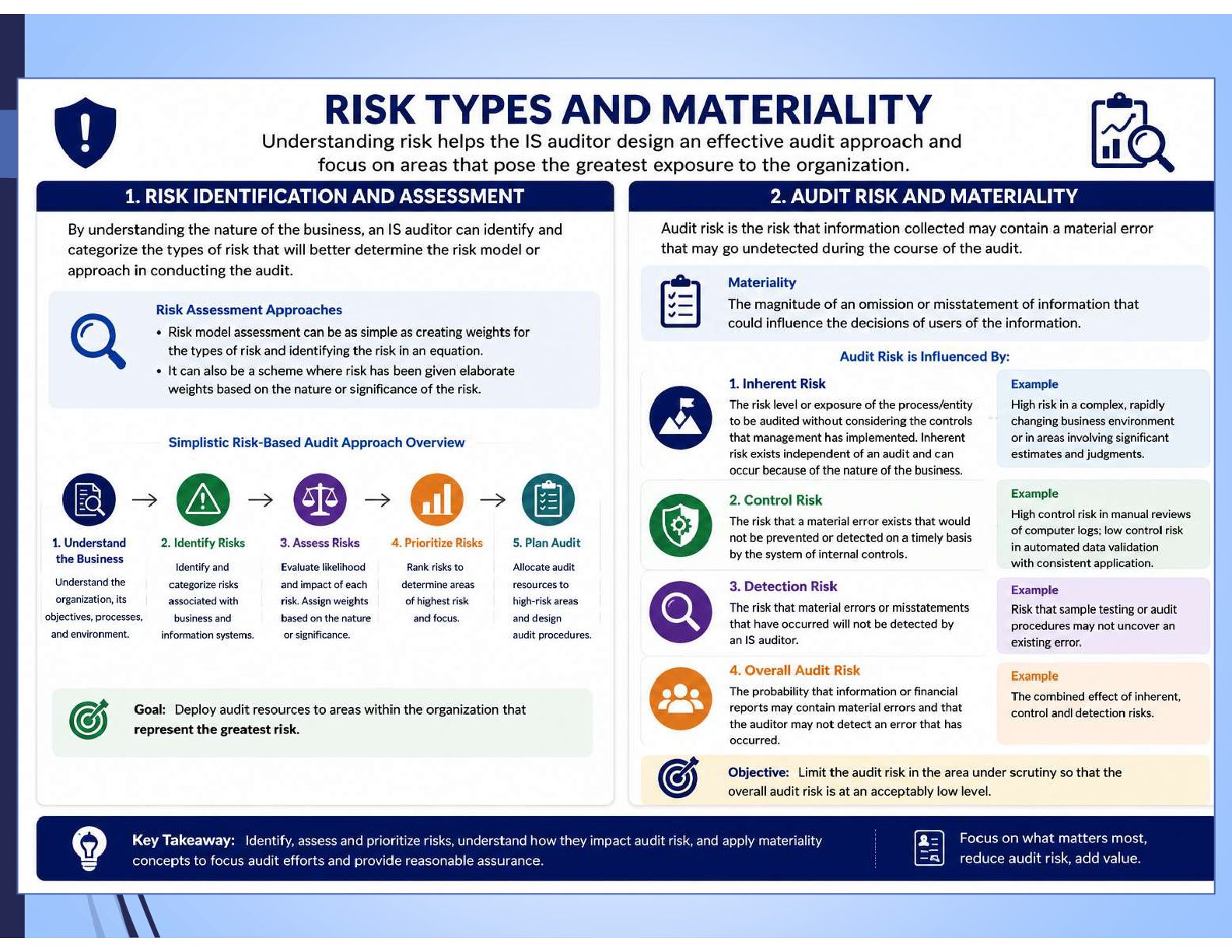

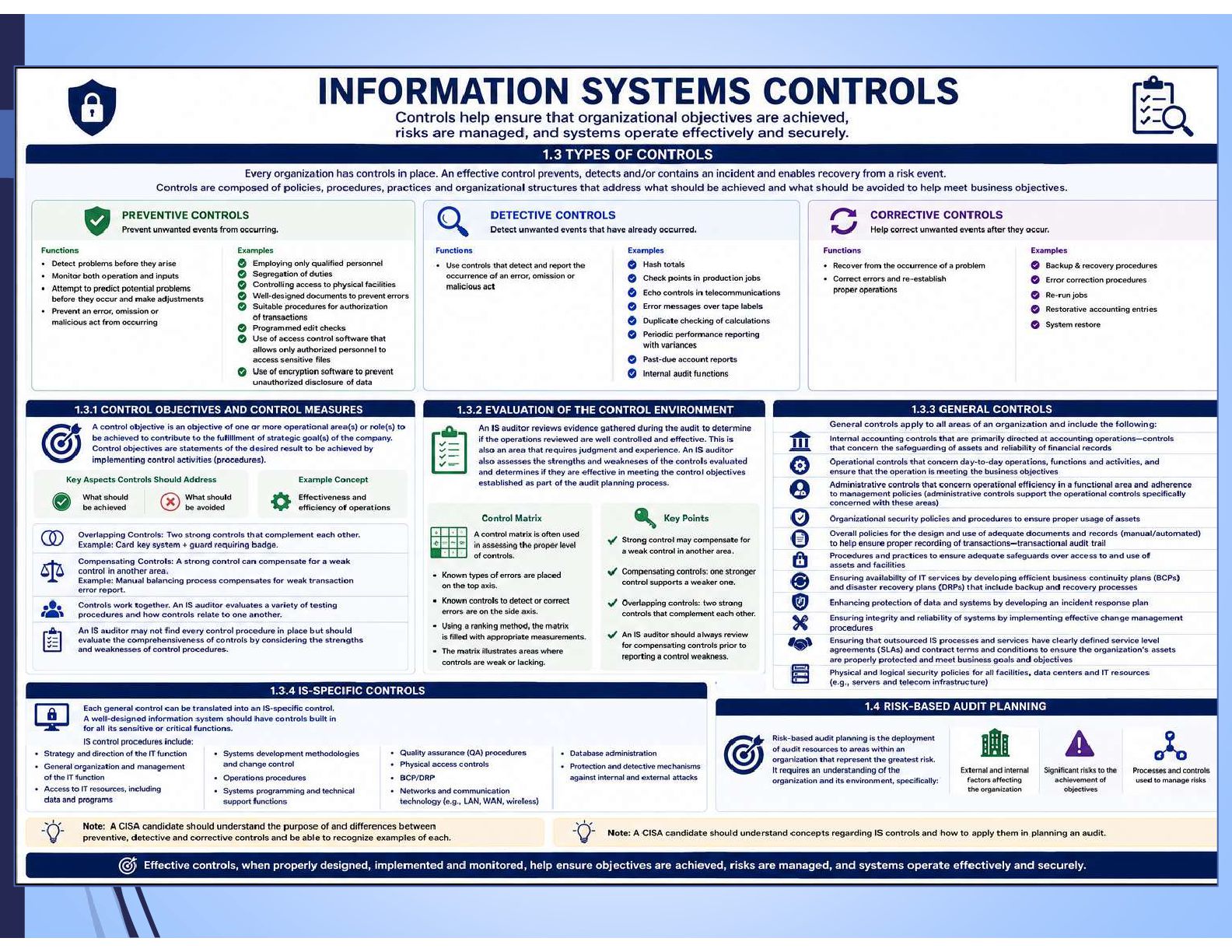

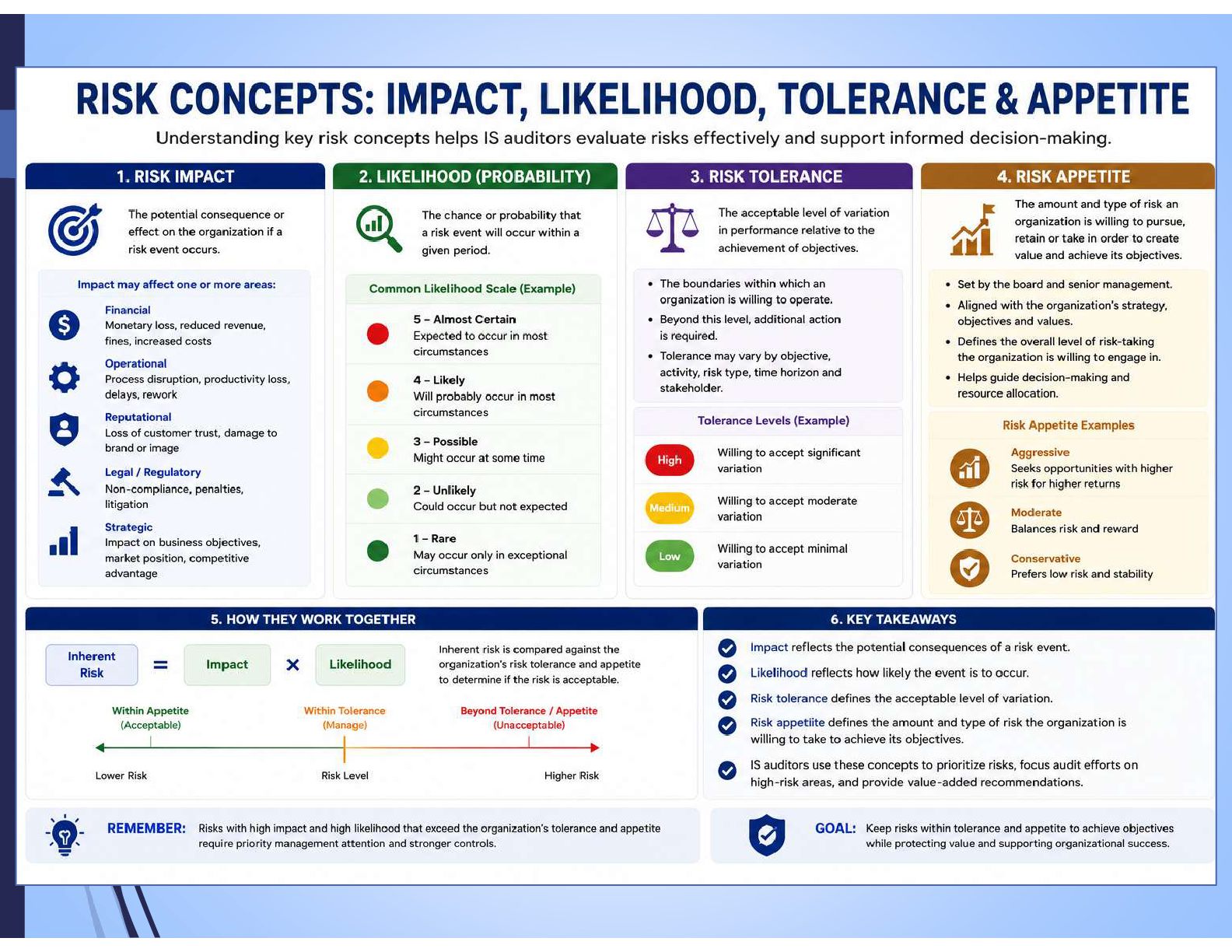

• Audit Risk, Materiality, and Control Concepts

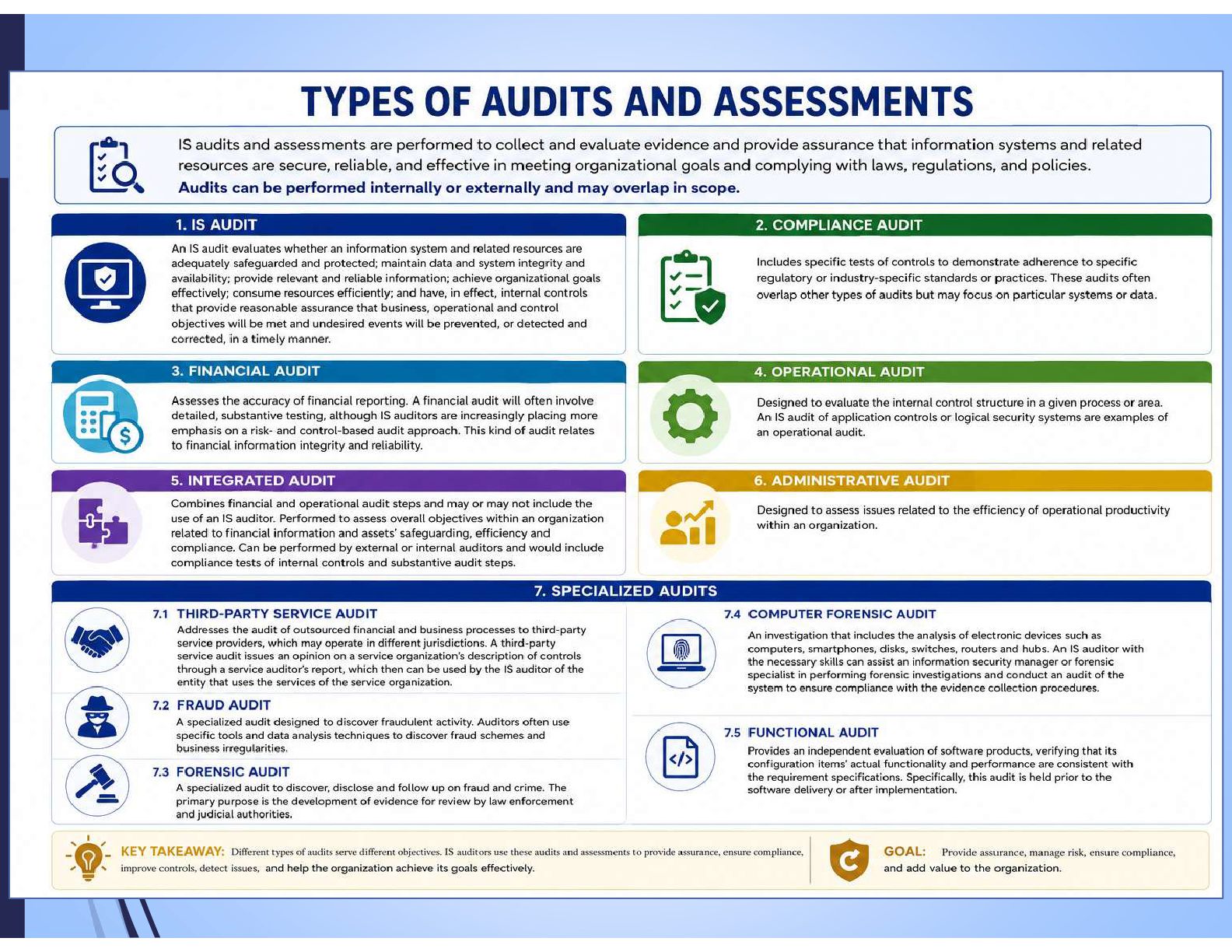

• Types of Audits and Assessments

• Practical CISA scenarios and exam reminders

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}